Takeaways

If you've ever been paid by direct deposit or paid a bill straight from your bank account, you've used ACH. You probably never noticed it.

ACH payments quietly move most of the money in the United States. In 2025, the ACH network handled 35.2 billion payments worth $93 trillion.

Banks, credit unions, and other financial institutions rely on ACH transfers for almost everything routine, from direct deposits to bill payments.

This guide explains what ACH payments are, how they work, what they cost, how to send and accept them, and where they fall short.

This article explains what atomic settlement is, why it matters for financial infrastructure, how stablecoins make it practical, and what enterprises need to evaluate before adopting it.

What is an ACH payment?

An ACH payment is a bank-to-bank transfer that moves money electronically through the Automated Clearing House network. It skips paper checks, card networks, and cash.

Banks don't process the transactions one at a time. They bundle ACH transactions into batches and clear them at set points during the business day.

ACH payments are also called ACH transfers or ACH transactions. The terms get used interchangeably.

Almost every bank and credit union in the country can send and receive ACH payments. With so many credit unions and other financial institutions connected, ACH transfers reach nearly any US bank account.

What does ACH stand for?

ACH stands for Automated Clearing House. It's the US financial network that banks and credit unions use to send and receive electronic payments and money transfers.

What is the Automated Clearing House (ACH) network?

The ACH network is the shared rail that nearly every US bank and credit union plugs into. NACHA (National Automated Clearing House Association) writes the rules.

Thousands of financial institutions take part, and each agrees to follow those rules so ACH transfers clear smoothly between them.

Two ACH operators actually move the files.

- One is the Federal Reserve (through FedACH).

- The other is The Clearing House (through its Electronic Payments Network, or EPN).

The system dates to the 1970s, when banks built it to cut down on paper checks. It has grown every year since, from 26.8 billion payments in 2020 to 35.2 billion in 2025 (Nacha).

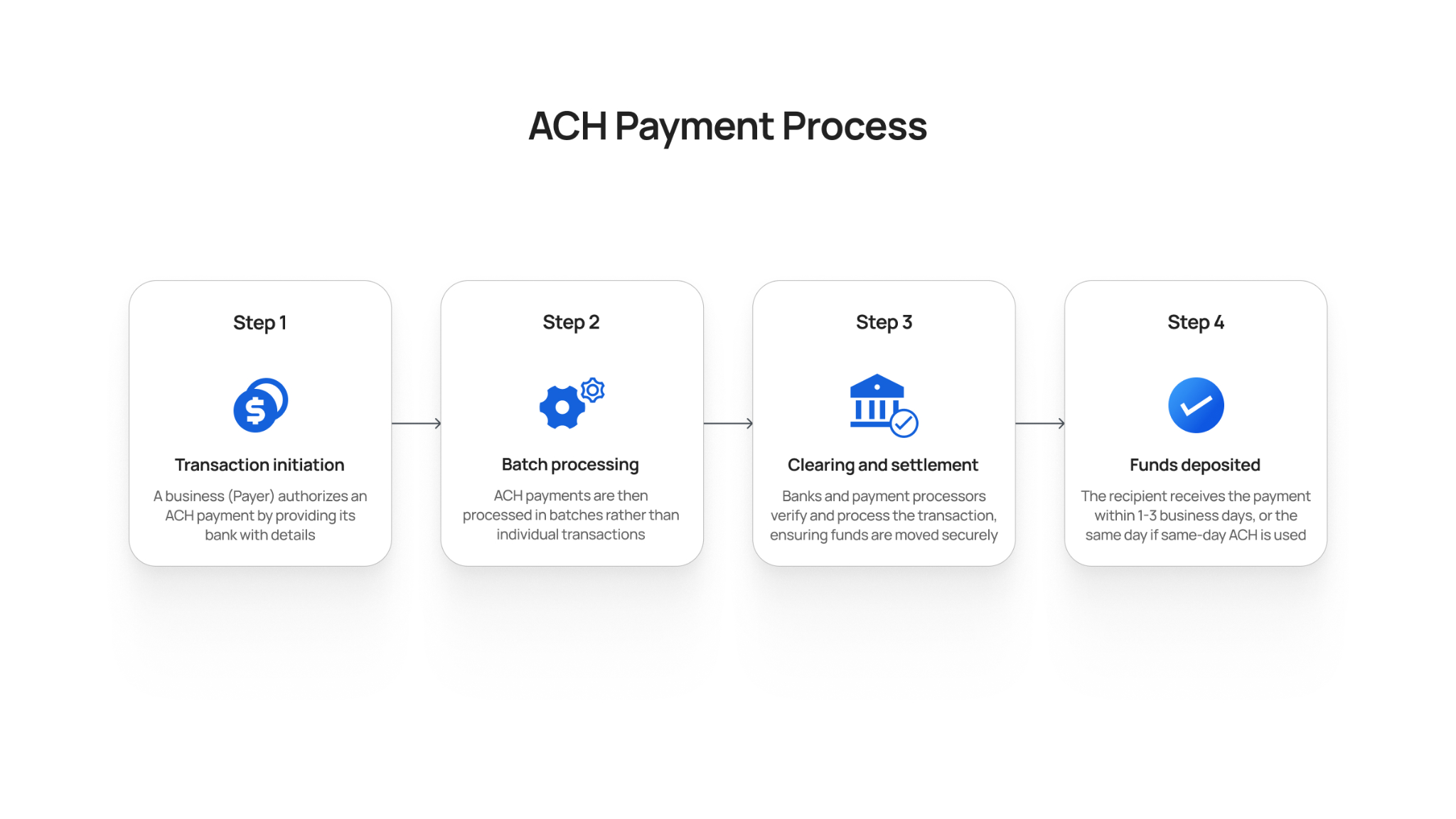

How do ACH payments work?

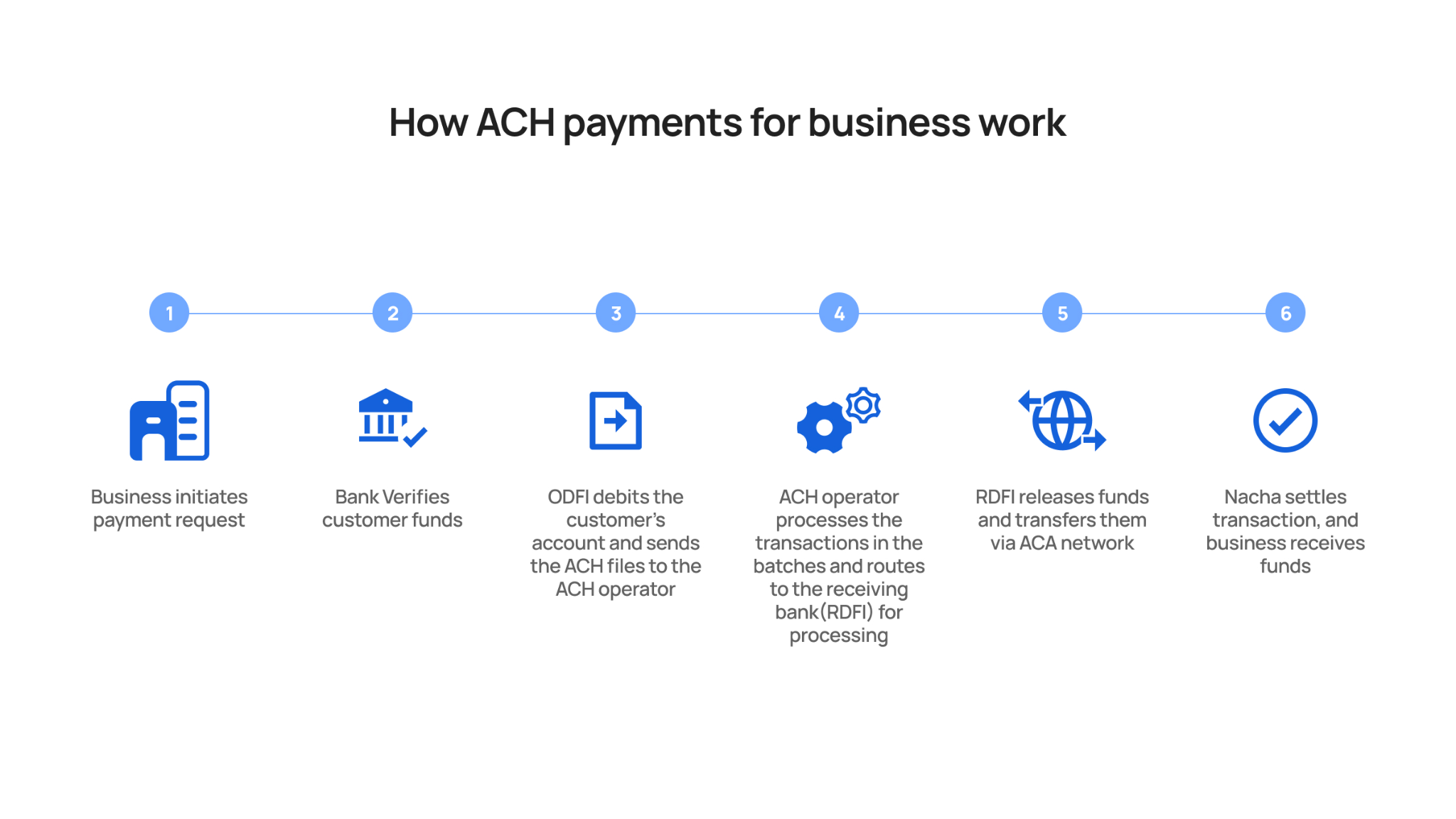

Every ACH transfer passes through five roles, two of which are financial institutions. Once you know them, the timing and the fees make sense.

- Originator: The person or business starting the payment

- ODFI (Originating Depository Financial Institution): The originator's bank, which submits the ACH request

- ACH Operator: The Federal Reserve or EPN, which routes the batched files

- RDFI (Receiving Depository Financial Institution): The bank on the other side

- Receiver: The account holder getting the credit or debit

Here's a familiar example. You set up autopay for your phone bill using your account and routing numbers.

At each billing cycle, your phone company's bank (the ODFI) sends an ACH transfer request to your bank (the RDFI). The two financial institutions confirm there are sufficient funds, and the money moves.

One quirk trips people up. "Originating" and "receiving" describe the request, not the cash. With an ACH debit, the originator sends the request but ends up receiving the funds.

The ACH operator settles batches several times throughout the business day. That batching is exactly what keeps transaction costs so low.

Because the work happens between financial institutions in bulk, ACH payments stay cheap even at enormous volume.

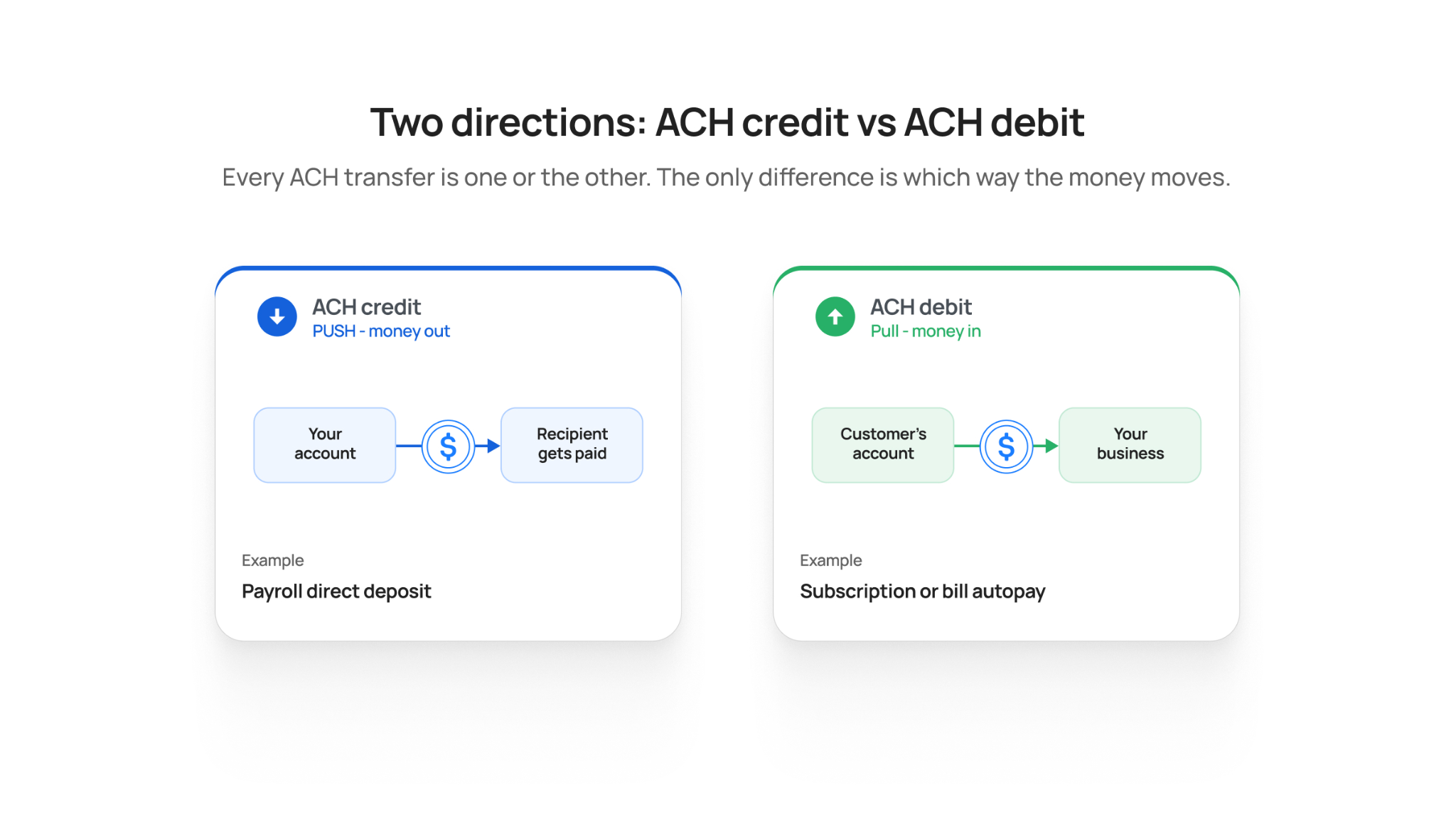

Types of ACH payments

Within the ACH system, every transfer is either a credit or a debit. The only difference is direction.

Together, these two ACH transfers cover every payment the network handles.

ACH credit (push)

An ACH credit pushes money out of one bank account into another. Payroll direct deposits are the classic example.

ACH debit (pull)

An ACH debit pulls money from an account, with the account holder's authorization. Your gym charging a monthly fee is an ACH debit.

Direct Deposits vs Direct Payments in ACH

NACHA sorts real-world uses into two categories.

- Direct deposits: Money paid from a business or government agency to a consumer, such as payroll, tax refunds, and Social Security

- Direct payments: Money individuals or organizations send out, such as bill payments, recurring payments, and P2P transfers

Direct deposits alone made up 8.74 billion ACH transactions in 2025, which is why "direct deposit" is almost a synonym for getting paid.

Examples of ACH payments

ACH payments show up all over everyday life. Common examples include:

- Payroll direct deposits from an employer

- Tax refunds from the IRS or a state government agency

- Automatic bill payments for utilities, insurance, or a mortgage

- Recurring payments for subscriptions and memberships

- Person-to-person transfers between friends or family

- B2B vendor and supplier payments between businesses

- Buying digital assets from an on-ramp like Transak

All these examples operate on the ACH network as either a credit or a debit. Direct deposits flow in, while direct payments like bills and subscriptions flow out. Although they can all ACH transfers, other payment methods may be available for some or most of these transactions.

Why are ACH payments highly preferable for American businesses

American businesses prefer ACH payments because they are the cheapest, most reliable way to move domestic money at scale. ACH costs a fraction of cards and wires, rarely declines, and automates the payments a company makes most often, such as payroll, vendor bills, and recurring invoices.

The shift is visible in the numbers. Businesses sent 8.1 billion B2B ACH payments in 2025, up 9.9% from the year before. Here is why US businesses keep choosing the ACH network:

- Cost-Effective at Volume: ACH transfers are cheap (often under $1) compared to card payments (1.3%–3.5%) or wires (up to $60)

- Replacing Paper Checks: It is electronic, traceable, and cheaper to process than paper checks, which are rapidly being abandoned for B2B payments

- Payroll Standard: It is the backbone for American payroll (direct deposits), allowing employers to automate scheduled payments

- Reliability and Automation: Bank accounts don't expire, leading to fewer recurring payment failures and allowing for automated billing, payroll, and reconciliation

- Universal US Reach: Connects to almost every US bank and credit union, allowing businesses to pay or collect from nearly any domestic account through a single processor

Where ACH leaves a gap for business use case

ACH is not the whole answer. It stops at the US border and runs on banking days, so a business with overseas suppliers or weekend payouts still needs another rail alongside it.

That is the one place ACH consistently falls short for US companies, and it is exactly where faster and cross-border options pick up.

How long do ACH transfers take?

Standard ACH transfers take 1–3 business days to settle. They don't run on weekends or federal holidays, because the network follows banking days. Most ACH payments you send or receive fall into this standard window.

ACH credits often clear in one business day. ACH debits usually settle within one to three. A receiving bank may also place a short hold on incoming funds.

Same Day ACH

Same Day ACH settles within hours, on the same business day, as long as you submit before one of three daily cutoff windows.

It carries a per-transaction cap of $1 million, in place from 2022. NACHA has approved raising that limit to $10 million on September 17, 2027.

Same Day ACH handled 1.4 billion payments worth $3.9 trillion in 2025, up 16.7% year over year. These faster ACH transfers usually cost a small premium per transfer.

Coming Soon: Instant ACH Bank Transfer by Transak

Pay from your bank account and get crypto in your wallet within seconds. Card speed, bank cost, same checkout.

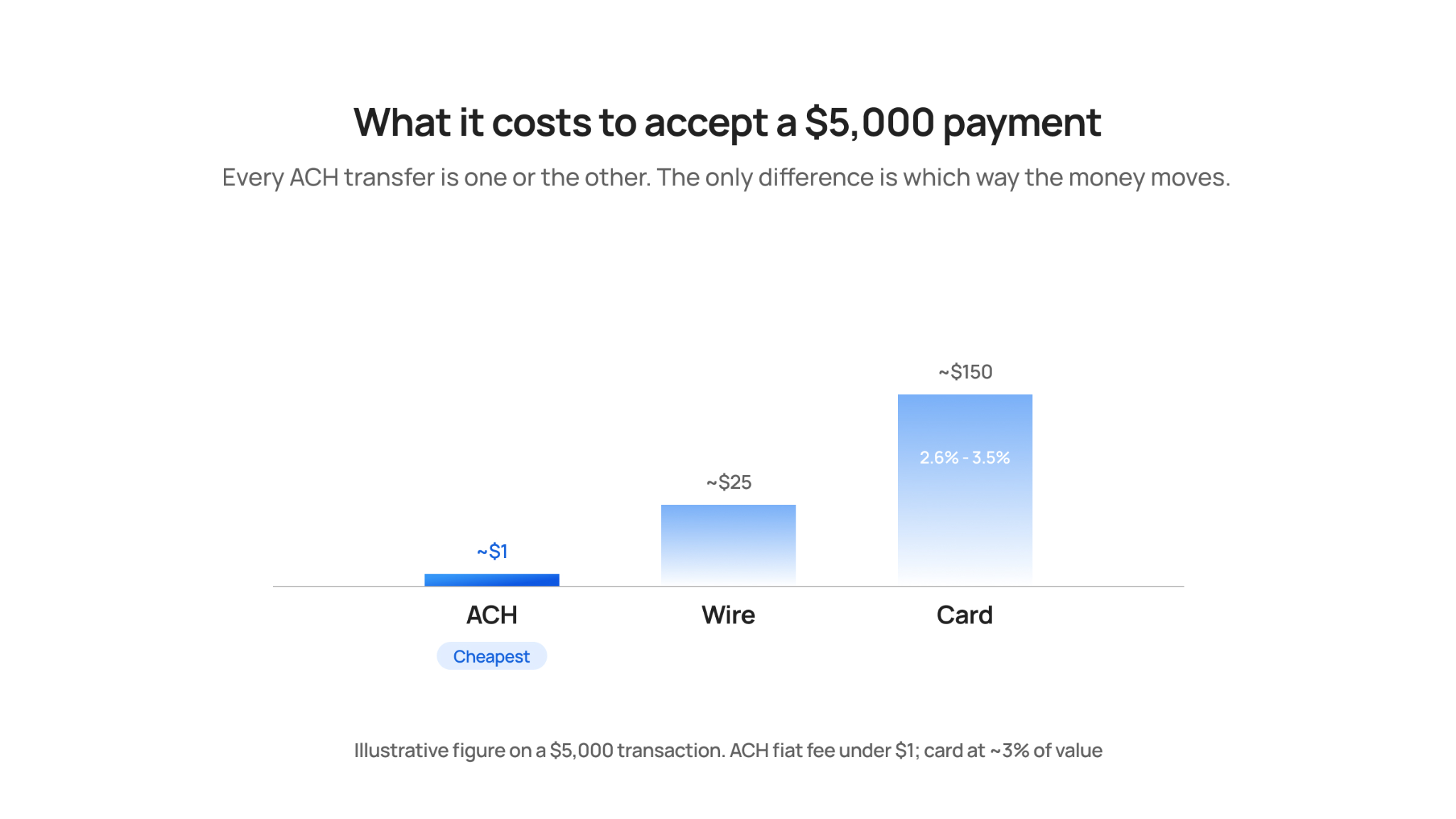

How much do ACH payments cost?

ACH is one of the cheapest ways to move money. The median internal cost to process ACH payments is $0.29 per transaction.

For a business using a payment processor, flat fees typically run $0.25 to $1.50 per ACH transfer. Some providers charge a small percentage instead, and a few add a monthly fee. Consumers usually pay nothing to receive funds.

Even with the odd return fee, ACH payments cost a fraction of card payments or wire transfers.

The savings show up most against other methods:

- Card payments charge roughly 1.3%–3.5% per transaction.

- Wire transfers can cost up to $60, often charged to both parties.

On a $5,000 invoice, a card might cost $100 or more, while ACH stays under a dollar. For any business taking recurring payments, that gap adds up fast.

Why ACH payments get rejected

When an ACH transfer fails, the bank returns a reject code that explains why.

|

Code |

Reason |

What to do |

|

R01 |

Insufficient funds |

Retry later or ask for another payment method |

|

R02 |

Account closed |

Request updated account details |

|

R03 |

No account / unable to locate |

Re-check the account and routing numbers |

|

R29 |

Corporate customer not authorized |

Get proper authorization first |

A rejected ACH payment can trigger a return fee, usually $2–$5 for both parties. Fix the cause quickly to avoid repeat fees on each billing cycle.

How to send and accept ACH payments

For a business, ACH runs in both directions. Here's each one.

How do I pay someone via ACH?

- Enable ACH through your bank, payroll provider, or a payment processor.

- Get the recipient's authorization to pay them.

- Submit the payment using their bank routing number and account number.

- Wait one to three business days for the transfer to clear.

How to accept ACH payments

Small businesses can't act as the ODFI or RDFI themselves. You work through a bank or another financial institution, or a third party payment processor.

- Set up an ACH collection with a processor or your bank.

- Collect a signed or online authorization (a mandate) from the customer.

- Verify the customer's bank account, often using microdeposits.

- Initiate the ACH debit and receive the funds once the batch clears.

The authorization step is not optional paperwork. An unauthorized ACH debit can be returned, and the business may face a penalty.

Advantages and disadvantages of ACH payments

ACH payments are the right tool for many jobs and the wrong one for others. The trade-offs are easy to lay out.

Advantages of ACH payments

- Low cost: Far cheaper than credit card payments or wire transfers

- Fewer declines: ACH payments link direction to bank accounts and the accounts don't expire like cards, so recurring payments fail less often

- Built for automation: Ideal for payroll, recurring bills, and B2B transfers

- Safer than checks: Nothing physical to lose, steal, or forge

- Reversible: Unlike a wire transfer, an ACH transfer can be returned within set windows

Disadvantages of ACH payments

- Speed: Standard ACH transfers can take several business days, too slow for urgent transfers.

- Privacy: setting one up means sharing your bank account and routing numbers, which some payers dislike.

- Limits: ACH transactions can carry daily and monthly caps on how much you move.

- US-only: ACH payments are domestic, so international payments need wire transfers or other rails.

For very large or international transfers, businesses fall back on wire transfers or stablecoin-based cross-border rails, since ACH payments can't reach overseas accounts.

Are ACH payments safe?

Yes. ACH payments run on one of the most regulated payment systems in the US, and NACHA requires banks, credit unions, and processors to encrypt sensitive bank data. Consumer ACH debits are also protected under the Electronic Fund Transfer Act.

The rules just got stricter. In 2026, Nacha replaced its old "commercially reasonable" fraud standard with risk-based fraud monitoring, phased in across the network in March and June 2026.

The target is credit-push fraud, where a payer is tricked into authorizing a real payment. Vendor-impersonation and payroll-redirection scams are common examples.

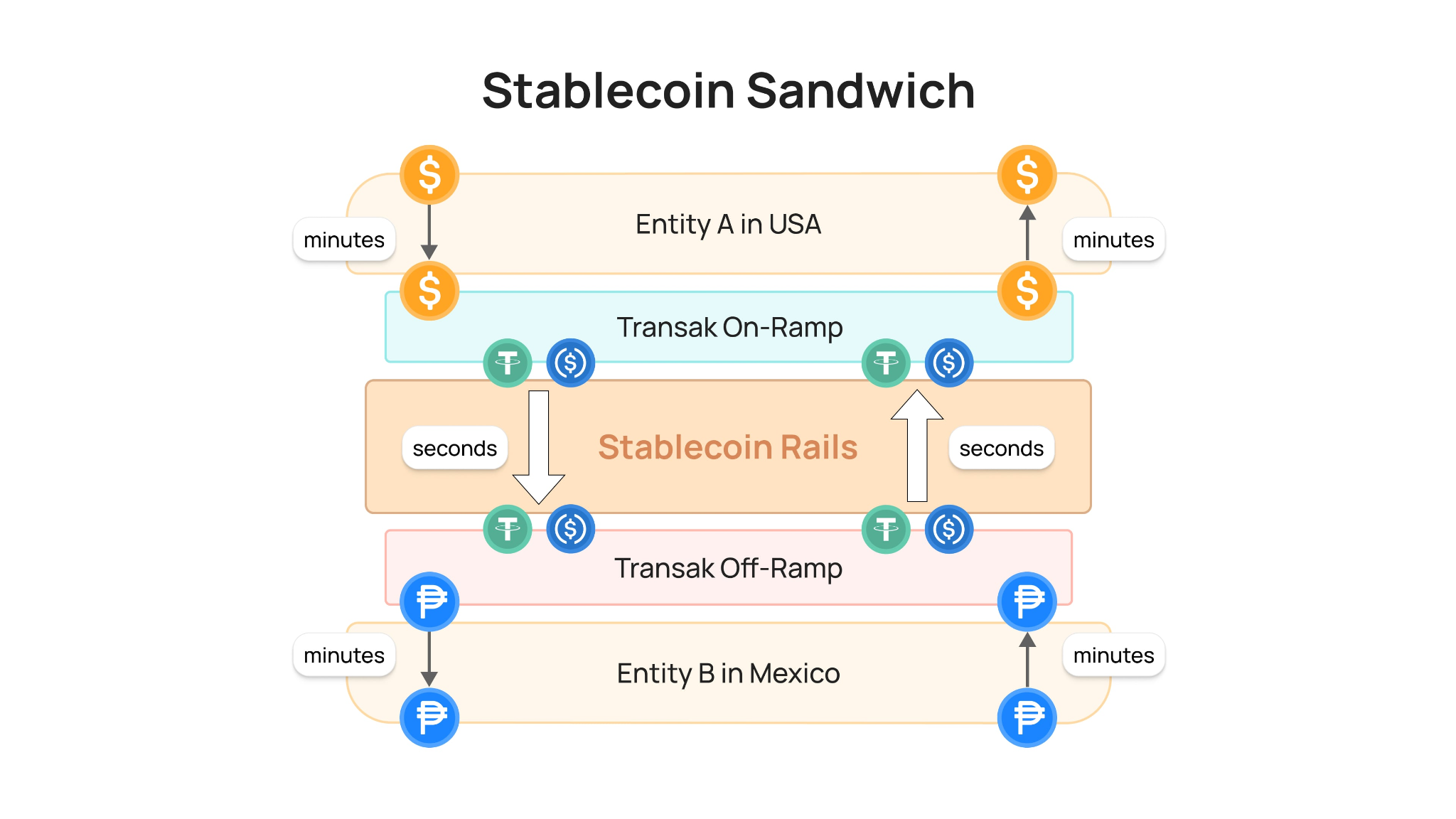

Where ACH stops and stablecoins begin

ACH payments are excellent for domestic, scheduled payments. They do nothing the moment money has to cross a border or move on a weekend.

That's the gap fintechs increasingly close with stablecoins. When a user funds their wallet with digital assets, an ACH bank transfer via an on-ramp is a common way to move on-chain dollars in.

For cross-border flows, dollars collected by ACH convert to a stablecoin, move on-chain in minutes, then convert back to local currency. This stablecoin sandwich is how cross-border payments now settle in minutes instead of days.

Frequently asked questions

What is an example of an ACH payment?

A paycheck deposited by your employer is an ACH payment that pushes money to you. An automatic monthly utility charge pulled from your checking account is an ACH debit. Both move through the ACH network.

Are ACH and Zelle the same?

No. Zelle moves money between enrolled bank accounts in minutes over its own network. ACH transfers are processed in batches and usually take one to three business days, though Same Day ACH is faster. They are separate payment systems.

How do I pay someone via ACH?

Through your bank or a payment processor. You need the recipient's bank routing number and account number, plus their authorization. The ACH transfer then clears in one to three business days.

Is an ACH payment the same as a direct deposit?

Not quite. A direct deposit is one type of ACH payment, a push of funds into your account. All direct deposits are ACH payments, but not all ACH payments are direct deposits.

Is an ACH transfer the same as an EFT?

No. ACH is one kind of electronic funds transfer (EFT), but EFT is a broad term that also covers wire transfers, card payments, and P2P apps. Every ACH payment is an EFT; not every EFT uses the ACH network.

Where to go from here

Sort your payments into two buckets. Domestic and scheduled? ACH wins on cost. Cross-border or urgent? You'll need another rail.

Map your main payment flows against that split, and you'll know exactly where ACH payments fit and where to route to a faster rail instead.