Takeaways

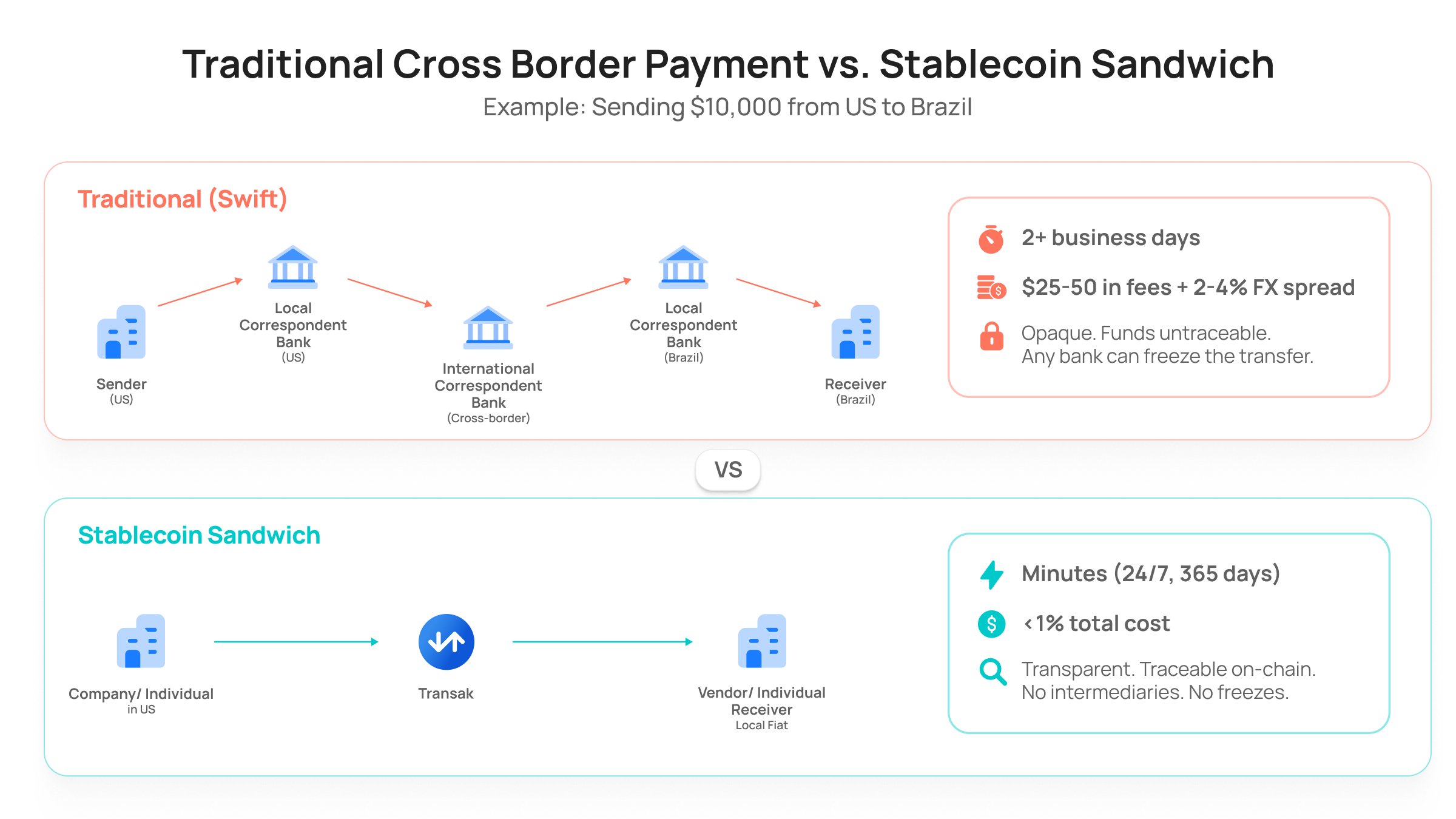

Cross-border payments still run on infrastructure built in the 1970s. SWIFT messages hop between correspondent banks, each adding a fee, a delay, and a reconciliation gap.

A simple overseas transfer that can be completed within seconds in the age of the internet would pass through four intermediaries, take three to five business days, and lose 6-8% of its value to FX markups and fees. And if the amount is tiny, say $40, an additional $20 may be required just in fees - that’s a 50% premium!

The stablecoin sandwich replaces that and empowers both platforms and users. The platforms have more flexibility over their revenue and users retain more of their monetary value.

So, what exactly is the stablecoin sandwich?

What Is A Stablecoin Sandwich

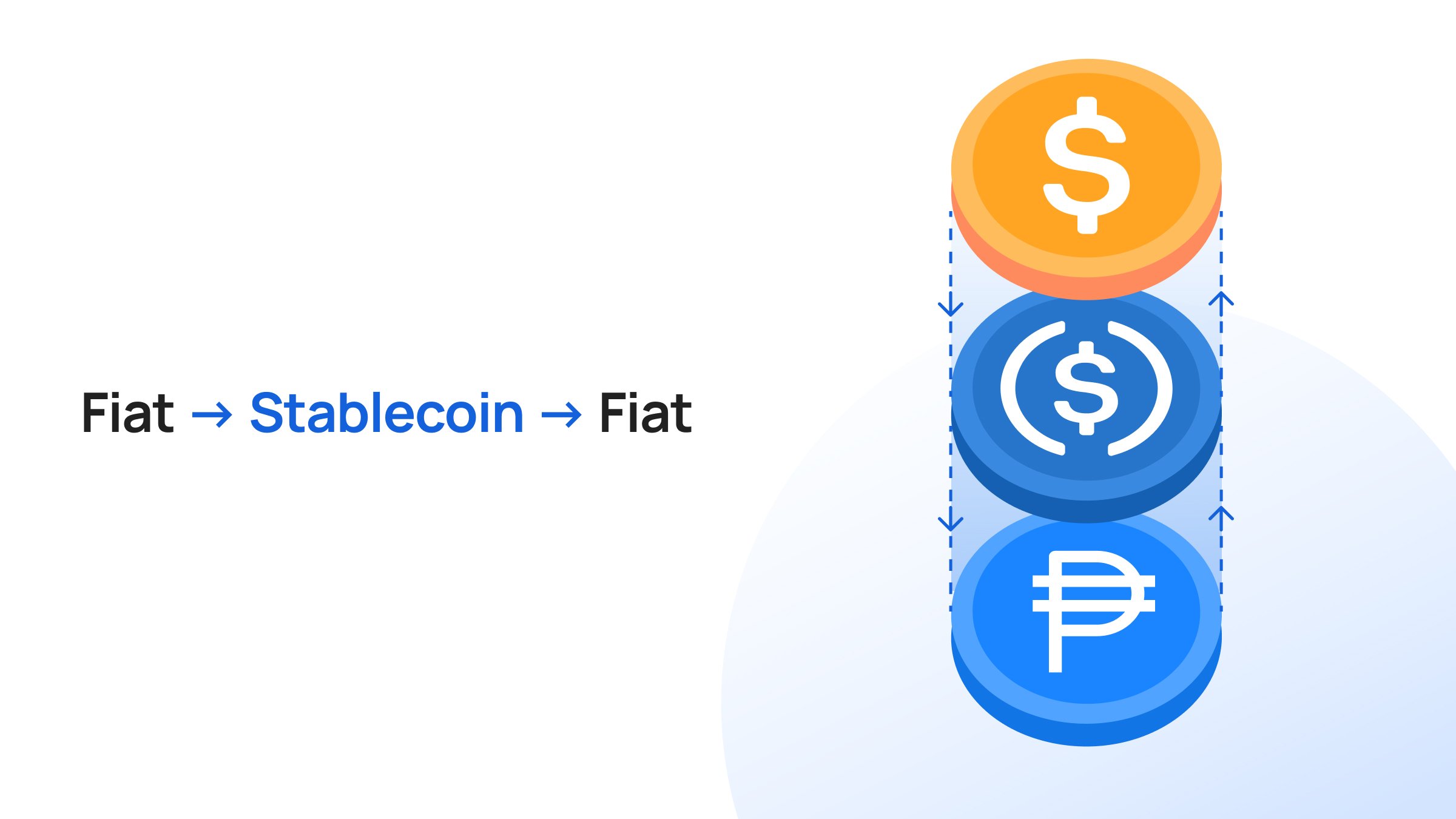

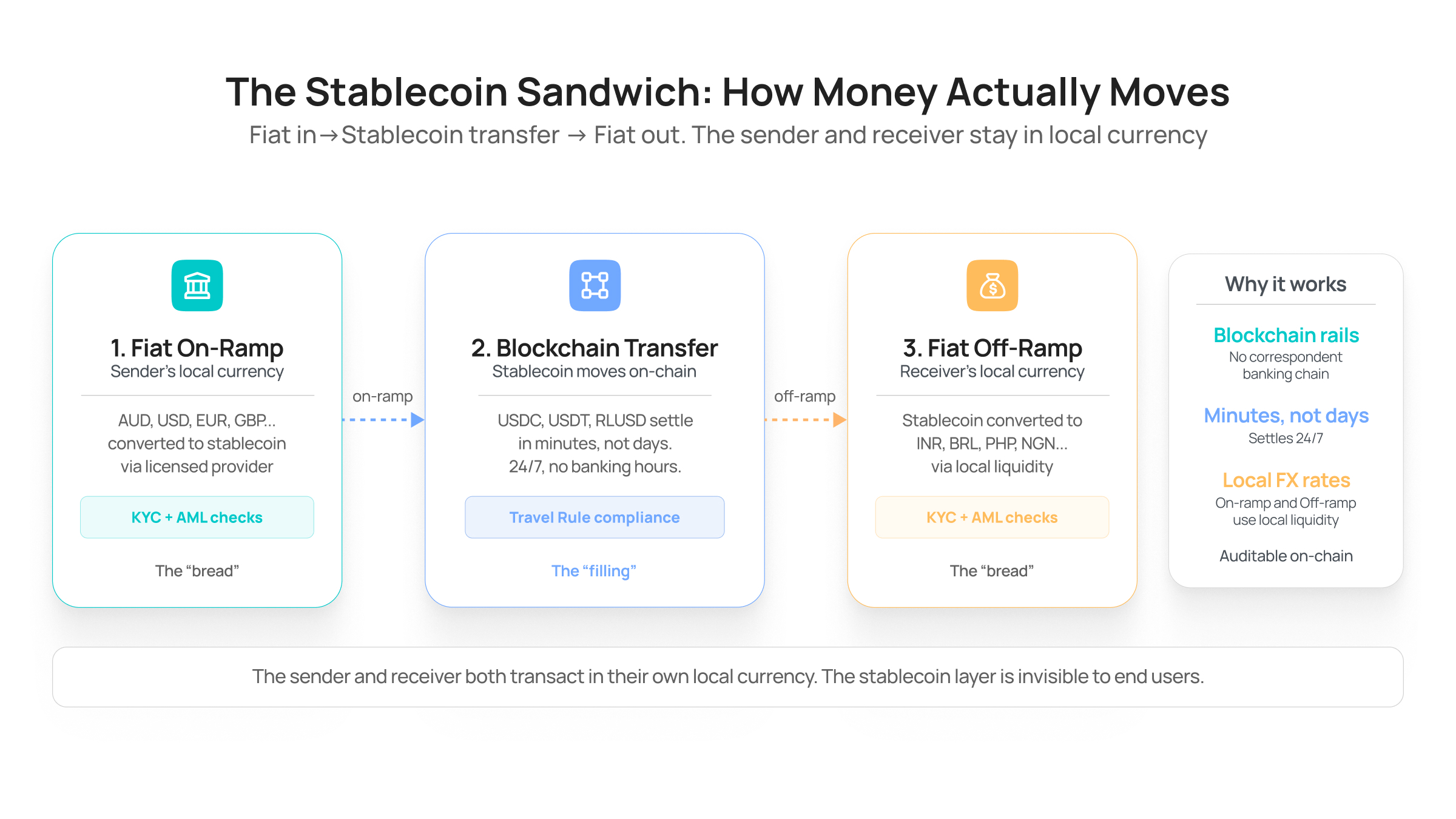

The stablecoin sandwich is a three-step process that modernizes the legacy cross-border payment flow. It converts the sender's fiat into a stablecoin, moves it on-chain, and converts it back to fiat at the destination. The sender and receiver both stay in their own currency. The stablecoin layer is practically invisible to the users.

Also Read: What Is Stablecoin Orchestration?

How The Stablecoin Sandwich Works

A stablecoin sandwich is a payment architecture where value starts as fiat currency, travels as a stablecoin across a blockchain, and arrives as fiat currency in the recipient's local market.

The term was first coined by Ran Goldi, SVP of Payments at Fireblocks, in 2021. Since then, it has become the dominant architecture for stablecoin-powered cross-border payments at companies like Visa, Circle, BVNK, and Thunes.

Also Read: A Step-by-Step Guide to Blockchain Payments

Now, let’s break down the three steps of a stablecoin sandwich flow.

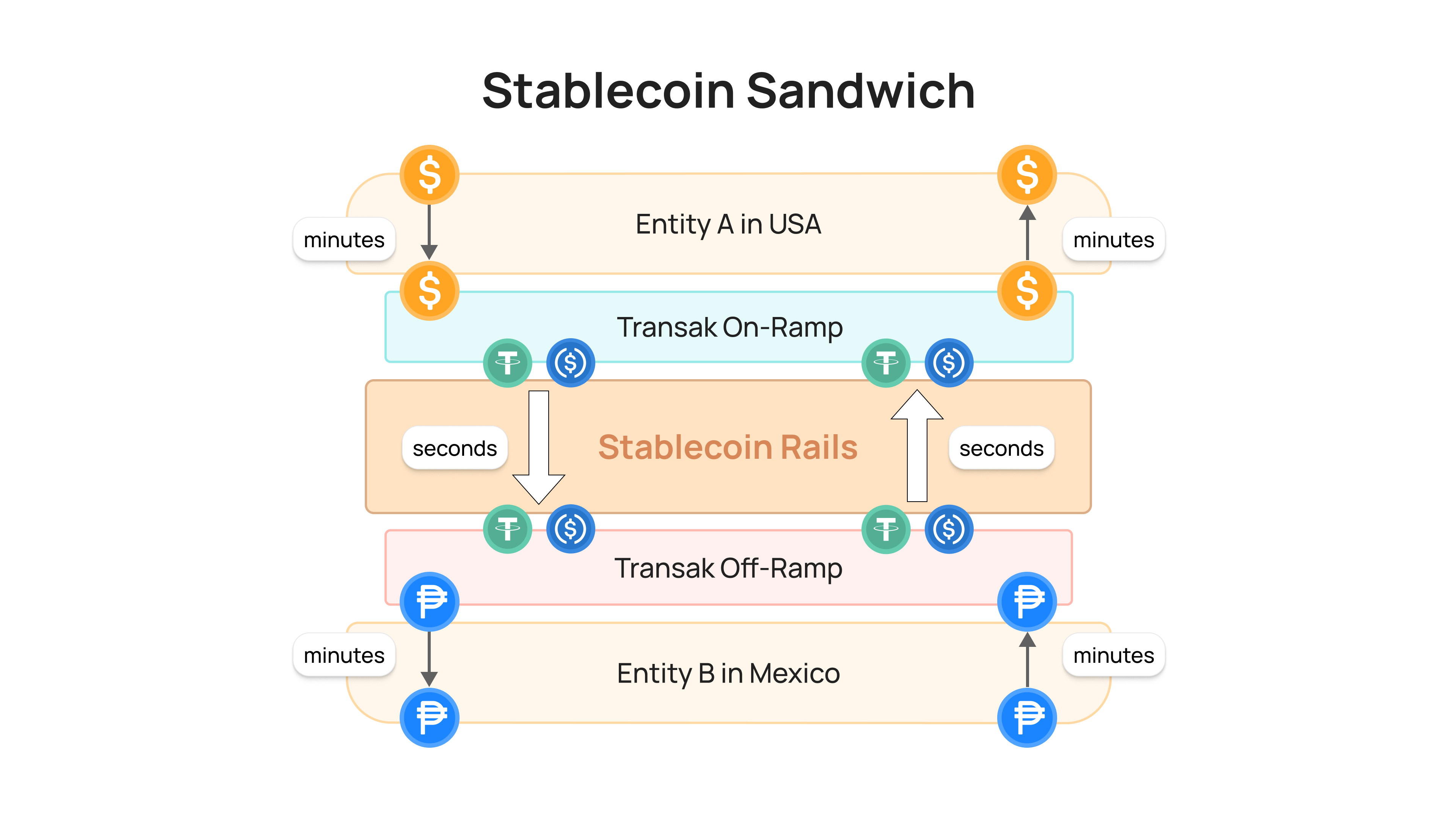

Step 1: On-Ramp (Fiat → Stablecoin)

The sender's local currency (USD, EUR, GBP) is converted into a dollar-pegged stablecoin like USDC or USDT through a licensed on-ramp provider.

KYC, AML screening, and sanctions checks happen here.

The provider uses local payment rails (bank transfer, card, mobile money) to collect fiat and issues stablecoins in return.

Step 2: Blockchain Transfer

The stablecoin moves on-chain from the originating provider to the destination provider.

This is the step that eliminates correspondent banking.

Settlement happens in minutes, runs 24/7 including weekends and holidays, and costs a fraction of a cent on chains like Solana, Tron, or Ethereum L2s. Every transfer is auditable on-chain.

Step 3: Off-Ramp (Stablecoin → Fiat)

At the destination, a licensed off-ramp provider converts the stablecoin into the receiver's local currency (BRL, INR, PHP, NGN) using local liquidity pools.

The receiver gets fiat deposited into their bank account. They may never know stablecoins were involved.

Why The Stablecoin Sandwich Flow Is Faster And Cheaper

Traditional cross-border payments route through a chain of correspondent banks. Each bank has its own cut-off times, reconciliation cycles, and fee structures. The sender's bank may not have a direct relationship with the receiver's bank, requiring one or two intermediaries. Funds can sit in limbo for 48+ hours during holidays or weekends. SWIFT processes ~$150 trillion annually, but the architecture hasn't changed in decades.

The stablecoin sandwich compresses this into two domestic transactions connected by a single on-chain transfer. It removes the intermediary banks, eliminates multi-day settlement windows, and replaces opaque FX markups with competitive local conversion rates on each side. And the advantages for enterprises are very meaningful.

Settlement Speed

Stablecoin transfers settle in under three minutes on most chains. Traditional wires take three to five business days.

For companies managing payroll across 20 countries or settling supplier invoices on tight cycles, this is the difference between capital sitting idle and capital being deployed.

Cost Reduction

Traditional cross-border payments carry 3-7% in combined fees (FX spreads, correspondent fees, receiving bank charges). Stablecoin sandwich flows typically run below 1% total cost. For a company processing, say, $50M annually in cross-border payments, that's a difference of $500K to $2M per year.

Prefunding Elimination

Traditional payment companies must prefund accounts in every destination country to enable same-day payouts. An estimated $27 trillion (~24% of global GDP) sits locked in prefunded accounts globally. The stablecoin sandwich removes this requirement because value moves in real-time. Capital that was previously locked in nostro accounts becomes available working capital.

Visa's stablecoin prefunding pilot on Visa Direct, announced at SIBOS 2025, explicitly targets this: businesses can prefund with stablecoins instead of parking fiat balances in advance, keeping capital productive while ensuring payouts are covered.

24/7 Operations

Blockchain networks don't observe banking hours, holidays, or weekend closures. For companies operating across multiple time zones, this means payouts can be initiated and settled any time. Treasury teams no longer need to plan around cut-off times in Singapore, Frankfurt, and New York simultaneously.

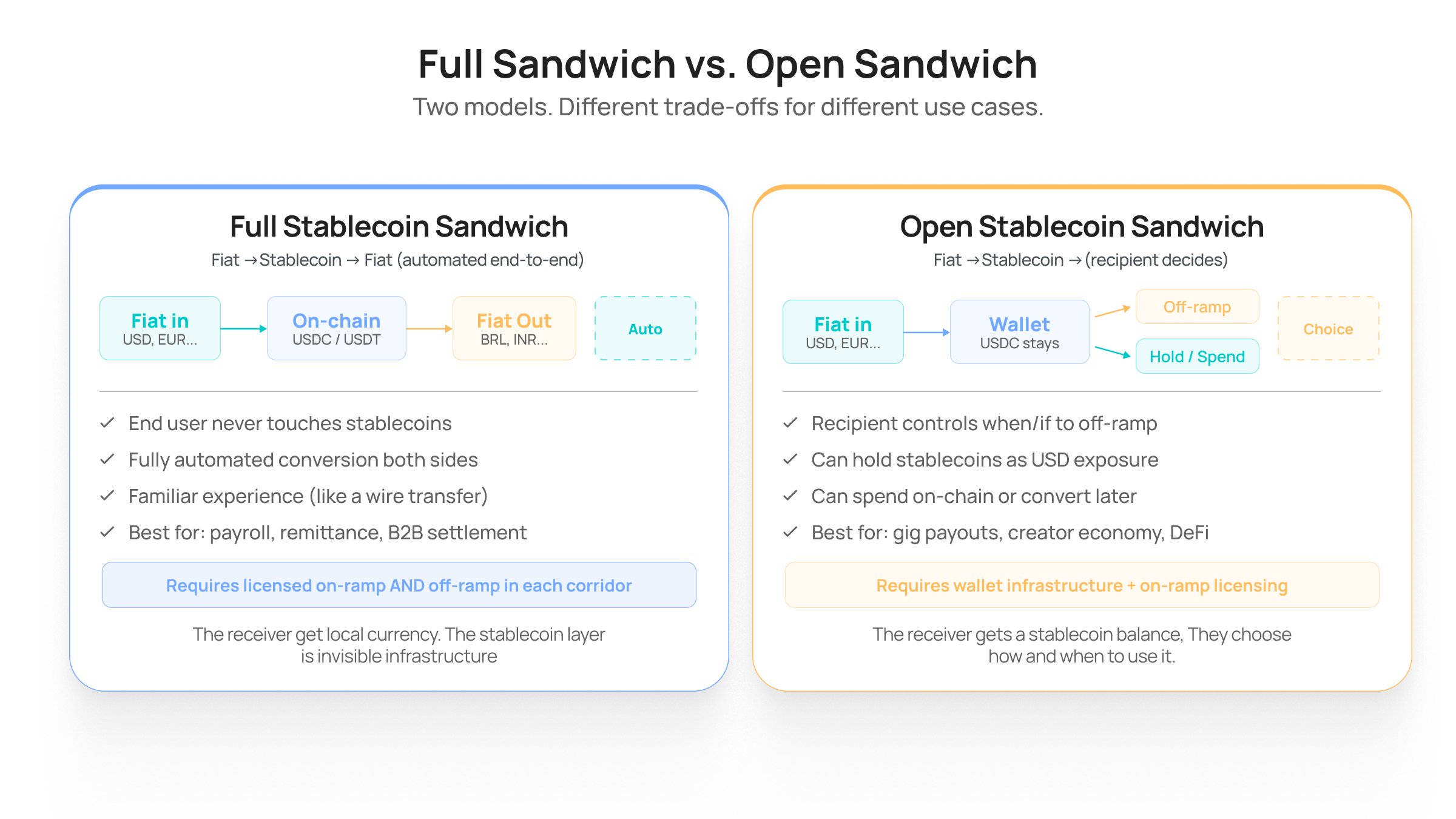

Full Sandwich vs. Open Sandwich

Not every stablecoin sandwich ends in fiat. There are two distinct models:

- Full stablecoin sandwich model

- Open stablecoin sandwich model

Full Stablecoin Sandwich (Fiat In → Stablecoin Transfer → Fiat Out)

In this model, the entire flow is automated and the receiver gets local currency in their bank account.

This is the model used by remittance platforms, B2B payment companies, and payroll providers. The end user on both sides has a fully familiar experience: they send and receive money in their own currency, through their own bank account or mobile wallet. The stablecoin layer is invisible infrastructure, not a user-facing feature.

The full sandwich requires licensed infrastructure on both ends. An on-ramp provider in the originating country and an off-ramp provider in the destination country. Transak provides both.

The full sableclin sandwich model is best for applications like cross-border payroll, supplier settlements, remittances, treasury transfers.

Open Stablecoin Sandwich (Fiat In → Stablecoin Transfer → Customization)

Instead of automatically converting to local fiat, the recipient receives stablecoins in an embedded wallet. They can hold, spend on-chain, or off-ramp to their bank when they choose.

This model is gaining traction in the gig economy and creator economy. A contractor in the Philippines paid by a US company might prefer to hold USDC as dollar exposure rather than immediately converting to PHP, especially during periods of local currency depreciation.

The open sandwich requires on-ramp licensing and wallet infrastructure, but doesn't necessarily need a pre-integrated off-ramp in every destination.

The open stablecoin sandwich model is ideal for: freelancer payouts, gig worker payments, creator economy platforms, and markets where users want dollar exposure.

Compliance Surface In A Stablecoin Sandwich

.jpg)

While the stablecoin sandwich is a very simple flow to visualize, the compliance requirements underneath is the complete opposite.

The on-ramp is the heaviest layer. The provider must hold a license in the sender's jurisdiction (MTL in the US, FCA in the UK, AUSTRAC in Australia, MiCA CASP in the EU), perform KYC/KYB, run AML and sanctions screening, file suspicious activity reports, and maintain records for five to seven years. Each country requires its own license, which is the primary reason most fintechs don't build their own on-ramp.

The transfer layer is where the Travel Rule applies. VASPs must transmit originator and beneficiary information with every virtual asset transfer. Wallet screening, self-hosted wallet identification, and cross-chain bridge monitoring also apply.

The off-ramp is the hardest to execute. It requires local licensing, beneficiary KYC, bank account verification, and FX liquidity management. It's also where fraud risk concentrates because stablecoins settle in minutes, but fiat reversals are slow, so compromised transactions may be cashed out before fraud is detected.

For enterprise buyers evaluating infrastructure, the question is not "does it work?" It's "who holds the licenses in each corridor I need?"

Talk to our team and find out if Transak is the right fit for you.

Where Enterprises Are Using The Stablecoin Sandwich Today

The stablecoin sandwich is already all around us. Stablecoin transaction volume reached $33 trillion in 2025 and B2B stablecoin payments grew from under $100M monthly in early 2023 to over $6 billion by mid-2025.

Cross-Border Payroll

Companies paying contractors and employees across multiple countries use the full sandwich to settle in local currency without maintaining banking relationships in every market. Contractors who previously waited five business days for a wire transfer now receive funds the same day.

Remittances

In Latin America, 71% of stablecoin activity is tied to cross-border payments. For corridors like US-to-Mexico, US-to-Philippines, or Europe-to-Africa, the stablecoin sandwich cuts costs and settlement time dramatically compared to traditional remittance networks.

Treasury and Supplier Payments

Finance teams use stablecoin rails to move money between subsidiaries, settle supplier invoices across borders, and manage liquidity across time zones. The prefunding elimination alone justifies the switch for companies currently locking millions in destination-country accounts.

Card Network Integration

Visa's stablecoin settlement reached a $4.5 billion annualized run rate by January 2026. Card-linked stablecoin spending exceeded $18 billion annualized in early 2026. The stablecoin sandwich is being absorbed into the existing card infrastructure.

Limitations and Risks

The stablecoin sandwich is a significant improvement over correspondent banking, but it isn't without trade-offs.

Last-Mile Liquidity

The off-ramp depends on local fiat liquidity. In developed markets like the US, UK, or EU, this is straightforward. In emerging markets with thin banking infrastructure, limited FX liquidity, or capital controls, the off-ramp can become the bottleneck. Coverage is only as good as the off-ramp network.

Transak provides coverage across key payment corridors globally. Talk to us today and find out if your preferred corridor is supported.

Fiat Dependency at Both Ends

The "sandwich" architecture still relies on traditional financial infrastructure at both endpoints. As long as both ends depend on legacy banking rails, the full potential of blockchain settlement is constrained by the slowest link.

Regulatory Fragmentation

Every jurisdiction has its own licensing requirements, reporting thresholds, and Travel Rule implementation timelines. Running a stablecoin sandwich across 20 corridors means managing 20+ regulatory regimes. This complexity is one of the strongest reasons why platforms prefer Transak rather than building in-house.

Stablecoin Issuer Risk

The sandwich depends on the stablecoin maintaining its peg. If the underlying issuer faces a liquidity crisis, reserve shortfall, or regulatory action, value in transit could be affected. For this reason, enterprise implementations typically use USDC or USDT, which collectively represent 93% of stablecoin market capitalization and have established reserve frameworks.

How Transak Powers the Stablecoin Sandwich

Transak's On-Ramp API handles the fiat-to-stablecoin conversion on the sender side, the stablecoin moves across a blockchain network, and Transak's Off-Ramp API handles the stablecoin-to-fiat conversion at the destination.

Explore the developer docs, integration options, or the compliance page for full licensing details.

Frequently Asked Questions

What is a stablecoin sandwich in payments?

A stablecoin sandwich is a cross-border payment architecture where the sender's fiat currency is converted into a stablecoin (like USDC or USDT), transferred across a blockchain, and converted back into the receiver's local fiat currency. Both sides transact in their own currency. The stablecoin layer handles the cross-border movement.

How is the stablecoin sandwich different from a regular crypto payment?

In a crypto payment, the recipient receives cryptocurrency. In a stablecoin sandwich, the recipient receives local fiat currency in their bank account. The stablecoin is only used as a settlement rail between the on-ramp and off-ramp. The end user may never interact with or even know about the stablecoin layer.

What stablecoins are used in the stablecoin sandwich?

Most implementations use USD-pegged stablecoins, primarily USDC (Circle) and USDT (Tether), which together account for 93% of stablecoin market capitalization. RLUSD (Ripple) and PYUSD (PayPal) are also gaining traction. The choice of stablecoin depends on chain availability, liquidity depth, and regulatory acceptance in the relevant corridors.

What is the difference between a full sandwich and an open sandwich?

In a full stablecoin sandwich, the entire flow is automated where fiat converts to stablecoin and back to fiat at the destination. In an open sandwich, the recipient receives stablecoins in a wallet and decides when or whether to convert to local currency.

How fast are stablecoin sandwich payments compared to SWIFT?

Stablecoin transfers settle in a few minutes on most blockchains and operate 24/7. Traditional SWIFT transfers take three to five business days and are limited by banking hours, holidays, and correspondent bank reconciliation cycles.

Is the stablecoin sandwich legal?

Yes, when operated through licensed providers. The stablecoin sandwich uses the same KYC, AML, and sanctions screening frameworks that apply to any regulated money transmission. Providers must hold appropriate licenses in each jurisdiction and comply with reporting obligations. Regulatory frameworks like the GENIUS Act (US), MiCA (EU), and AUSTRAC reforms (Australia) have formalized how stablecoin payments are supervised.