Takeaways

Every business that handles payments at scale eventually hits the same wall. Reconciliation.

When hundreds or thousands of users send money to the same bank account, matching each payment to the right person becomes a manual, error-prone process. A customer forgets to include a reference number. Another one makes a typo. Your finance team spends hours each week chasing down mismatches and rejected payments.

Virtual accounts and virtual IBANs solve this by giving each user, customer, or transaction its own unique account number, all routed to a single pooled account behind the scenes.

This guide breaks down what virtual accounts and virtual IBANs are, how they work, where they fit in modern payments infrastructure, and how we use them to simplify cross-border stablecoin payments.

What Is An IBAN?

An IBAN, short for International Bank Account Number, is a standardized format for identifying bank accounts across borders in 89 countries.

Developed under the ISO 13616 standard by the International Organization for Standardization, the IBAN system exists to reduce errors in international payments and ensure money reaches the correct bank account on the first attempt.

SWIFT acts as the official IBAN registrar and registration authority. The system was originally conceived to simplify international payments across European countries, but adoption has since expanded well beyond Europe.

How an IBAN Is Structured

An IBAN number consists of up to 34 alphanumeric characters, and every IBAN follows the same pattern regardless of the issuing country:

Component |

Example |

What It Identifies |

|---|---|---|

|

Country code |

GB |

A two letter country code (always only upper case letters) |

|

Check digits |

29 |

Two digits that validate the IBAN before processing |

|

Bank code |

NWBK |

The bank identifier code for the specific financial institution |

|

Branch code |

601613 |

The branch of the issuing financial institution |

|

Account number |

31926819 |

The individual account at that specific bank |

The first four characters are always a two letter country code followed by two check digits. The remaining characters make up the Basic Bank Account Number (BBAN), which is the bank account number in that country's domestic format. The BBAN contains the bank code, branch code, and the individual account number.

.jpg)

For a British IBAN, the bank account number BBAN is 18 characters long. For a German IBAN, it's 22. The exact length of the IBAN bank account number depends on each country's national banking standards, as defined by that country's national central bank or designated payment authority. An IBAN consists of these components in a fixed sequence, and the structure is validated before any financial transaction is processed, reducing rejected payments and transfer delays.

The IBAN format was designed by the European Committee for Banking Standards before being adopted as an international standard by the International Organization for Standardization. The European Committee originally proposed it to standardize international payments within Europe, and it succeeded.

Today, most European countries require IBANs for both domestic payments and international payments, and adoption continues to grow across the Middle East, the Caribbean, and parts of Africa. Not all banks in every country support IBANs yet, but the trend toward global adoption is clear.

How to Find Your IBAN Number

You can find your IBAN number on your bank statement, through your online banking portal, or by contacting your bank directly.

Most banks display the IBAN code prominently in account details once you log in. If your bank is in a country that uses the IBAN system, the IBAN code is simply a reformatted version of your existing bank account number with the country code, check digits, bank code, and branch code added.

Some banks also include the IBAN on physical debit or credit cards, though this varies by financial institution.

IBAN vs. SWIFT Code: What's the Difference?

This is one of the most common points of confusion in international banking, and they serve different but complementary purposes.

An IBAN identifies a specific bank account. A SWIFT code (also called a Bank Identifier Code, or BIC) identifies a specific financial institution within the SWIFT network.

SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, is the global messaging network that banks use to send payments and share financial data internationally.

Feature |

IBAN |

SWIFT/BIC Code |

|---|---|---|

|

Purpose |

Identifies a specific bank account |

Identifies a specific bank or financial institution |

|

Length |

Up to 34 characters |

8 or 11 characters |

|

Used for |

Routing payments to the correct account |

Routing payments to the correct bank |

|

Adopted by |

89 countries (via IBAN registry) |

200+ countries (via the SWIFT network) |

|

Governed by |

ISO 13616 (International Organization for Standardization) |

ISO 9362 (business identifier codes) |

When you send money internationally, the receiving bank often needs both to process international payments correctly. The SWIFT code routes the payment to the correct bank within the SWIFT network. The IBAN then directs it to the correct individual account at that specific bank.

Using the wrong bank code or account number in either identifier can result in rejected payments and transfer delays.

In countries where IBANs are not used, SWIFT codes combined with a local bank account number serve as the standard method for identifying bank accounts and routing international payments to a foreign bank account.

The IBAN registry maintained by SWIFT lists every country's IBAN format, branch code structure, and bank identifier requirements, making it the definitive reference for identifying bank accounts across borders.

Does IBAN Exist in the USA?

No. The United States does not use the IBAN system for domestic payments or bank account identification. Instead, U.S. banks use a combination of an ABA routing number (a nine-digit bank code that identifies the financial institution) and an account number. For international transfers into the U.S., senders use SWIFT codes combined with the recipient's routing number and account number.

This creates friction for businesses operating across different countries and handling international payments. A European customer expecting to send payments via an IBAN encounters a completely different system when sending to a U.S. bank account number.

Virtual IBANs, as we'll see, help bridge this gap by giving businesses local account details in multiple countries without needing to open a foreign bank account in each one.

What Is A Virtual Account?

A virtual account is a unique account number assigned to a customer, transaction, or business unit that sits on top of a single underlying physical bank account.

The virtual account does not hold funds independently. Instead, it acts as a routing layer, directing incoming payments to the correct place within the central master account.

Think of it as a building with one mailroom but separate mailboxes for every tenant. The mail all arrives at one address, but each piece goes to the right person because every mailbox has its own number.

For businesses, this means:

- Automatic reconciliation via unique account numbers.

- Elimination of reference code errors.

- Significant reduction in manual finance workloads.

Virtual accounts are widely used in fintech, e-commerce, insurance, and increasingly in crypto and stablecoin infrastructure.

What Is A Virtual IBAN?

A virtual IBAN (sometimes shortened to vIBAN or VBAN) is a virtual account that follows the IBAN format.

vIBAN looks identical to a traditional IBAN, functions identically for the person making the payment, and can send and receive payments through the same banking rails. The difference is that instead of being linked 1:1 to a physical bank account, a virtual IBAN routes funds to a central master account alongside potentially thousands of other virtual IBANs.

_02.jpg)

A virtual IBAN contains the same components as a regular IBAN, i.e., a country code, check digits, bank identifier code, and account number. The person paying has no way to tell whether they're sending to a virtual IBAN or a traditional one. For them, it's just an IBAN number they enter during a bank transfer.

Behind the scenes, the virtual IBAN acts as a sub-account. Each one is tied to a specific customer or purpose, and the issuing platform can instantly identify every incoming payment without relying on manual matching.

Virtual IBAN vs. Traditional IBAN

Feature |

Traditional IBAN |

Virtual IBAN |

|---|---|---|

|

Linked to a physical bank account |

Yes (one-to-one) |

No (many-to-one, via central master account) |

|

Unique per customer |

Requires a new bank account |

Issued instantly, no new bank account needed |

|

Reconciliation |

Manual (reference codes) |

Automatic (unique identifier per customer) |

|

Setup time |

Days to weeks (bank onboarding) |

Seconds to minutes (API-based) |

|

Multi-currency support |

Requires separate accounts per currency |

Can support multiple currencies on one IBAN |

|

Best for |

Personal banking, single-entity accounts |

High-volume platforms, marketplaces, exchanges |

How Do Virtual IBANs Work?

The TL;DR is that the entire process happens within the existing banking infrastructure. No new payment rails are needed. The virtual IBAN layer sits on top of traditional bank transfers, adding intelligence without adding friction.

1. Issuance

A business integrates with a Banking-as-a-Service provider or payment institution that supports virtual IBAN issuance. Through an API, the business requests a new virtual IBAN for each customer or use case.

2. Payment Collection

The customer receives their unique virtual IBAN and uses it to send payments via standard bank transfers (SEPA in Europe, FPS in the UK, or local domestic payments elsewhere). The sender's bank processes the payment exactly as it would to any traditional bank account.

3. Routing

The payment arrives at the provider's central master account. The system immediately identifies the virtual IBAN, matches it to the correct customer or purpose, and records the transaction.

4. Reconciliation

Because each payment is linked to a unique virtual IBAN, the receiving platform knows exactly who paid, how much, and when, without any manual intervention.

Use Cases for Virtual IBANs

Crypto Exchanges and Wallets

Crypto platforms handle fiat deposits from thousands or millions of users. Each user needs to fund their account before buying crypto. Without virtual IBANs, every user sends money to the same bank account with a reference code, and the exchange's team has to match them manually. This creates transfer delays, misrouted funds, and customer support headaches.

With virtual IBANs, each user gets a dedicated IBAN. Their bank transfer goes straight to their account, automatically. No reference codes. No mismatches.

This is exactly how we structured our on-ramp infrastructure in our partnership with MetaMask. When a user sends a transfer, the system matches the payment to the user instantly, enabling faster conversion to stablecoins like USDC, USDT, or other digital assets.

In our partnership with Cross River, we use fully routable subledgers for real-time transaction visibility across ACH, wire transfers, and instant payment rails like RTP and FedNow, all powered by virtual account infrastructure.

Cross-Border Payments and Remittances

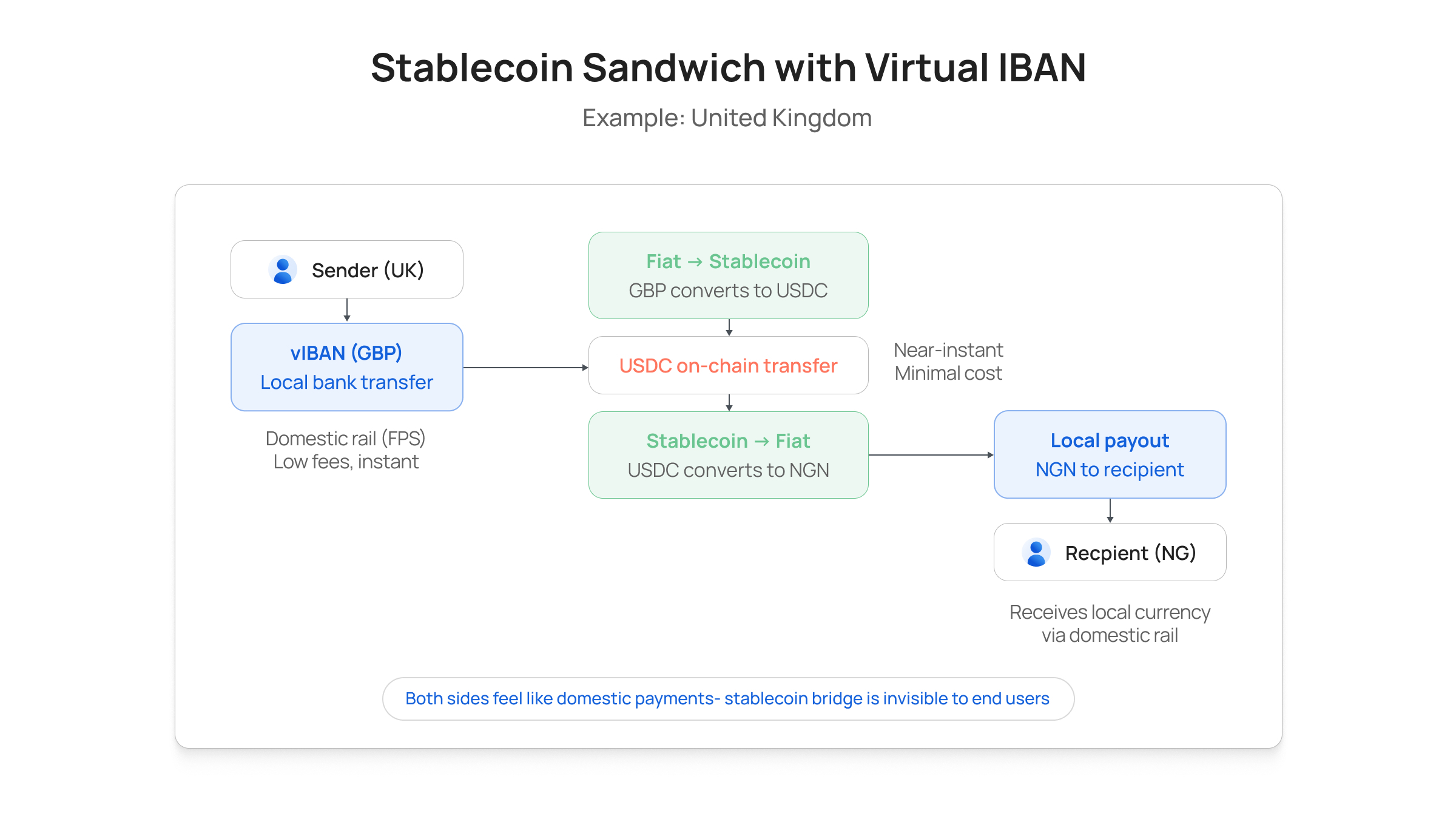

Businesses that send and receive payments in different countries can either open physical bank accounts in every market (expensive, slow, compliance-heavy) or use virtual IBANs to establish local payment presence without local bank accounts.

A remittance company can issue virtual IBANs in EUR, GBP, and USD, allowing customers in multiple countries to send money as a domestic payment rather than an international transfer. This typically reduces fees and settlement times significantly.

When combined with stablecoin rails, virtual IBANs become even more powerful. Fiat enters through a local virtual IBAN, converts to a stablecoin, moves instantly across borders, and exits as local currency on the other side. This is the stablecoin sandwich architecture that's reshaping international payments.

E-Commerce and Marketplaces

Marketplaces managing payouts to thousands of sellers need a clean way to segregate funds. Virtual IBANs let each seller receive payments through their own unique bank account number, while the marketplace maintains one pooled account for operational control.

Sellers in different countries can receive payments via domestic bank transfers rather than costly international transactions, and the marketplace can reconcile every money transfer automatically.

Payroll and Contractor Payments

Companies paying contractors globally through stablecoin payroll infrastructure use virtual accounts to manage multi-currency payouts without maintaining bank accounts in every country they operate in.

Treasury Management

Large enterprises use virtual IBANs for internal fund management, assigning separate virtual accounts to different departments, subsidiaries, or projects. Each virtual IBAN acts as a ledger entry within the same physical bank account, making it easier to track internal money transfers and capital allocation.

Named IBANs vs. Virtual IBANs: Is There a Difference?

In practice, a "named IBAN" is a virtual IBAN that has been assigned to and registered in the name of a specific individual or entity. The term is used by platforms to describe virtual bank accounts that carry the user's verified identity, not just a generic reference number.

The distinction matters for compliance. A generic virtual IBAN is an anonymous routing number. A named IBAN ties that routing number to a KYC-verified identity, which is increasingly important under regulations like the EU's Anti-Money Laundering Regulation (AMLR), which will require virtual IBAN issuers to identify end-users and link them to specific underlying payment accounts by 2027.

For crypto and stablecoin platforms, named IBANs serve a dual purpose.

- Improve reconciliation (every payment is automatically matched to the right user)

- Satisfy compliance requirements (every virtual account is tied to a verified identity)

What Are the Risks of Virtual IBANs?

While beneficial, virtual IBANs could carry risks that businesses must navigate:

- Financial Crime: Their rapid issuance makes them potential targets for money laundering and layering illicit funds, as noted by the EBA.

- Regulatory Complexity: Fragmentation across jurisdictions creates compliance hurdles, as legal definitions of virtual accounts vary significantly by country.

- Ownership Transparency: If not properly linked to a verified identity, they can obscure beneficial ownership, a gap the EU's AMLD6 aims to close by 2027.

- Monitoring Challenges: Because they look identical to traditional accounts, legacy banking systems may fail to detect suspicious cross-border activity.

Platforms that take compliance seriously, like Transak (which holds MTLs across the U.S., plus licenses in the UK, EU, Australia, Canada, and India), mitigate these risks by tying every virtual account to a KYC-verified identity and implementing continuous transaction monitoring.

Virtual IBANs in the Context of Embedded Finance

Embedded finance describes the integration of financial services directly into non-financial products through APIs. Instead of redirecting users to a bank, the banking functionality lives inside the app.

Virtual IBANs are a foundational building block of embedded finance. They allow any platform to offer payment collection, fund segregation, and multi-currency accounts without becoming a bank. The virtual IBAN is issued by a licensed financial institution behind the scenes, while the user-facing platform controls the experience.

For crypto and stablecoin infrastructure, this model is increasingly important. Platforms like Transak use Virtual Account APIs to let partner apps enable fiat-to-crypto conversion natively within their interfaces. The user sends a bank transfer to their named IBAN, and the funds are automatically converted to stablecoins and delivered to their wallet. No app switching or manual reconciliation.

This is what makes virtual accounts the connective tissue between traditional banking and blockchain-based payment infrastructure. They bridge the gap between fiat and crypto, using familiar financial environments that users already trust.

How Virtual Accounts Power Stablecoin On-Ramps

The path from fiat to stablecoins involves several steps: KYC verification, fiat payment, currency conversion, blockchain transaction, and wallet delivery. Virtual accounts simplify the fiat payment step, which is often the point where the most friction exists.

Here's how it works in practice:

- The platform verifies the user's identity through Transak's compliance infrastructure.

- The user receives a dedicated virtual bank account tied to their verified identity.

- The user initiates a standard bank transfer from their existing bank account to their named IBAN. For the user, this feels identical to any other bank transfer.

- The virtual account infrastructure instantly matches the incoming payment to the user. No reference codes needed.

- The fiat is converted to the requested stablecoin (USDC, USDT, or others) and delivered to the user's wallet.

This flow eliminates two of the biggest friction points in crypto on-ramping, which are failed payment matching and manual reconciliation. It also supports near 1:1 stablecoin pricing because bank transfers are cheaper to process than card payments.

How to Get a Virtual IBAN or Virtual Account

If you're a business looking to issue virtual IBANs to your users, you'll need to work with a licensed provider. Options include Banking-as-a-Service platforms, electronic money institutions (EMIs), or payment infrastructure providers.

The typical integration process looks like this:

- Choose a provider that supports virtual IBAN issuance in your target markets. Key considerations: regulatory coverage, supported currencies, API quality, and compliance capabilities.

- Integrate via API. Most providers offer REST APIs for creating, managing, and querying virtual accounts.

- KYC your users. Depending on the regulatory framework, you may need to verify users before issuing them a virtual IBAN. Some providers handle this for you.

- Issue virtual IBANs. Once integrated, you can create virtual IBANs programmatically, often in seconds.

For financial applications, we enable fiat payment collection through named IBANs, built-in KYC/AML compliance, and automatic conversion to stablecoins, all through a single API integration.

Frequently Asked Questions

What is a virtual IBAN number?

A virtual IBAN is a unique International Bank Account Number that functions like a traditional IBAN for sending and receiving payments but is not linked to a separate physical bank account. The International Bank Account Number format remains the same, with the same country code, check digits, bank code, and Basic Bank Account Number (BBAN). The difference is that it routes payments to a central master account rather than a standalone account, enabling automatic reconciliation and multi-currency support for businesses managing high payment volumes.

What does vIBAN mean?

vIBAN stands for virtual IBAN, short for virtual International Bank Account Number. It's sometimes also written as VBAN in banking. The terms are interchangeable and refer to a virtual account number in the International Bank Account Number format that routes payments through existing banking infrastructure to a pooled underlying account. The Basic Bank Account Number (BBAN) component within the virtual IBAN follows the same structure as a traditional IBAN.

Is an IBAN the same as a SWIFT code?

No. An IBAN identifies a specific bank account, while a SWIFT code (also called a Bank Identifier Code or BIC) identifies a specific financial institution within the SWIFT network. For international payments, you often need both: the SWIFT code to route the payment to the correct bank, and the IBAN to direct it to the correct account.

Is an IBAN the same as a routing number?

Not exactly. An IBAN is the international standard for bank account identification used in 89 countries. A routing number (ABA routing number) is specific to the United States and identifies a bank within the ACH network. They serve similar purposes in their respective systems, but they follow different formats and banking standards.

Does IBAN exist in the USA?

No. The United States does not use the IBAN system. U.S. domestic payments use ABA routing numbers (nine-digit bank codes) combined with account numbers. For receiving international transfers, U.S. banks use SWIFT codes. Some virtual account providers bridge this gap by offering virtual IBANs alongside virtual ACH account details for businesses operating in both U.S. and IBAN-based markets.

What are the use cases for virtual IBANs?

Virtual IBANs are used across crypto exchanges and wallets (for fiat deposit matching), cross-border payments and remittances (for local payment presence in multiple countries), e-commerce marketplaces (for seller fund segregation), payroll platforms (for multi-currency contractor payments), and treasury management (for internal fund tracking across business units).

How do I find my IBAN number?

Check your bank statement, log into your online banking portal and look under account details, or contact your bank directly. If your bank is in one of the 89 countries using the International Bank Account Number system, your IBAN is a standardized version of your existing bank account number with a country code, check digits, bank code, and bank identifier added. The Basic Bank Account Number (BBAN) portion of your IBAN maps directly to your domestic account number.

Transak is the payments infrastructure for stablecoins and crypto. With Virtual Account APIs, named IBANs, and compliance-ready rails, Transak enables apps to onboard users, facilitate cross-border payments, and support multi-party payment flows natively within their platforms. Integrated by 600+ apps and used by over 10 million users globally. Learn more at transak.com.