Takeaways

Cross-border payments, i.e., paying for goods and services from one country recipient to another, are a norm today (but the legacy infrastructure did not consider this evolution when it was being built).

So, when JP Morgan says, ‘Money needs to keep moving — and the blockchain could be the way to achieve it,’ it isn’t commenting on a possibility.

Cross-border payments are the lifeblood of international trade, remittances, and global business operations. Yet, under the hood, they remain painfully inefficient. Money often hops between multiple correspondent banks, incurs high fees, takes days to settle, and is vulnerable to delays, currency mismatches, and compliance friction.

Blockchain promises to rewire this outdated system.

In fact, JP Morgan has already invested billions in blockchain and asset tokenization to provide 24/7, real-time programmable payments.

Today, institutional adoption of stablecoins is at its peak, and 90% of central banks are currently working on a CBDC (Central Bank Digital Currency).

While traditional payment rails still power the majority of international payments, blockchain-led payments are fast becoming the institutional favorite. The US Federal Reserve is testing XRP for instant international transactions.

In this article, we’ll break down what cross-border payments are, where the current system falls short, and why blockchain is the inevitable next step.

What Are Cross-Border Payments?

Cross-border payments refer to financial transactions where the sender and the recipient are located in different countries. These transactions are essential for several activities, like paying international suppliers, sending money to family abroad, investing in global markets and settling trade between corporations.

A Nigerian freelancer working for an American client receiving payment, a shopper buying makeup products from a Korean website, or a British company paying its supplier in Germany – all involve international financial transactions, or cross-border payments.

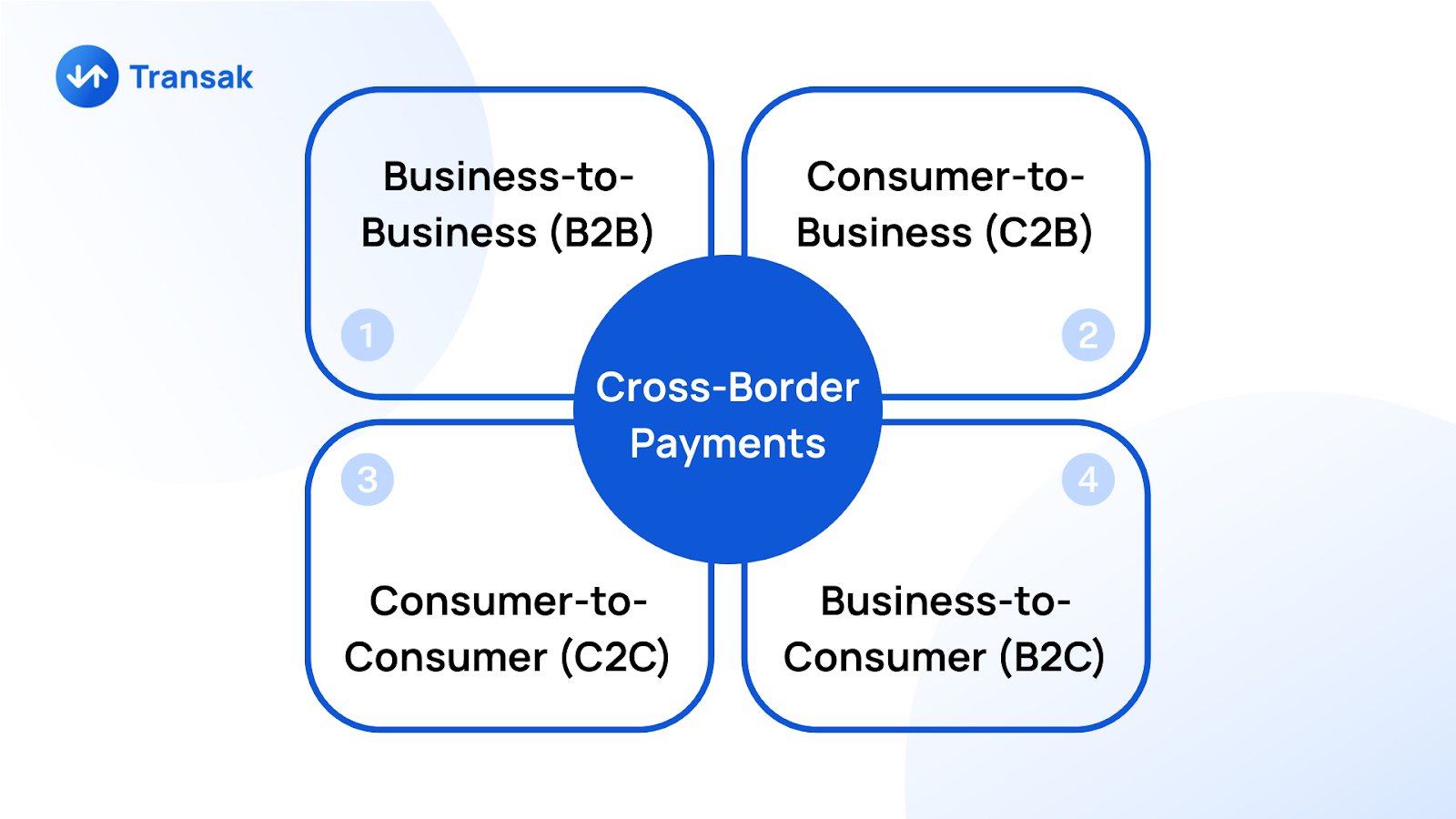

Cross-border payments typically fall into four categories:

- Business-to-Business (B2B): For example, a company in India paying a software vendor in the U.S.

- Consumer-to-Business (C2B): A customer in France purchasing goods from an e-commerce store in China.

- Consumer-to-Consumer (C2C): A migrant worker in the UAE sending money back to their family in Pakistan.

- Business-to-Consumer (B2C): A U.S. company paying remote employees or freelancers in the Philippines.

ACH (Automated Clearing House), wire transfers, credit cards, and cryptocurrencies are among the primary methods for transferring money across borders today. Traditionally, these payments rely on a network of intermediaries (correspondent banks, payment processors, clearinghouses, etc.) to facilitate settlement. But this system is inefficient for modern money movement.

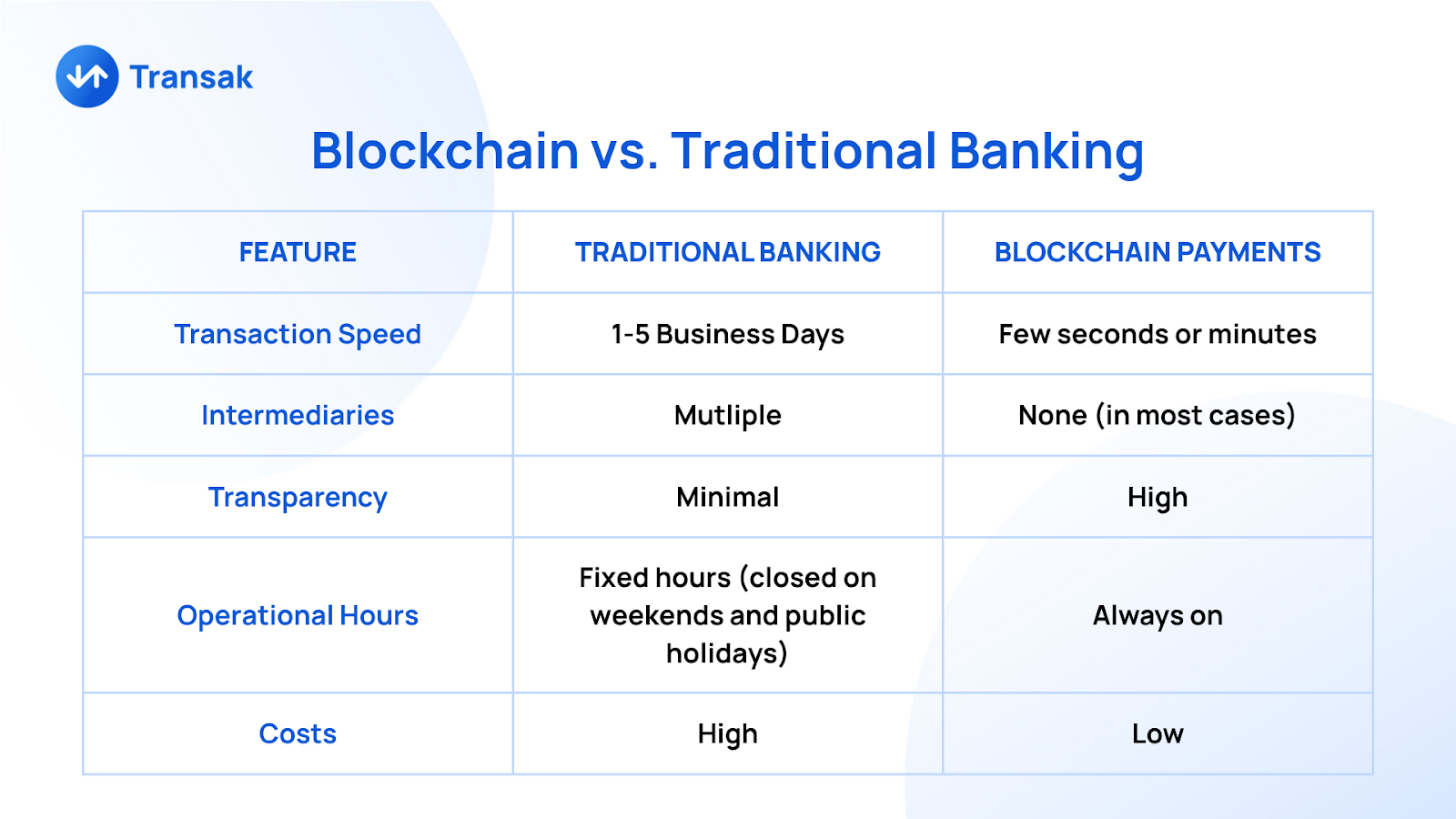

The average cross-border transaction today can take 2–5 business days, cost upwards of 6–10% in fees, and lacks transparency at every stage of the process. That's precisely why the financial world is exploring blockchain as a better alternative.

So, even the world’s largest payment networks, including Stripe, Mastercard, Visa, and PayPal, have already integrated blockchain technology into their payment systems. In fact, blockchain technology is one of the simplest ways for banks and institutions wanting to leapfrog traditional payment rails.

The Inter-American Development Bank, the IDB Lab, LACChain, Citibank Innovations Labs, and ioBuilders collaborated to develop a proof of concept that tested the viability of blockchain in cross-border payments. The execution time was reduced to 10 seconds. For perspective, ACH transfers took up to an hour.

JP Morgan’s blockchain wing conducted a simulation test to check the feasibility of blockchain-based cross-border transactions in Singapore Dollars and Euro CBDCs using a permissioned blockchain in partnership with the Monetary Authority of Singapore and Banque de France.

How Does A Cross-Border Transaction Work?

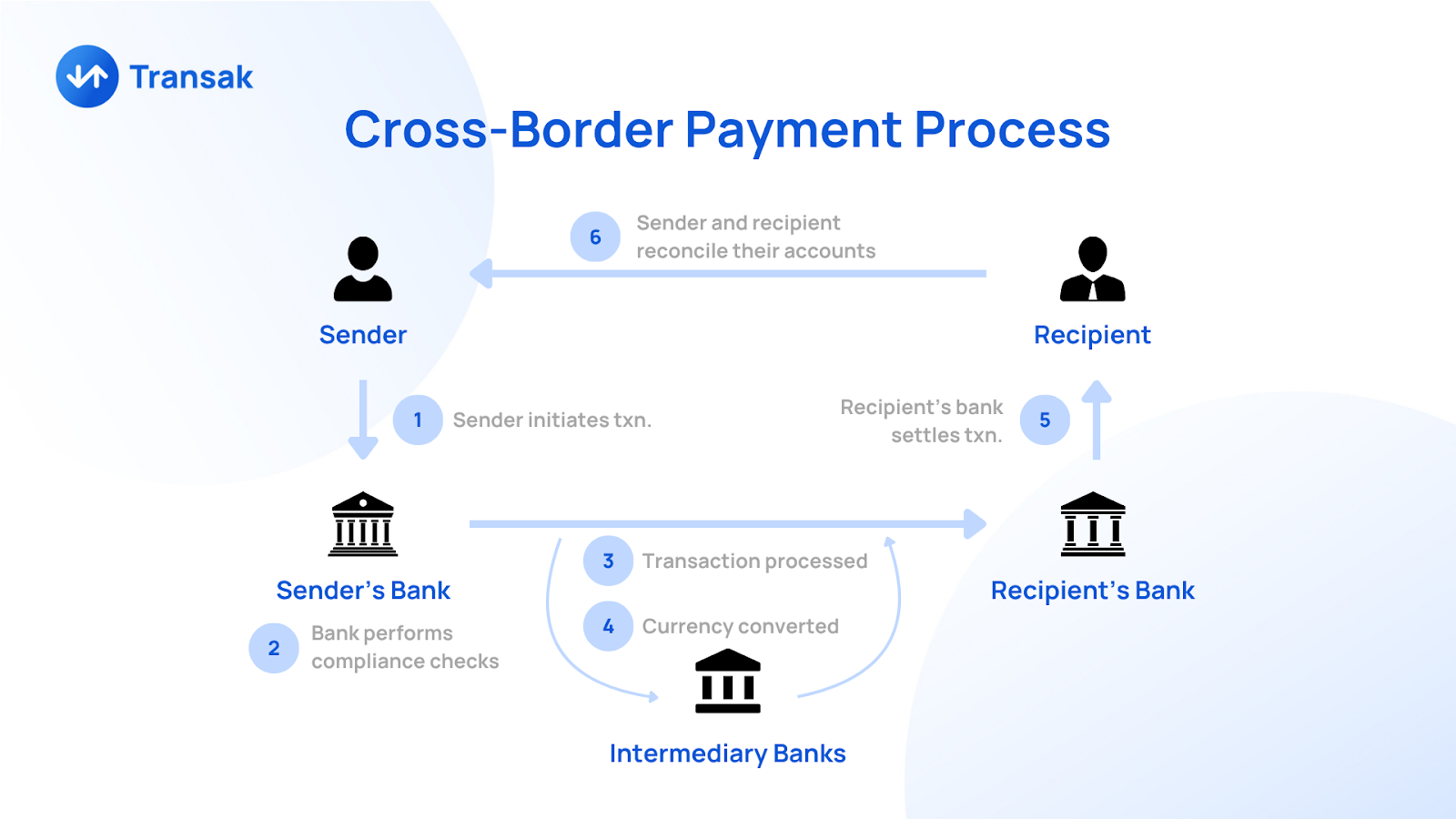

Cross-border payments involve a web of intermediaries, like payment networks, correspondent banks, commercial banks, and fintechs.

This friction exists because each country has its native payment system, banking infrastructure, regulations, and level of technological maturity.

1. Initiation by the Sender

The sender initiates a transfer from their local bank or payment provider. The funds are usually withdrawn in the sender’s local currency (e.g., USD, INR, EUR).

2. Intermediary Banks (Correspondent Banking)

If the sender’s bank doesn’t have a direct relationship with the recipient’s bank, the payment is routed through one or more correspondent banks that maintain nostro/vostro accounts (accounts held on behalf of each other). These intermediaries handle currency conversion and settlement.

Each handoff adds:

- Delays due to banking hours and time zones

- Fees for processing and currency conversion

- Opacity (the sender often doesn’t know where the money is or when it’ll arrive)

3. Foreign Exchange (FX) Conversion

Somewhere along the chain, the funds are converted from the sender’s currency to the recipient’s. This is usually done by an intermediary bank or FX provider, often at marked-up rates.

4. Compliance and Screening

To meet anti-money laundering (AML), sanctions, and know-your-customer (KYC) requirements, multiple checks are performed at each step. These can cause further delays or even block the transaction.

5. Settlement and Delivery

Eventually, the money reaches the recipient’s bank and is credited in the local currency. But this final step could take days, especially if the transaction is flagged or falls on a weekend or holiday.

Challenges Cross-Border Payments Face Today

Besides rising costs, slow and inefficient processes, and rising competition from fintech and cryptocurrencies, banks face a new set of challenges:

Banking Customers Are Highly Demanding

Today’s banking customers want banks to be operational 24/7, 365 days a year, and expect payments to be processed in real-time, at all times, from anywhere across the globe.

Many of the settlement and clearance processes are still human-led and demand a high level of security. To keep up with the peak demand, banks (both the sender and receiver across countries) would have to keep their servers, networks, and even databases operational at all times.

Rise in Service Time Due to Added Security Requirements

Frauds and hacks are on the rise as digital payments become an everyday norm and e-commerce turns the internet into an open marketplace for everyone and anyone to sell and purchase. Here, the payment rails need to be secured and monitored against every kind of known attack.

There's an additional burden on banks due to safety protocols like real-time monitoring, encryption, and multi-factor authentication on one hand, and keeping employees at their desks for longer hours to monitor data centers and address queries and grievances via customer support, on the other hand. The added service time and investment both add to the costs.

Real-Time Settlements Are Still Fictional for Many Banks

A business or a customer is no longer ready to wait till Monday for payment confirmation on an advance they received on Saturday. Real-time settlements, 365 days a year and regardless of the place and time, aren’t yet a possibility.

Banks still deploy manual clearance and settlement processes, which leave room for errors and fraud, and offer little scope for automating transactions or instant settlements.

Rising Middlemen Costs

Transaction fees can go as high as 5% to 10% of the total transaction amount, which makes bank-led international payments an expensive affair. Here’s the cost breakdown of a regular cross-border transaction:

- Correspondent banking fees

- Wire transfer charges

- Foreign exchange conversion fees

- Regulatory and compliance costs

- Payment delays and opportunity costs

On average, consumer cross-border fees come out to be 11% or higher. Half of Citibank’s corporate clients cite high costs as an issue, while 59% report slow speed as a bottleneck.

High Transaction Failure Rates

Customers also report high failure rates as a concern. In the US, the failure rate for cross-border payments was 11%. Transaction failures often occur due to a lack of transparency.

Another reason for transaction failure is due to typing errors. Data analytics company LexisNexis reports that ~50% of payments that don’t complete or are delayed are due to simple data entry problems, such as incorrectly typing the bank name and address, or getting the account numbers, IBAN, or Swift BIC codes wrong.

ISO 20022, and Relevance of Data Insights

Banks have been surviving on the MT standard since 1977. MT did offer a consistent communication system across financial networks. However, the standard had its limitations, and the ISO 20022 standard was introduced to replace it for banking messages. The standard promotes the addition and use of more structured and rich transaction data in payment messages.

The ISO 20022 standard will transform cross-border payments by allowing richer, more structured data to facilitate faster, transparent, and more efficient transactions. The final date of implementation of the standard arrives in November 2025.

To comply with the ISO 20022 standard, the SWIFT network and its institutions are required to include more data and arrange for logical data organization. This, in turn, will improve automation and enable new use cases.

However, the existing message structures lack clarity, and service models for banks are dependent on human interpretation. Only with the adoption of technologies like blockchain can banks streamline data without human intervention.

How Does Blockchain Alleviate These Challenges

Blockchain provides a transparent and immutable record of both transactional and non-transactional data. Its smart contract and tokenization capabilities allow programmability in money, process automation, and seamless value transfers.

Banks Are In Need Of A Technology Upgrade

The financial sector still operates on ancient 60-year-old systems and networks, which are broken, inefficient, costly, and slow. Plus, there are as many individual payment systems as there are countries.

“The idea that settlement processes should take more than a few minutes feels completely foreign in this day and age. It is therefore highly encouraging to see traditional financial institutions embracing blockchain technology in this way,” said James Butterfill, CoinShares Head of Research.

The banks and institutions can’t communicate directly. They need intermediaries. Blockchain technology, on the other hand, disintermediates and decentralizes legacy systems. Blockchains are bank-agnostic, global networks capable of serving as common links between the fragmented financial systems.

Faster Transactions And Cost Savings

Fast transactions are the primary advantage that blockchain technology offers. Blockchain enables banks and institutions to bypass the complex web of intermediaries, facilitating near-instant financial transactions that are validated by a set of validators via a blockchain consensus mechanism and encrypted using private keys and cryptography.

Smart contracts enable faster settlements by triggering payments based on real-time data inputs, thereby reducing the need for manual intervention. Blockchain payments can settle different forms of currency without incurring conversion costs.

For instance, a migrant worker in the US wants to send money to their family in India. Instead of directing money through a wire transfer, they can buy an equivalent amount of USDC and send it over. Transactions made with stablecoins typically incur lower fees compared to traditional banking systems due to reduced dependence on intermediaries.

Unlike banks, blockchain-led financial transactions can be settled 24/7, with zero downtime or maintenance. With code-driven approval and settlement, transaction costs can be reduced by up to 80%. You only pay for the gas fees required to execute a transaction.

Real-Time Settlements

Many countries are developing real-time payment systems that allow for payments to be processed around the clock.

Most of them already have domestic real-time payment (RTP) systems, but cross-border payments have yet to become real-time, due to the technical and legal complexities of integrating systems across all participating countries.

All participants in a transaction would have to link their RTP systems, standardize technical processes, and ensure the participant countries comply with an agreed set of regulations. This isn’t possible unless the participants are close trading partners and witness large bilateral flows. For instance, Singapore has integrated its payment app, PayNow, with India’s UPI network.

Blockchain overcomes these infrastructural and regulatory obstacles. By allowing payments to be settled on-chain, in real-time, in a transparent fashion.

“The use of DLT, alongside other technologies, to enhance settlement speed, improve liquidity management and collateral movements, and reduce costs is an obvious step forward,” says Michele Curtoni, Head of Strategy at SIX Digital Exchange (SDX).

A transaction that was previously settled via multiple intermediaries in 1 to 5 days is now finalized in a matter of seconds.

“Ultimately, where we want to get to is the ability to instantly settle any payment in any currency, anywhere, anytime. And that will probably require using blockchain technology,” says Jason Clinton, Head of Financial Institution Group Sales Europe at J.P. Morgan.

Pre-Validating Payment Information

Blockchain networks are always on, and smart contracts enable the programming of rules and regulations directly into banking processes.

Smart contracts can be used to pre-validate a beneficiary’s account information before the transaction begins. There’s a reduced risk of fraud and failures in blockchain payments.

Banks and institutions can fully rely on blockchain networks to relay information to the destination bank in another country.

Blockchains offer a tamper-proof and permanent record of information. Permissioned blockchains, especially, help banks retain control over the network and also ensure selective privacy of data. These virtues help reduce the concerns around data privacy and security.

Better Liquidity Management

Blockchain payments come with added visibility and real-time tracking, which allows for enhanced liquidity and reconciliation management in cross-border payments. SWIFT conducted an extensive PoC in collaboration with 34 participating banks on Hyperledger Fabric 1.0 in 2018.

The successful PoC was conducted to address Nostro account reconciliation issues in cross-border payments.

Security

Banks and institutions store data in their centralized servers, which increases the risk of single-point-of-failure attacks. A blockchain ledger becomes the single source of shared truth. There’s no room for tampering, and transactions and other data are stored across every node on a blockchain, which removes single-point-of-failure risks.

Blockchains like Stellar Lumens and XRPL have built-in compliance and KYC functionalities, which add to the security. And since money gets stored as digital assets on a blockchain, there are lower chances of fraud or theft.

Case Studies in Blockchain-Led Cross-Border Payments

1. Circle Payments Network (CPN)

CPN is a global cross-border payments network by stablecoin giant Circle that went live on May 21 this year. It acts as a network and coordination protocol that financial institutions can use for exchanging payment instructions and settling international financial transactions on public blockchains.

CPN supports cross-border remittances, enterprise payments, treasury and global cash consolidations, supplier payments, etc. Some of the early adopters include Alfred Pay (stablecoin to fiat off-ramps), Tazapay (compliant fiat disbursements), RedotPay (USDC-based payments in Brazil), and Conduit (on-ramp fiat into USDC in the US and Europe).

2. Stablecoins Need a Special Mention

Cross-border payments remain among the most novel use cases that stablecoins have been known for. Canadian businessman Kevin O’Leary commented on the role stablecoins are playing in cross-border payments, “Crypto will be the 12th sector of the economy within five years ‘cause it’s so productive to the rest of the sectors and just in digital payments.”

You can now transfer currency right across the border without using a bank. That’s a trillion-dollar industry, and it’s ancient, it’s a 60-year-old technology, and really high fees. If you have a wallet in Canada and you have a wallet in the US, you can just do a transaction of the stablecoin.

Stablecoin volumes hit $27.6 trillion last year, surpassing the combined volumes of Visa and Mastercard. Stablecoins have begun to decouple from crypto exchanges and position themselves as a component of real-world financial infrastructure, led by some of the biggest institutions and payment networks. As of 2024, stablecoins accounted for approximately 3% of global cross-border payments volume, with growth expected to reach 20% by 2029.

3. XRP (Ripple)

XRPL is emerging as a trusted alternative to SWIFT in the cross-border payments market. It acts as a bridge asset between different national fiat currencies, and banks love it. It also provides banks with on-demand liquidity solutions for seamless cross-border payments.

Ripple projects that it will overtake 14-20% of SWIFT’s volume in the coming years. XRPL has worked with legacy banks and financial institutions and remains a trusted partner for over 100 entities so far. Vietnam Central Bank has recognized XRP for international payments.

4. Stellar Network

Stellar Lumens offers blockchain payments at a speed of 3.2 seconds and at 90% cheaper costs, has built in KYC/AML in its compliance layer, and positions itself as the universal bridge asset between different fiat currencies.

The Stellar network facilitates $30 million worth of remittances on MoneyGram. BlackRock uses it for instant securities settlement. PayPal is integrating its stablecoin PYUSD with Stellar.

5. BRICS Interbank Payment System

BRICS Interbank Payment System is an initiative that combines BRICS Pay and China’s digital Renminbi (e-CNY) cross-border payment system to ensure a faster and cost-effective cross-border connectivity with 10 ASEAN nations and 6 Middle Eastern countries. It is based on blockchain and CBDCs, and seeks to reduce reliance on the SWIFT network.

The network covers 38% of the global trade volume, and offers a near-instantaneous settlement time of 7 seconds at a 98% slashed fee rate, great for businesses and governments trying to save international transfer costs. It also grants financial autonomy to the BRICS nations over and against the US sanctions and dollar dominance.

A successful use case of this network is the Russia-China trade route, which settles 95% of its trade in Rubles and Yuan.

Challenges of Blockchain Adoption in Payments

1. Fast-But-Fragmented Regulation

Digital‑asset regulation is evolving at warp speed, which would’ve been good if it weren’t happening in an uncoordinated way.

In the U.S., the SEC’s removal of SAB 121 in early 2025 relieved banks from treating crypto as a liability, yet state and federal agencies still lag in clarity.

In the EU, MiCA rolled out in late 2024, setting pan‑European rules, but member states vary in implementation. Meanwhile the EU’s AML Authority flags crypto as the region’s top laundering threat.

Companies face a strategic catch‑22. Innovate using digital rails, or stay in regulatory safe‑mode until global harmonization materializes?

How Transak Helps

Transak is registered as a Money Services Business (MSB) with FinCEN in the U.S., is FCA-registered in the UK, and complies with local regulations in multiple countries. By acting as the regulated layer between fiat and crypto, Transak abstracts away the burden of compliance to allow businesses to integrate crypto features while staying within legal boundaries.

2. Volatility Risk

Holding digital assets exposes treasuries to sharp value swings. Stablecoins promise relief, yet they remain lightly regulated and occasionally fraught.

Tether’s 2021 $41M fine and 63% of crypto-associated crime via stablecoins signal unresolved trust issues.

Treasury teams must now juggle real-time hedging strategies and compliance-grade reserves that are far from the long-term holdings comfort zone.

How Transak Helps

Transak supports multiple regulated stablecoins (like USDC and PYUSD) and real-time conversion between fiat and stablecoins. This gives businesses the option to instantly on-ramp/off-ramp without having to hold volatile assets.

3. Technical Debt

Blockchain payments require more than pressing “Send.” Firms need wallet/custody integration, key‑management security, interoperability with legacy systems, and specialized dev skills.

There are also deeper technical risks—like the fact that smart contracts can’t be easily changed if regulations evolve, or the security issues around connecting different blockchains.

It’s a whole new framework that requires serious technical planning and long-term investment.

How Transak Helps

Transak provides ready-to-use SDKs, APIs, and white-labeled UX components that businesses can plug into their apps or platforms natively. Wallets, dapps, and even centralized platforms can embed Transak’s infrastructure to offer fiat-to-stablecoin services without having to build complex systems from scratch.

4. Compliance Friction

Blockchain may be transparent, but that doesn’t mean it’s automatically compliant. Global rules like the FATF Travel Rule and new EU laws now require businesses to know exactly who’s sending and receiving funds (even on-chain). Compliance with anti-money laundering regulations is critical for blockchain networks handling cross-border payments.

That means firms must build systems to track transactions, screen for sanctions, and report activity in real-time across multiple layers.

Far from being a compliance shortcut, blockchain actually demands more control, and only those with the right infrastructure can keep up.

How Transak Helps

Transak is built for compliance at scale. It handles KYC, KYB, AML checks, transaction monitoring, and even FCA Travel Rule compliance across jurisdictions. Businesses using Transak don’t need to worry about screening or reporting. It’s all built into the platform with regulatory-grade infrastructure.

Conclusion

Blockchain offers a fundamentally better foundation for international money movement. It lets value move at the speed of the internet. The use of stablecoins allows businesses to access new markets and demographics, especially where traditional banking access is limited.

For businesses, this means faster liquidity. For individuals, it means cheaper remittances. For everyone, it means financial access is no longer dictated by geography or legacy infrastructure.

Of course, blockchain adoption isn’t without hurdles. When SWIFT conducted its PoC in 2018, it was quick to comment how further progress was needed on DLT and blockchain technology before banks could enjoy production-grade applications on a large scale.

But with the right infrastructure partners like Transak, these challenges become manageable. Transak abstracts away the messy middle (compliance, fiat ramps, identity verification) so that businesses can focus on building, not battling bureaucracy.

Make the Shift with Transak

If your business is ready to embrace the future of global payments, Transak makes it simple, secure, and compliant from day one.

Don't let outdated payment rails limit your growth.

Build cross-border payments on blockchain with Transak as your trusted partner.