Takeaways

Banks are bringing deposits on-chain. Not stablecoins or CBDCs, but actual bank deposits, represented as tokens on a blockchain, backed by the same regulatory protections that have governed commercial banking for decades.

These are tokenized deposits and they could reshape how institutional money moves on chain.

What Are Tokenized Deposits?

A tokenized deposit is a digital token issued by a licensed depository institution on a blockchain.

The token represents a claim on a traditional bank deposit. Economically and legally, it is identical to the money you hold in a bank account. The difference is the form. The token lives on a distributed ledger instead of a bank's internal database.

Tokenized deposits are neither a new asset class nor a synthetic dollar. They are essentially commercial bank money, expressed in a format that can move on-chain, settle instantly, and interact with smart contracts.

The JPMorgan and Oliver Wyman white paper on deposit tokens defines them as "transferable tokens issued on a blockchain by a licensed depository institution which evidence a deposit claim against the issuer."

The paper argues that because deposit tokens are commercial bank money in a new technical form, they fit naturally within the existing banking regulatory framework.

Also Read: Coin vs. Token - What’s the Difference?

How Tokenized Deposits Work

The mechanics are straightforward.

- A customer deposits cash with a bank.

- The bank mints a token on a blockchain representing that deposit claim.

- The token can be transferred peer-to-peer on-chain, used in smart contracts, or held as a cash equivalent.

- The token is redeemable 1:1 for fiat at the issuing bank at any time.

Behind the scenes, the bank holds the deposit just like any other. It is subject to the same capital requirements, liquidity coverage ratios, and risk management standards. If the bank fails, the deposit is insured up to applicable limits (FDIC insurance in the US, for example, covers up to $250,000 per depositor per institution).

The token itself adds new capabilities, like programmability, atomic settlement, and 24/7 transfer availability. But the underlying deposit does not change its nature just because it has been tokenized.

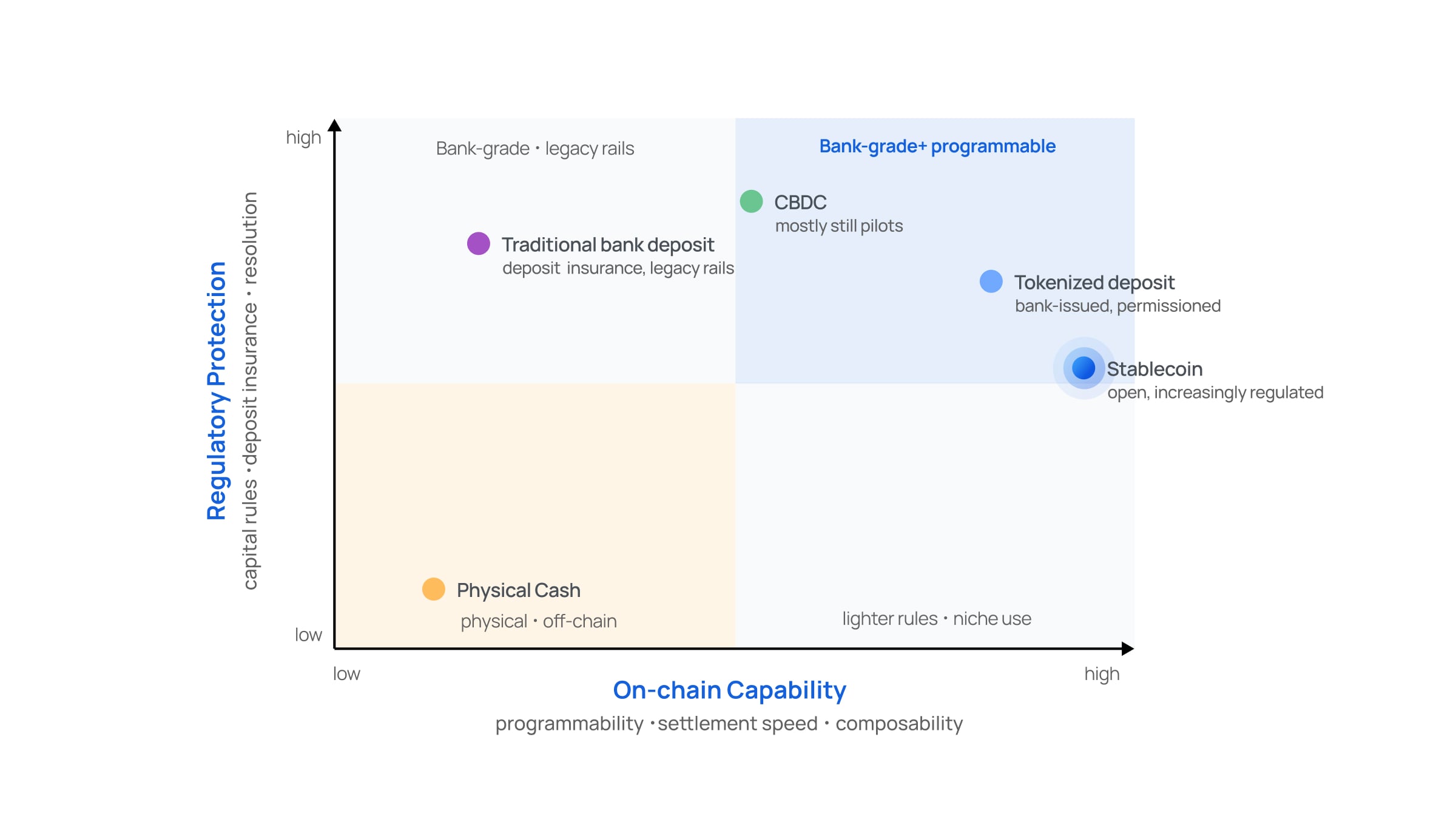

Tokenized Deposits vs. Stablecoins

This is where the conversation gets interesting. Stablecoins and tokenized deposits both aim to provide a stable digital dollar on-chain. But their structures, risks, and regulatory treatment diverge significantly.

|

Comparison Point |

Stablecoins |

Tokenized Deposits |

|---|---|---|

|

Issuer |

Private entities (Circle, Tether, Paxos). |

Licensed depository institutions (banks). |

|

Claim Structure |

Claim against the issuer's reserve assets. |

Claim against the issuing bank's full balance sheet. |

|

Deposit Insurance |

Generally not covered by government insurance. |

Covered by government schemes (e.g., FDIC in the US). |

|

Credit Intermediation |

Moves funding away from private sector lending. |

Keeps funding in the banking system to support credit creation. |

A 2026 staff report by The New York Fed arguing that tokenized deposits may preserve credit intermediation in ways that narrow-band stablecoin models do not.

This is not to say stablecoins lack a role. Stablecoins have built the on-chain liquidity infrastructure that makes tokenized assets viable. They have proven product-market fit for digital dollars.

Also Read: How Stablecoins Fit Into The Modern Treasury Stack

Tokenized Deposits vs. CBDCs

Central bank digital currencies are issued directly by central banks. They are a form of central bank money, the safest type of money in a given jurisdiction.

Tokenized deposits are commercial bank money. They carry the credit risk of the issuing bank, mitigated by regulation and insurance. CBDCs carry no credit risk because they are a direct liability of the central bank.

CBDCs remain mostly experimental. Over 90% of central banks are exploring them, but live projects are still in early pilot phases. Tokenized deposits can be built and deployed today, using existing banking infrastructure and regulatory frameworks.

Real-World Examples

JPMorgan (Kinexys)

JPMorgan’s Kinexys Digital Payments platform (formerly Onyx) has processed material transaction volumes using blockchain deposit accounts on a single-bank ledger.

In 2026, JPMorgan officially rolled out its JPM Coin deposit token on Base, a public blockchain, marking a significant step from permissioned infrastructure toward universal ledger access.

JPMorgan also issued SGD deposit tokens as part of MAS Project Guardian in Singapore, demonstrating peer-to-peer transfers on a public blockchain with compliance controls built into the token smart contract.

HSBC

HSBC launched its tokenized deposit service, HSBC Orion, in 2024. In 2025, it expanded the service to the United States. HSBC also completed a successful tokenized deposit pilot on the Canton Network, demonstrating interoperability between different bank-issued tokens across shared ledger infrastructure.

Citi

Citi has publicly argued that tokenized deposits belong at the core of finance, not at the fringe. In a 2026 position paper, Citi made the case that tokenized deposits preserve the credit intermediation function of banks while enabling the speed and programmability that blockchain provides.

Singapore (MAS Project Guardian)

The Monetary Authority of Singapore's Project Guardian has been a critical testbed. The pilot demonstrated that tokenized deposits could be used in foreign exchange transactions on a public blockchain, interacting with modified DeFi protocols, while maintaining compliance through verifiable credentials and restricted token transfers.

Use Cases for Tokenized Deposits

Payments and Settlement

Tokenized deposits merge payment instructions and value transfer into a single object. Instead of sending information through one channel (SWIFT, ACH) and value through another (correspondent banking chains), the token carries both. This enables direct peer-to-peer settlement, reducing reliance on intermediaries.

For cross-border payments, this is transformative. The correspondent banking system moves $23.5 trillion across borders annually. It costs $120 billion in fees and takes 2 to 3 days on average. Tokenized deposits can compress settlement to minutes, cut intermediaries, and provide real-time visibility into transaction status. This connects directly to the upgrade path that stablecoins offer for correspondent banking.

Programmable Money

Tokenized deposits can be programmed. Conditional transfers based on smart contract logic. Automated interest payments. Intraday lending decisions triggered by predefined conditions. Collateral movement that happens automatically as related trades complete.

The MAS’ Project Guardian used modified DeFi protocols to execute FX transactions with SGD deposit tokens. The smart contracts enforced compliance rules directly in the transaction logic.

Trading and Atomic Settlement

As tokenized assets grow (bonds, securities, real estate, commodities), the need for a blockchain-native cash equivalent to settle trades becomes acute. Tokenized deposits fill this role. They enable atomic settlement, where the transfer of an asset and the transfer of payment happen simultaneously. No settlement lag. No counterparty risk from delayed delivery.

JPMorgan's Kinexys Digital Assets platform has processed over $430 billion in repo transactions using this model since 2020.

Collateral Management

Tokenized deposits can serve as cash collateral in both traditional and digital asset markets. The token form allows collateral to move in real time and automatically as related trades complete, enhancing intraday liquidity management.

Regulatory Landscape

Tokenized deposits sit within existing regulatory frameworks. This is their structural advantage over stablecoins. But the specifics matter by jurisdiction.

- United States: The GENIUS Act, which provides regulatory clarity for stablecoin adoption in the US, also creates a framework that could accommodate bank-issued deposit tokens. The FDIC has signaled that tokenized deposits could be treated as insured deposits if the issuing bank is covered and the product meets scheme requirements.

- Singapore: MAS has been the most active regulator in this space. Its consultation paper proposed that no additional reserve backing or prudential requirements should be imposed on banks that issue tokenized deposits, arguing that existing requirements for capital, liquidity, AML, and technology risk management are sufficient.

- Euro Zone: The EU's DLT pilot regime enables the use of distributed ledger technology for regulated financial services, including the issuance and settlement of tokenized assets. Tokenized deposits could qualify under this framework.

- Japan: Japan's Financial Services Authority has explicitly considered allowing banks to issue stablecoins as deposits, noting that they are already subject to prudential regulations and that holders would be protected by deposit insurance.

Why Tokenized Deposits Struggle to Replace Stablecoins

A common misconception is that tokenized deposits will eventually displace stablecoins by offering the same on-chain utility with real regulatory backing. But that line of thought underestimates how much of a stablecoin's value comes from the things a tokenized deposit cannot copy without ceasing to be a deposit.

Tokenized deposits have four structural problems to begin with:

- They are closed by design. Stablecoins won by being open to anyone. A tokenized deposit has to check KYC, sanctions, and capital rules at the ledger itself, which is why it only runs on approved bank networks. The same rules that make it safe also limit where it can go.

- They only work with pre-approved partners. Banks cannot let their money touch unaudited contracts, so a tokenized deposit can only move between counterparties, jurisdictions, and use cases the issuer has already cleared. That is a much smaller playing field than money that plugs into anything on-chain.

- Every bank issues its own version. USDC is one token from one issuer, accepted everywhere. Tokenized deposits are different at every bank, so a JPMorgan dollar and a Citi dollar are not the same thing until some redemption rail connects them. Users end up having to care which bank issued the money in their wallet.

- They cannot reach most users. Stablecoin demand is strongest in places where local banking is weak or the local currency is unstable. Tokenized deposits need an account at the issuing bank to use them at all. That works for institutions, but it shuts out most retail and emerging-market users.

A few other issues that tokenized deposits fail to solve are the problem of debanking, centralization, and composability.

Also Read: Why Wallets Are Now Becoming Banks

The Road Ahead

The stablecoin playbook for 2026 and beyond is that stablecoins are real financial infrastructure. Tokenized deposits can be a complementary chapter.

Now all platforms can readily leverage tokenized bank deposits. But they can unlock the benefits of stablecoins within weeks.

With stablecoin rails, any private financial application can lower operational costs, improve margins, and improve speed and reliability of their payments.

Talk to our team and explore how stablecoins can fit into your payments flows.