Takeaways

Every crypto payment today asks too much of the user.

On-ramp and off-ramp transactions today are treated as isolated events. The user must re-engage with a checkout process each time, re-confirm rates, and wait through the same pipeline. That works for occasional transactions. It breaks down entirely for use cases like payroll, remittances, or creator payouts, where payments need to flow continuously without human intervention.

Programmatic payments solve this.

What Are Programmatic Payments

Instead of requiring a human to push each transaction through a multi-step funnel, a programmatic payment executes automatically when a predefined condition is met. The user (or system) triggers one action, and everything else happens in the background.

Programmatic Payments vs. Traditional Payment Automation

Traditional payment automation takes a manual workflow and speeds it up. A scheduled bank transfer, a recurring card charge, a batch payroll run. These systems execute on a fixed schedule or in response to a human-initiated command. The logic is rigid, and the payment rails are conventional.

Programmatic payments are event-driven. They respond to signals: a wallet transfer, a smart contract state change, an API call, a bank deposit into a virtual account. The payment logic, compliance verification, conversion, routing, and settlement all execute within a single automated pipeline the moment the trigger fires.

Also read: How Transak Abstracts the Messy Middle of Stablecoin Payments

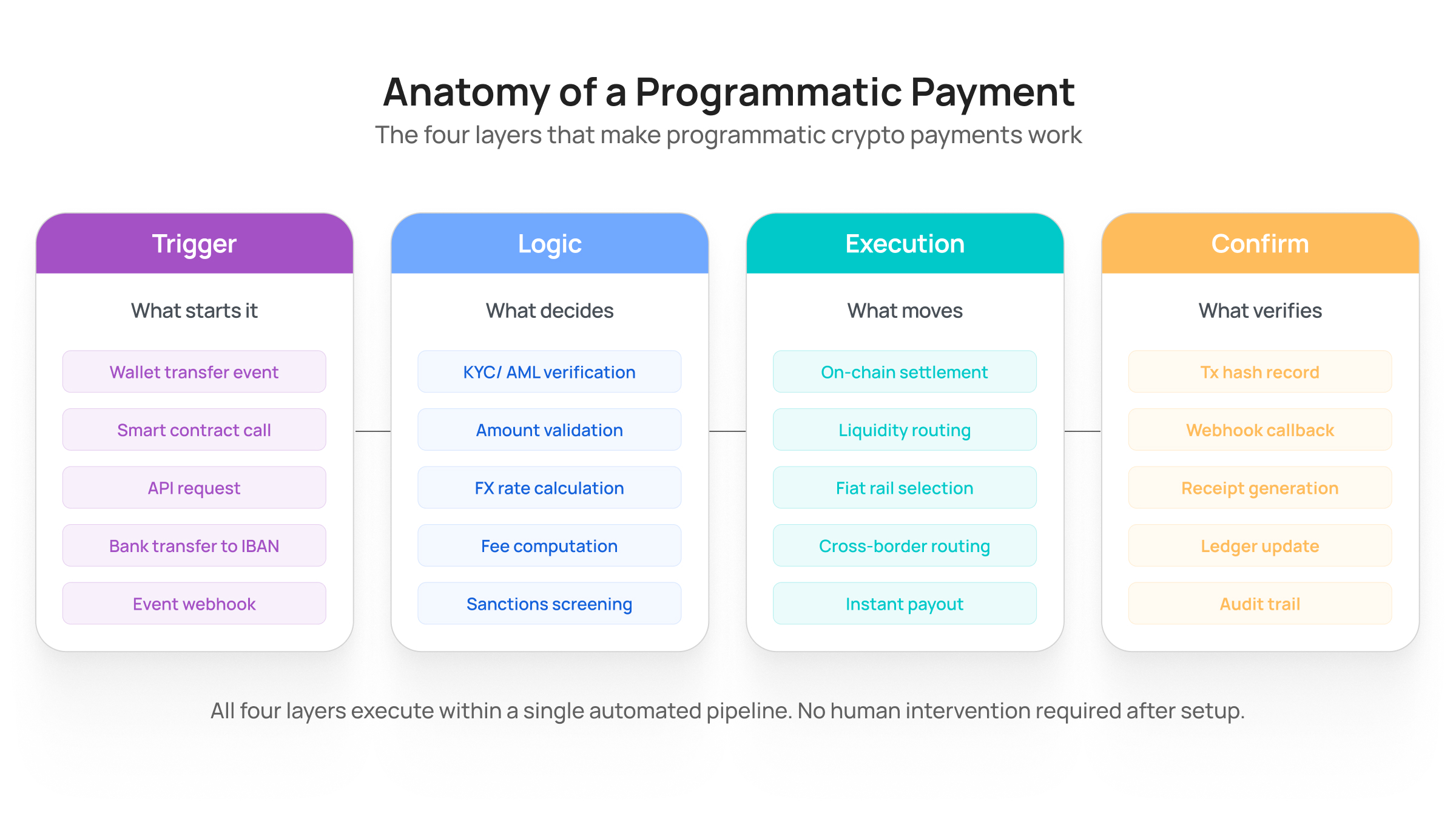

What Makes a Payment "Programmatic"

A programmatic payment has four layers, and all four need to work together for the system to function.

Also read: A Step-by-Step Guide to Blockchain Payments

The Trigger

Something needs to start the payment. This could be a wallet transfer to a dedicated address, a smart contract execution, an API request, or even a standard bank transfer to a virtual account (named IBAN).

The key characteristic is that the trigger is machine-readable. A human does not need to click "confirm" every time.

The Logic

Once triggered, the system evaluates a set of rules.

- Is the sender verified?

- Does the amount fall within permitted limits?

- What is the current FX rate?

- Are there sanctions flags?

This layer is where compliance lives, and it is what separates programmatic payments from simple auto-transfers.

The Execution

The actual movement of value.

In a crypto-to-fiat programmatic payment, this means settling the on-chain transaction, sourcing liquidity, selecting the optimal fiat rail (Visa Direct, SEPA Instant, local bank transfer), and pushing the payout to the recipient's account.

In the opposite direction, a fiat deposit into a virtual bank account triggers an automatic conversion to stablecoins and delivery to the user's wallet.

The Confirmation

The system generates proof that the payment completed, updates internal ledgers, and creates the audit trail. No manual reconciliation required.

Why Stablecoins Make Programmatic Payments Viable

Programmatic payments existed before crypto went mainstream. But stablecoins add something that traditional payment rails cannot: composability at the protocol level.

A USDC transfer on Ethereum or Solana is natively programmable. You can attach conditions to it via smart contracts. You can trigger downstream actions the moment it confirms on-chain. You can route it across borders without correspondent banking chains. And it settles in seconds.

The real opportunity is not in trading volume. It is in payment flows where stablecoins serve as the programmable transport layer between two endpoints.

For a remittance, the sender deposits USDC. The system detects the deposit, verifies the sender, calculates the local currency equivalent, routes to the recipient's bank, and deposits fiat. That entire chain can happen within two minutes. On traditional rails, the same transfer takes three to five business days and costs 6-7% in fees through conventional remittance providers.

For on-ramping, a user receives a personal virtual bank account (a named IBAN). They transfer euros or dollars to that account from their regular bank, just like any domestic bank transfer. The infrastructure detects the deposit, auto-converts it to USDC or another stablecoin at near 1:1 rates, and delivers the tokens to the user's wallet.

.jpg)

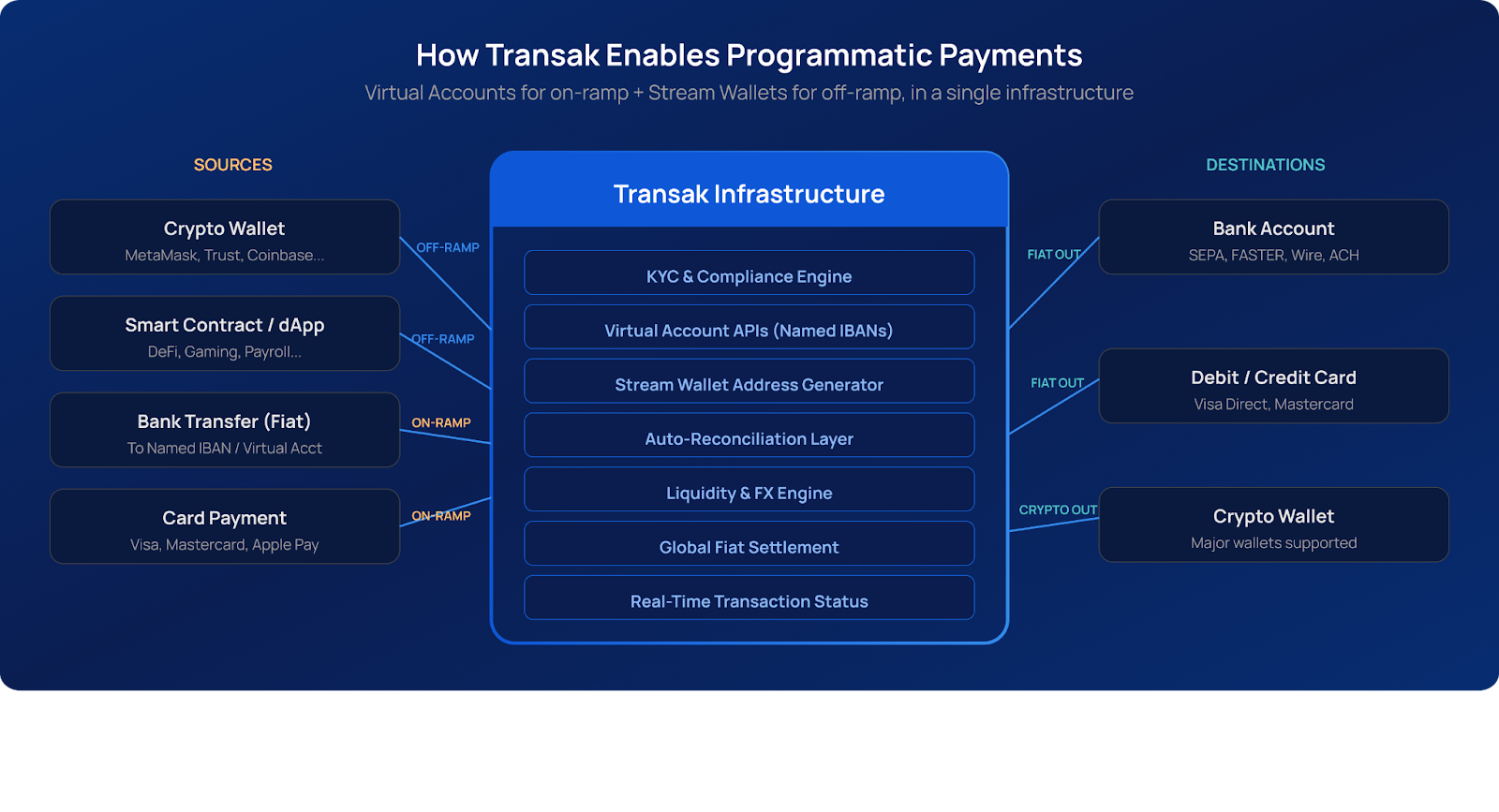

How Transak Enables Programmatic Payments

Transak Stream is our programmatic payment product, built to handle both on-ramping and off-ramping within a single infrastructure. It replaces widget-based checkout flows with persistent, event-driven payment endpoints.

Also Read: Introducing Transak Stream

How It Works

After a one-time setup (KYC verification and payment method configuration), each user receives two types of persistent endpoints:

- Stream wallet addresses for off-ramping. A unique address is generated for each cryptocurrency and network the user selects. Any crypto sent to that address triggers the automated fiat payout. The user's bank account or card receives the funds, typically in under two minutes.

- Virtual bank accounts (named IBANs) for on-ramping. A personal bank account is created for each user and currency. Any fiat deposited into this account triggers delivery to the user's wallet. Because the IBAN carries the user's name, the system auto-reconciles deposits without manual matching.

Both endpoints are persistent and reusable. Once created, they function indefinitely. The user never needs to revisit a widget, confirm a rate, or place an order.

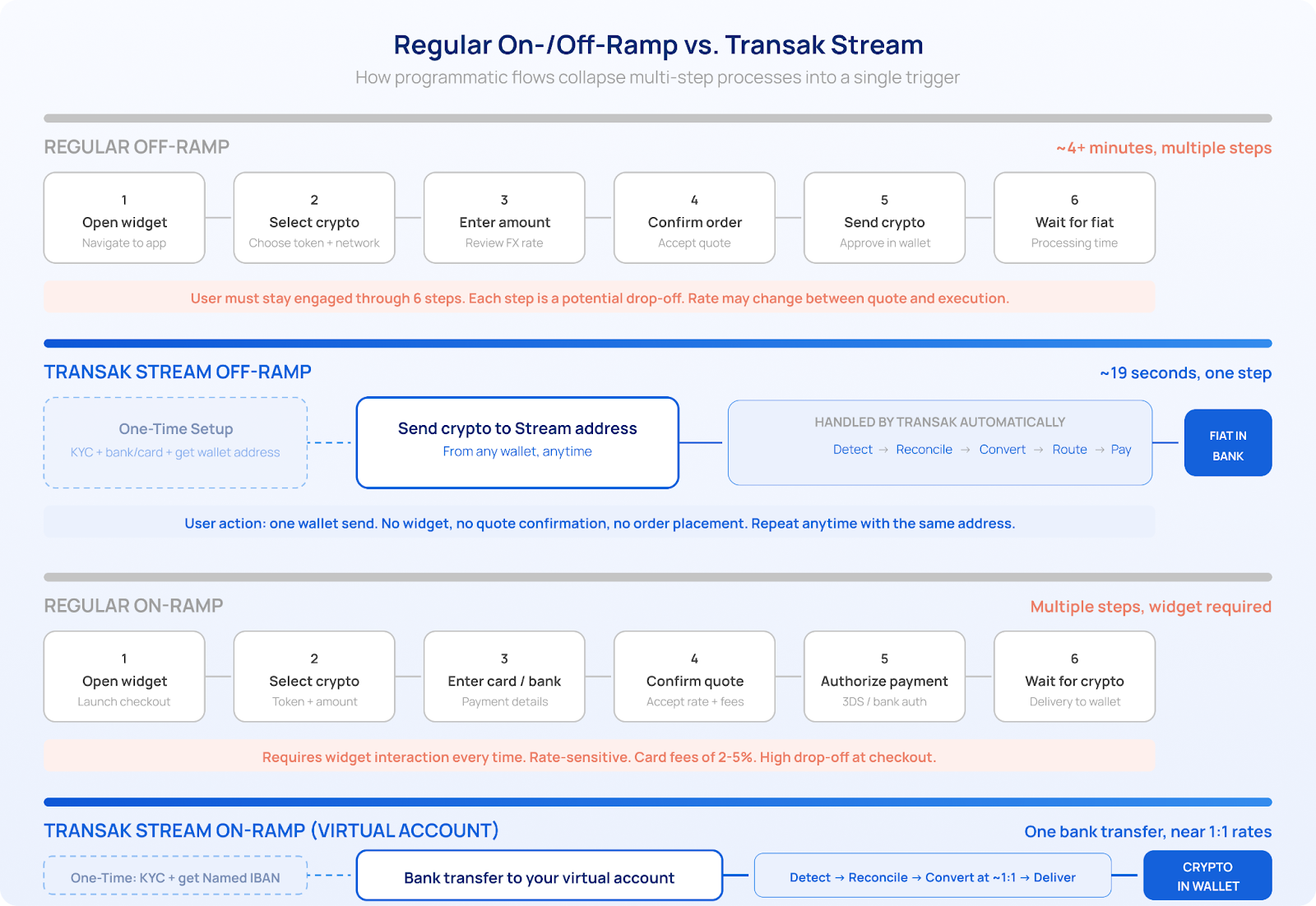

Manual On-/Off-Ramping vs. Transak Stream

The Standard Off-Ramp (Without Stream)

A user who wants to convert crypto to fiat goes through roughly six steps. They:

- open the off-ramp widget,

- select the cryptocurrency and network,

- enter the amount they want to sell,

- review

- accept the quoted exchange rate,

- approve the transaction in their wallet, and then wait for fiat to arrive.

The process takes around four minutes or more, and each step is a potential drop-off. The rate they were quoted may shift between the time they saw it and the time the transaction settles.

The Stream Off-Ramp

The user sends crypto to their Transak Stream wallet address. That is the entire user action. The system detects the incoming transaction, auto-reconciles it, converts at the live rate, and pushes fiat to the user's bank account or card.

In Transak's benchmark testing, this was completed in 19 seconds. There is no widget to navigate, no quote to confirm, and no order to place. The address is reusable, so the second transaction is identical to the first.

The Standard On-Ramp (Without Stream)

Buying crypto through a conventional on-ramp follows a similar multi-step pattern. The user:

- launches the widget,

- selects the token they want to buy,

- enters their card or bank details,

- confirms the quoted price and fees,

- authorizes the payment (often with 3D Secure or bank authentication),

- and waits for the crypto to land in their wallet.

Card-based on-ramps typically charge 2-5% in fees. The user must repeat this process for every purchase.

The Stream On-Ramp (Virtual Accounts)

The user sets up a bank transfer to their personal Transak virtual account, a named IBAN that carries their own name. Funds arrive, auto-convert to the selected stablecoin at near 1:1 rates, and land in the user's crypto wallet.

It works exactly like transferring money between bank accounts. No widget, no card fees, no price confirmation screens. And because the IBAN is persistent, the user can set it up as a standing order in their bank for recurring purchases.

Also read: How to Use Transak Stream

FAQs

How are programmatic payments different from programmable money?

Programmable money refers to digital assets (like stablecoins or CBDCs) with logic embedded directly into the token via smart contracts. Programmatic payments are about the flow of money, using software to automate how and when any type of value moves. You can have programmatic payments without programmable money (like API-driven bank transfers), and you can have programmable money without programmatic payments (like a time-locked token sitting in a wallet). The most powerful systems combine both.

What is the difference between a virtual bank account and a Stream wallet address?

Both serve the same programmatic purpose: they are unique, persistent endpoints assigned to individual users that trigger automated flows when value arrives. A virtual bank account (or named IBAN) is the on-ramp endpoint. Fiat deposited into it auto-converts to crypto. A Stream wallet address is the off-ramp endpoint. Crypto sent to it auto-converts to fiat. Both are part of Transak Stream and together create a bidirectional programmatic payment system.

What compliance risks do programmatic payments introduce?

The primary risk is that speed can outpace oversight if the compliance layer is not built into the programmatic pipeline itself. The solution is to front-load verification. Transak handles this by requiring one-time KYC before issuing any Stream endpoint (wallet address or virtual account), and by running sanctions screening and risk checks on every transaction in real-time, before funds are disbursed.

What happens if I send the wrong cryptocurrency to a Transak Stream address?

Each Transak Stream wallet address is generated for a specific cryptocurrency and network. Sending an unsupported token or using the wrong network can result in lost funds. Transak recommends labeling saved addresses clearly with the crypto and network (e.g., "Transak-USDC-Ethereum") to prevent errors.