Takeaways

A migrant worker in the US sends $500 home to the Philippines on a Friday afternoon. The money disappears into a correspondent banking chain, hopping through an intermediary in New York, clearing through a nostro account in Singapore, and finally landing in a local bank in Manila.

Five days, three intermediaries and $32 in fees later, the family gets their share on Wednesday.

This has been the default experience for the global remittance market still running on a system designed in the 1970s.

Yet, the technology to settle that same transfer in under ten minutes, for less than a dollar in fees, already exists.

Why Traditional Remittance Settlement Is Stuck in a Different Era

To understand why stablecoins matter for remittance, you first need to understand why the current system is so slow.

When a remittance company sends money across borders, the transaction doesn't travel in a straight line. It moves through a chain of correspondent banks, each maintaining nostro and vostro accounts with the next, and every hop adds time, cost, and opacity.

Here's what a typical corridor (say, US to Mexico) actually looks like:

- Sender's bank debits the customer's account

- Correspondent bank #1 (usually in USD) receives the instruction and queues it for batch processing

- Correspondent bank #2 (sometimes a regional intermediary) processes the FX conversion

- Beneficiary bank credits the recipient (often the next business day after receiving final confirmation)

Each of these steps introduces its own settlement window, compliance check, and fee layer. The result is a system where the average cost of sending $200 internationally sits at 6.4%, and certain corridors (Sub-Saharan Africa, Pacific Islands) exceed 8%.

The delays are structurally expensive. Every day money sits in transit, someone is paying for that float.

What Changes When You Put Stablecoins Underneath

Stablecoins fundamentally compress this pipeline. Instead of moving value through a chain of intermediaries over days, a stablecoin transfer settles on-chain in minutes (sometimes seconds) regardless of the corridor.

Here's why the mechanics are different:

- No Correspondent Chain: Stablecoins move peer-to-peer on a blockchain. There's no intermediary bank sitting on the funds overnight. A USDC transfer from a wallet in New York to a wallet in Manila happens in one atomic transaction (fully executed or completely reverted).

- No Batch Processing Windows: Traditional rails operate on banking hours. SWIFT messages queue up. ACH runs in batches. Stablecoin networks settle 24/7/365.

- No FX Opacity: In the correspondent model, FX conversion happens at an intermediary bank's rate, which the sender rarely sees upfront. With stablecoins, the conversion happens at the off-ramp that is transparent, competitive, and visible to the platform.

- Near-Zero Transfer Cost: Sending $500 in USDC on Solana or a Layer 2 like Base costs fractions of a cent. Compare that to the $15–40 in fees that a traditional wire or remittance transfer eats up.

What took 2–5 business days now takes 2–10 minutes. What cost 6.4% now costs under 1%. And the remittance company doesn't need to maintain nostro accounts or pre-fund corridors.

How Remittance Platforms Actually Integrate Stablecoin Rails

Remittance companies aren't crypto companies. They don't want to run blockchain nodes, manage custody infrastructure, or build compliance engines for digital assets. They want to send money faster and cheaper.

Here’s how the integration model could look like.

Step 1: Fiat On-Ramp (Sender Side)

The sender pays in their local currency (USD, EUR, GBP, etc.) through the remittance platform's existing interface. Nothing changes for the end user. Behind the scenes, the fiat is converted to a stablecoin (typically USDC or USDT) via an on-ramp infrastructure provider.

Step 2: On-Chain Transfer

The stablecoin moves on-chain from the sender-side wallet to the receiver-side wallet. This is the fast part and settlement in minutes or seconds on networks like Solana, Polygon, or Ethereum L2s.

The remittance platform doesn't need to interact with the blockchain directly because the infrastructure provider handles routing, gas fees, and chain selection.

Step 3: Fiat Off-Ramp (Receiver Side)

At the destination, the stablecoin is converted back to the recipient's local currency and deposited into their bank account or mobile money wallet via local payment rails.

This can require local banking integrations, KYC compliance, and real-time FX conversion in each destination market.

Step 4: Reconciliation

The on-chain transaction hash provides an immutable audit trail. Paired with off-chain settlement records, the remittance platform gets end-to-end visibility that's actually better than what correspondent banking offers.

The Real Infrastructure Challenge: Two Problems, Not One

If stablecoin rails are so obviously better, why hasn't every remittance company switched already?

Because cross-border stablecoin remittance is two completely different infrastructure challenges that happen to sit at opposite ends of the same transaction.

Problem 1: Origination (Getting Money In)

On the sending side, remittance platforms need to convert local fiat into stablecoins. This means integrating with local payment methods while handling KYC/AML compliance in each sending market.

The complexity is that every sending market has its own licensing requirements, payment method ecosystem, and compliance standards. An on-ramp that works in the US (ACH, wire, debit card) looks completely different from one that works in the UK (Faster Payments, Open Banking) or Brazil (PIX).

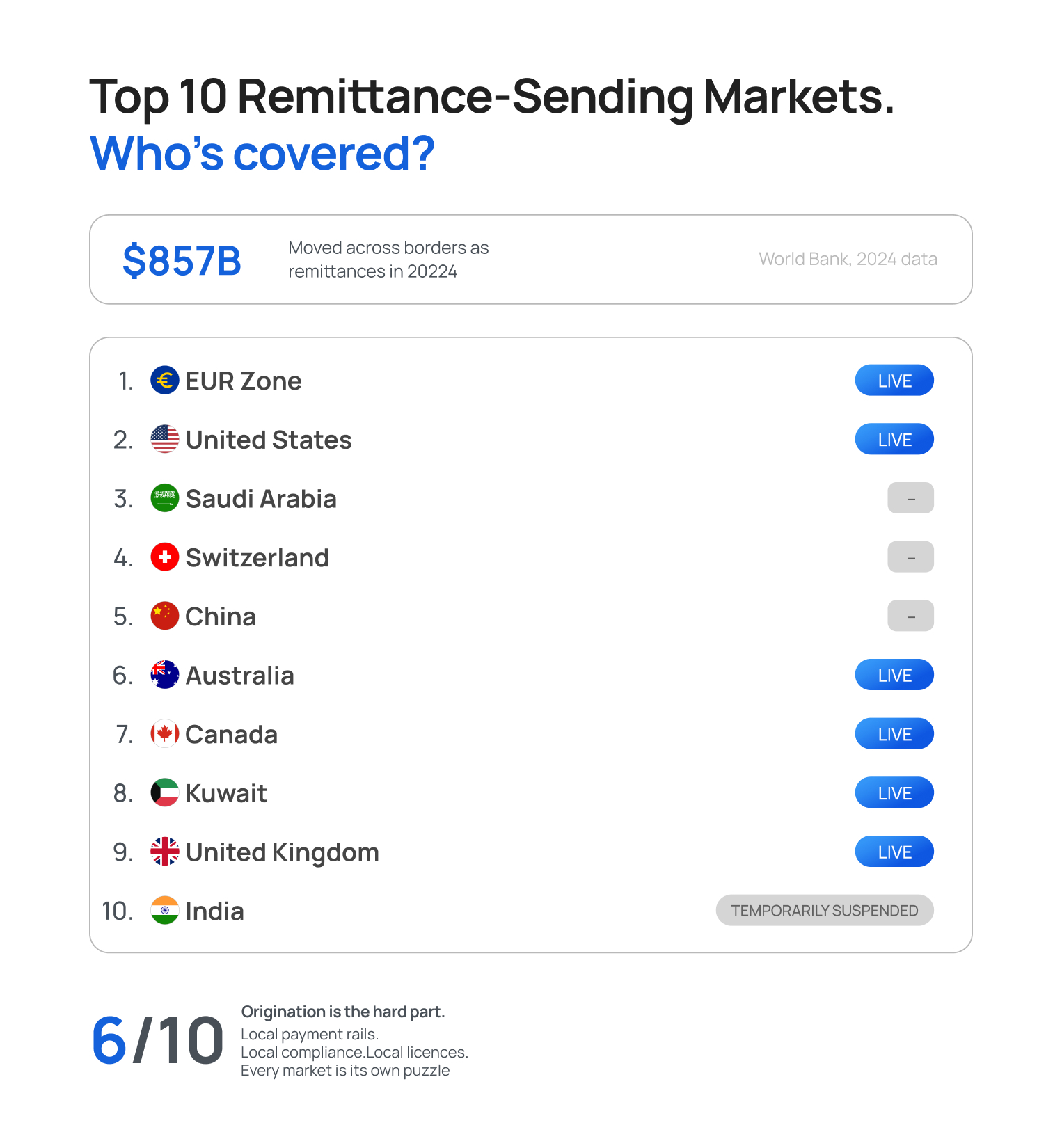

Transak's infrastructure covers the sending side across the markets that matter most. Of the World Bank's top 10 remittance-sending markets, Transak supports on-ramp services in 6. That's origination infrastructure across markets responsible for over $406 billion in annual outbound remittances.

Problem 2: Last-Mile Delivery (Getting Money Out)

The receiving side is a whole different game in itself. Converting stablecoins back to local currency and depositing into a bank account requires deep local payment rail integrations in each destination market.

Each market has its own banking APIs and settlement behavior, KYC/AML requirements, FX conversion mechanics, and failure modes. Building this in-house means maintaining relationships with local banks, payment processors, and regulators across dozens of countries.

Why the Infrastructure Partner Model Works

Rather than trying to solve both problems from scratch, which is a multi-year, multi-million-dollar project, remittance platforms work with infrastructure providers who've already built, licensed, and maintained these integrations.

For origination, Transak provides the regulated fiat-to-stablecoin on-ramp across key sending markets through a single API. We handle local payment method integration, multi-level KYC, and compliance so that your remittance app’s existing user experience stays untouched while stablecoins move underneath.

For last-mile delivery, the stablecoin-to-fiat off-ramp connects to local payment rails in destination markets, handling FX conversion and payout to bank accounts or mobile wallets. See Transak's full global coverage here.

The result is that remittance platforms can start capturing the speed and cost benefits of stablecoin rails in their highest-volume sending corridors without waiting for full bilateral coverage across every market.

The Regulatory Tailwind

One of the biggest historical objections to stablecoins in remittance was regulatory uncertainty. That objection is rapidly disappearing.

- United States: The GENIUS Act established a federal framework for stablecoin issuance and reserves, giving enterprises the legal clarity they needed to build on stablecoins.

- European Union: MiCA (Markets in Crypto-Assets Regulation) created a comprehensive licensing regime for stablecoin issuers and service providers, making stablecoins legally usable financial instruments across 27 member states.

- UAE: The Central Bank of the UAE has approved a regulatory framework for stablecoins, with a particular focus on enabling cross-border payments.

- Singapore: MAS (Monetary Authority of Singapore) finalized its stablecoin regulatory framework, establishing reserve and redemption requirements that align stablecoins with existing payment instruments.

For remittance companies, this regulatory clarity is the green light. Working with a compliant infrastructure partner means the licensing and regulatory burden doesn't fall on the remittance platform itself.

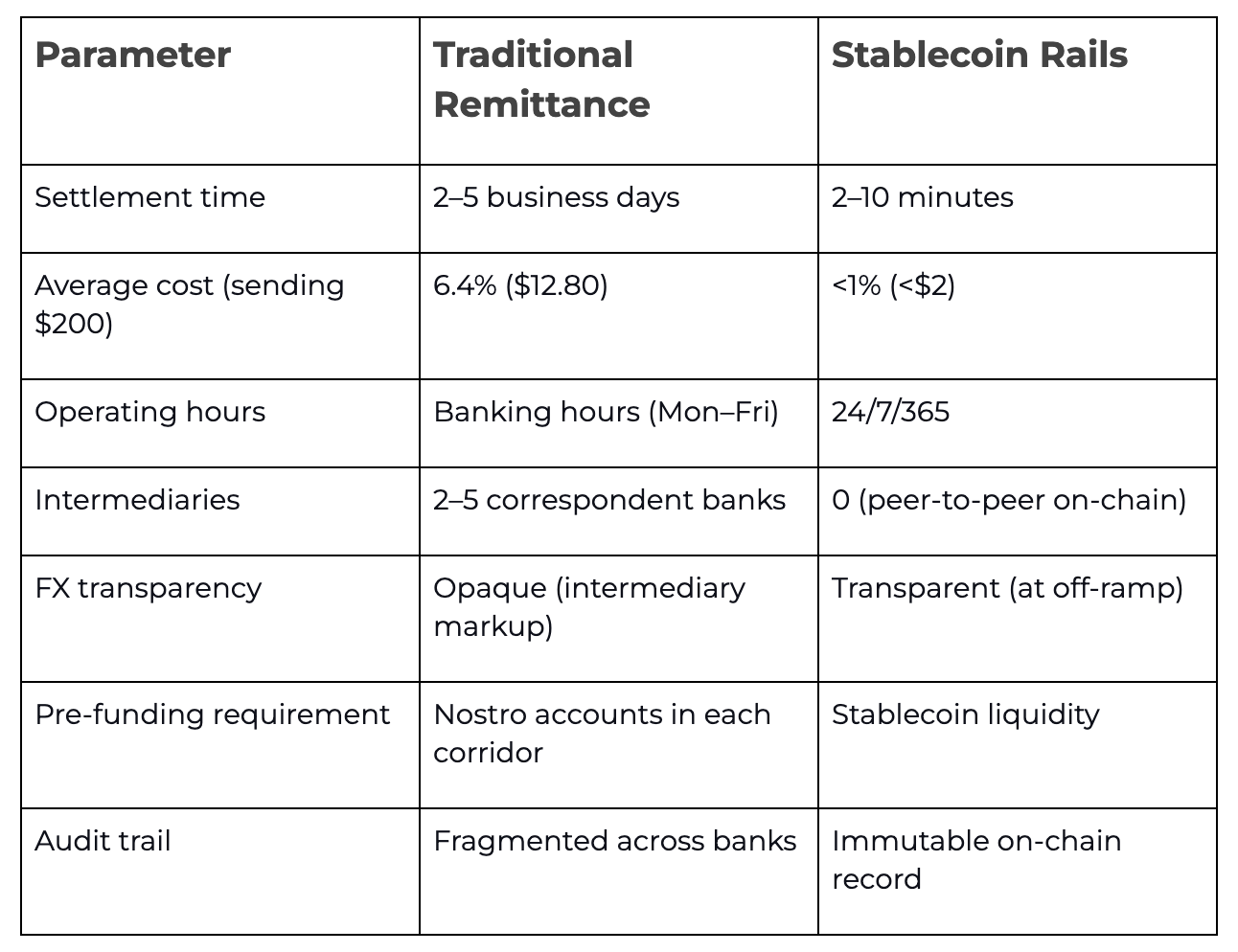

Stablecoin Settlement Speed: A Direct Comparison

Let's put the numbers side by side.

The speed difference alone is transformative. But the real business case is in the combination: faster settlement frees up working capital, lower fees improve margins or pass savings to customers, and 24/7 availability means no more "your transfer will process on the next business day."

What the Best Stablecoin Infrastructure for Remittance Companies Looks Like

Not all infrastructure is created equal. Remittance platforms evaluating stablecoin integration should look for:

End-to-End Coverage: Failure handling becomes easier when one integration handles origination and last-mile delivery. Transak handles both sides of the transaction (fiat in, stablecoin transfer, fiat out) through a single API across many key remittance corridors. See full coverage here.

Global Payment Rail Coverage: The infrastructure needs to support local payment methods in the corridors that matter. This is what makes last-mile delivery actually work.

Built-In Compliance: KYC/KYB, sanctions screening (OFAC, EU, UN), transaction monitoring, and jurisdictional rules should be embedded in the infrastructure layer. Transak is FCA-authorized in the UK and a registered MSB in the United States, with licensed entities across multiple jurisdictions.

Multi-Chain Flexibility: The infrastructure should route transactions across the most efficient chain for each corridor without the remittance platform needing to make those decisions.

White Label Capability: The end user should never see a crypto wallet, a blockchain, or a gas fee. The stablecoin layer should be completely invisible. The remittance platform's brand and UX stay front and center.

The Business Case: Beyond Just Saving on Fees

The obvious pitch for stablecoin rails is cost savings. But the strategic value goes deeper.

Working Capital Efficiency

Traditional remittance locks up capital in nostro accounts across every corridor. Stablecoins are fungible. So, one pool of USDC can service any corridor, any time. That's a fundamental improvement in capital efficiency.

New Corridor Expansion

Opening a new remittance corridor traditionally requires establishing correspondent banking relationships, negotiating FX rates, and pre-funding accounts. With stablecoin infrastructure, a new corridor can be live in days — not months.

Competitive Differentiation

The remittance market is brutally competitive. Offering near-instant settlement at lower fees is a moat. Once customers experience same-day remittance, they don't go back to waiting five days.

Revenue Model Flexibility

Lower infrastructure costs mean remittance platforms can choose to pass savings to customers (competitive pricing), retain them (margin expansion), and/or invest them (better UX, more corridors, loyalty programs).

What Happens Next

The remittance industry is at an inflection point.

Stablecoin transaction volumes are projected to reach $50 trillion by 2030. Cross-border payments and remittance will be one of the largest use cases driving that growth.

Remittance platforms that integrate stablecoin rails now will lock in a structural cost advantage, expand into new corridors faster, and deliver an experience that traditional-rail competitors simply cannot match.

Ready to explore how stablecoin infrastructure can modernize your remittance platform? Talk to our sales team to learn how our APIs can integrate with your existing stack.