Takeaways

Traditional financial settlement is slow by design. A stock trade executed on Monday does not legally change hands until Wednesday. That 48-hour gap is a liability that locks billions of dollars in collateral and invites risks and inefficiencies.

Atomic settlement eliminates that gap. Both legs of a transaction, the asset and the payment, move in a single operation. Either both settle or neither does. There is no in-between. No waiting. No window where one party has delivered and the other has not paid.

This article explains what atomic settlement is, why it matters for financial infrastructure, how stablecoins make it practical, and what enterprises need to evaluate before adopting it.

What Atomic Settlement Means

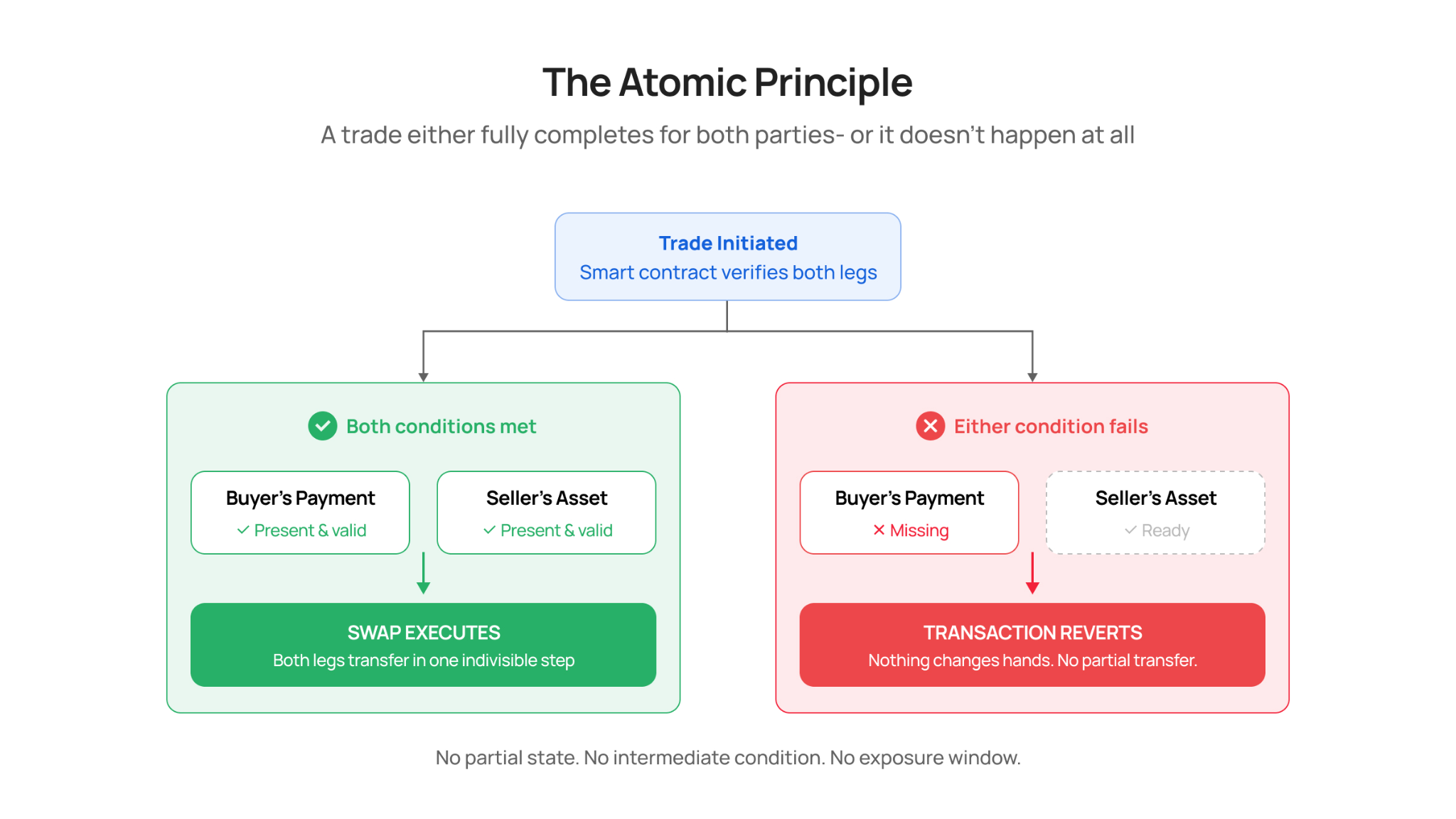

Atomic settlement means a trade either fully completes for both sides at the same instant, or it doesn't happen at all. There's no in-between.

In computer science, an atomic operation cannot be divided into smaller steps. It succeeds completely or fails completely. No partial state or intermediate condition.

In finance, atomic settlement applies this principle to Delivery-versus-Payment (DvP)*. The transfer of an asset and its corresponding payment execute as one indivisible transaction. The contract governing the trade enforces an all-or-nothing condition. If the buyer's payment and the seller's asset are both present, both transfer simultaneously. If either condition fails, nothing changes hands.

This is fundamentally different from traditional DvP. The "versus" in legacy DvP implies two separate processes that are coordinated but not unified. Clearinghouses and central counterparties sit between buyer and seller to manage the risk that one side defaults before the other settles. Atomic settlement removes that coordination problem entirely.

The result is that counterparty risk (the risk that the other party in a financial transaction fails to fulfill their side of the deal) drops to near zero at the point of execution.

*DvP (Delivery versus Payment) is a settlement rule requiring that the delivery of an asset and the payment for it are linked, so that one only happens if the other also happens. The goal is to prevent a situation where a seller hands over the asset but doesn't get paid, or a buyer pays but doesn't receive the asset.

The Problem With Traditional Settlement

Most securities markets today operate on a T+2 settlement cycle. The "T" stands for trade date. The number represents business days before the transaction becomes final. Two full business days.

During that window, several things happen. None of them is good for capital efficiency.

- Counterparty risk stays open. The buyer could send payment, but not receive the asset. The seller could deliver the asset but not receive payment. Clearinghouses absorb this risk, but they charge for it through margin requirements and collateral deposits.

- Capital sits trapped. Billions of dollars are locked in clearing fund deposits and margin collateral to hedge against settlement failure. That capital cannot be deployed elsewhere. It earns nothing while it waits.

- Reconciliation is expensive. Multiple intermediaries, including custodians, registrars, transfer agents, and central counterparties, each maintain their own ledgers. Back-office teams spend hours reconciling discrepancies across these systems at the end of each business day.

- Markets close. Settlement only happens during business hours on weekdays. A trade executed on Friday afternoon does not settle until Tuesday. Weekend and holiday gaps extend the risk window further.

The U.S. moved to T+1 settlement in May 2024. The National Securities Clearing Corporation reported a roughly 30% decrease in its clearing fund, freeing approximately $3.7 billion in collateral. But T+1 still leaves a full business day of exposure. Europe remains on T+2, with a target move to T+1 by October 2027.

How Atomic Settlement Works

On-chain atomic settlement requires two things to function:

- The asset leg. The financial instrument being traded, whether a bond, equity, fund share, or real-world asset, is represented as a tokenized asset on a blockchain.

- The cash leg. The payment for that asset must also exist on-chain, typically as a regulated stablecoin or a tokenized bank deposit.

When both legs are tokenized on the same ledger, a smart contract can execute the exchange in a single transaction. The contract holds both parties' assets in escrow. It verifies that both the asset and payment are present and valid. Then it executes the swap instantly.

If either party fails to deposit their side of the trade, the transaction reverts. The entire operation is atomic.

This is why the cash leg matters so much. A tokenized bond can move on-chain in seconds. But if the corresponding payment still travels through traditional banking rails, the transaction cannot be truly atomic. The settlement speed is limited by the slowest leg. For atomic settlement to work end-to-end, both the asset and the cash must exist on the same infrastructure.

Why Stablecoins Are Critical to Atomic Settlement

Stablecoins provide the on-chain cash leg that atomic settlement requires. A regulated stablecoin like USDC or a tokenized bank deposit like JPM Coin gives counterparties a digital dollar that settles on the same ledger as the tokenized asset. Without it, atomic settlement is incomplete.

For financial institutions, regulated stablecoins solve three specific problems in the settlement stack:

- Speed: Stablecoin transfers finalize in seconds, regardless of the time of day or the banking calendar. A cross-border payment that takes two to five business days via SWIFT can settle on-chain in under a minute.

- Certainty: Stablecoin transactions are irreversible once confirmed. There is no chargeback window, no pending status, no reversal risk. This is what makes the "atomic" part possible. Both legs of a DvP transaction must be final for the smart contract to execute.

- Compliance: Regulated stablecoin-based payments powered by regulated infrastructure providers come with KYC, AML screening, and audit trails built in. This is non-negotiable for institutional adoption. A settlement system that cannot demonstrate compliance to regulators is a non-starter.

Atomic Settlement vs. T+2: A Direct Comparison

| Factor | T+2 Settlement | Atomic Settlement |

|

Settlement time |

2 business days |

Seconds to minutes |

|

Counterparty risk |

Open for 48+ hours |

Eliminated at execution |

|

Capital efficiency |

Billions locked in collateral |

Capital freed immediately |

|

Operating hours |

Business days only |

24/7/365 |

|

Reconciliation |

Manual, multi-system, batch |

Real-time, single ledger |

|

Intermediaries |

Custodians, CCPs, transfer agents |

Smart contracts |

|

Error handling |

Manual correction over days |

Auto-revert on failure |

Real-World Progress: Banks Are Already Building This

Atomic settlement is not theoretical. Major financial institutions are actively deploying the infrastructure.

JPM Coin (JPMorgan)

JPM Coin is the first bank-issued U.S. dollar deposit token. It launched on Coinbase's Base network in November 2025 and expanded to the Canton Network in January 2026. It represents a direct claim on deposits held at JPMorgan and operates only with whitelisted wallets under full KYC controls.

Project Guardian (MAS)

The Monetary Authority of Singapore's initiative published a DvP settlement guide for DLT-based debt securities in 2025. It brought together policymakers, banks, and infrastructure providers to define how tokenized bonds and funds can settle atomically under existing regulatory frameworks.

Project Agora (BIS)

Seven central banks and over 40 private institutions are building a multi-currency unified ledger. A key design goal is embedding compliance checks at payment origination and sharing them across institutions, directly targeting redundant AML and KYC screening as the primary source of cross-border settlement delays.

How Transak Closes the Cash Leg Gap

The bottleneck in atomic settlement is the cash leg. Asset tokenization is solvable. Smart contracts are mature. What is missing for most institutions is compliant, regulated on-chain money that plugs into a settlement workflow without months of licensing work and millions in build cost. This is what Transak provides.

Transak is the regulated payments infrastructure for stablecoins. A single API connects financial applications to fiat-to-stablecoin conversion across 64 countries, with licensing, identity verification, AML screening, and fraud monitoring built into every transaction. Over 600 applications use it today, serving more than 10 million end users. For institutions building atomic settlement workflows, this means the cash leg arrives pre-vetted and on the same chain as the tokenized asset.

Talk to our team and explore how stablecoins can fit into your payment flows.