For financial apps, wallets, payout platforms, and fintechs, stablecoins offer a practical way to move money faster, reduce settlement friction, and make payment flows easier to predict.

Legacy settlement is slow and unpredictable. Cross-border wires take days, remittance targets are frequently missed, and treasury teams struggle with manual reconciliation across time zones.

Stablecoins solve this by finalizing payments in seconds at a fraction of the cost. These rails run 24/7, eliminating banking hour delays and Sunday cutoffs.

This piece breaks down why stablecoin settlement is genuinely faster and more reliable than legacy infrastructure, what the production data from Visa, Western Union, and MetaMask shows, and what fintechs need to consider when wiring stablecoin rails into their products.

Why Settlement Speed Matters So Much

Settlement is where a payment actually becomes final. Until then, money may be “in motion,” but it is not fully usable. For fintechs, that gap means delayed user balances, fragile treasury planning, manual reconciliation, and support tickets from customers who think something has gone wrong.

Traditional rails often introduce delays because they depend on banking hours, regional cutoffs, intermediaries, and batch processing. That is manageable for some business models, but it becomes painful when your product’s business model primarily revolves around transaction speed and/or uninterrupted cash flow.

Stablecoins help because they settle on-chain. Once a transfer is confirmed, the receiving side can treat the value as available much faster than with many legacy rails. For apps that need to credit user accounts, fund wallets, or route payouts quickly, that difference is huge.

Why Does Traditional Settlement Infrastructure Slow Fintechs Down?

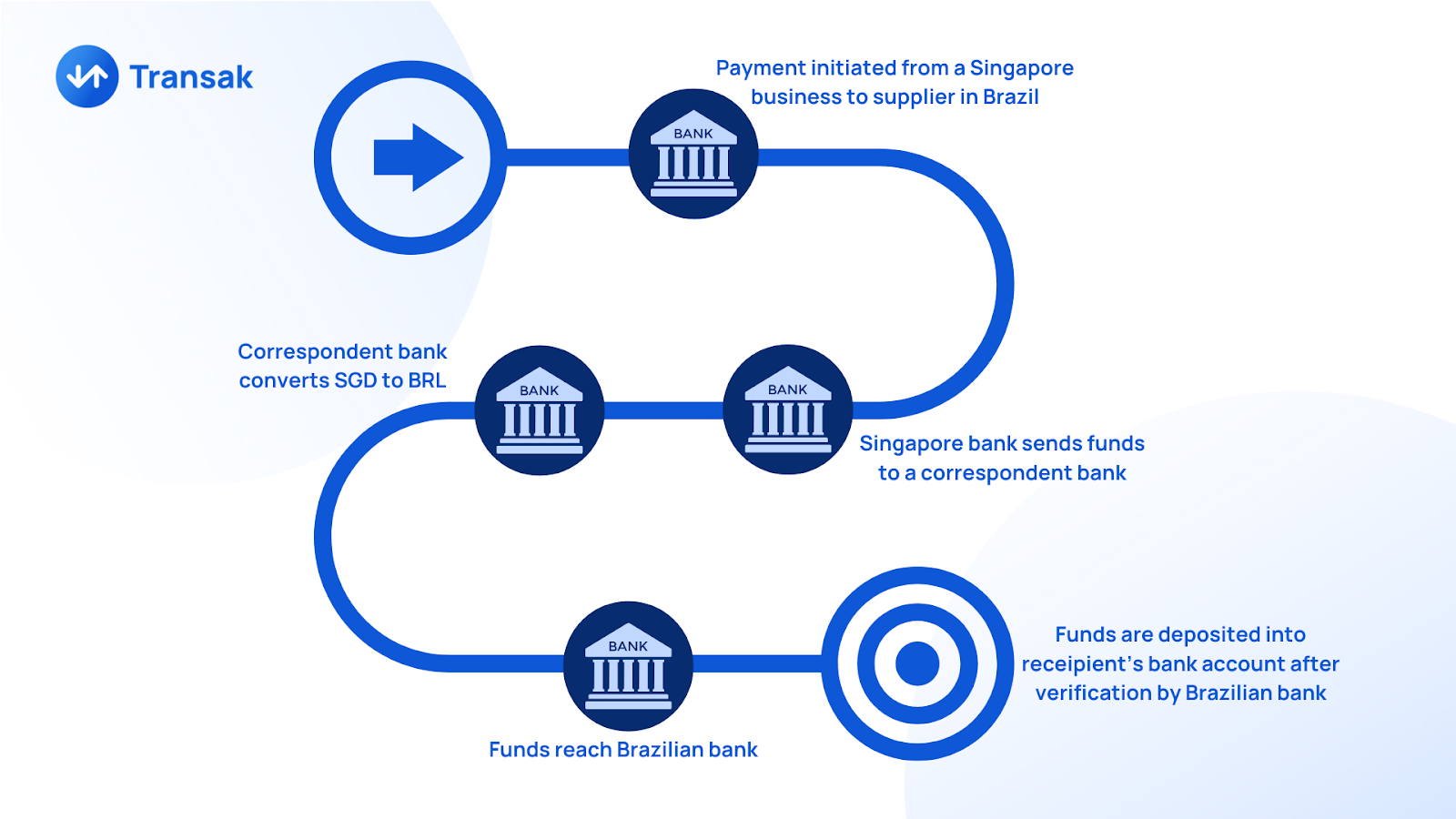

Traditional cross-border settlement is slow because it depends on a chain of correspondent banks holding pre-funded accounts in each currency, all reconciling during local banking hours. SWIFT itself only sends the messages. The actual money moves through nostro/vostro ledgers that batch-process during business windows, which is why even routine wires often take 24 to 72 hours.

The Financial Stability Board's most recent annual review found that only 60% of wholesale payments on SWIFT settle within an hour. For retail remittances, just 35% reach beneficiaries within an hour, against the G20's target of 75%. The World Bank's 2026 remittance cost survey put average global transfer fees at 6.49%, which is well above the 1% benchmark regulators set in 2020.

For a fintech, every layer of that chain is a place something can break.

- A correspondent bank closes its books at 4pm local time.

- A compliance check flags a false positive that takes a human two hours to clear.

- A currency conversion happens at a rate that wasn't quoted to the end user.

The longer the chain, the more reconciliation, more capital tied up in pre-funded accounts, and more reasons a payment lands late or doesn't land at all.

Stablecoins remove the chain entirely.

How Fast Do Stablecoin Payments Actually Settle?

Stablecoin payments settle in seconds. There is no correspondent bank, no nostro reconciliation, and no banking-hours dependency. Once the block confirms, the payment is final and irreversible.

That speed gap has become the single biggest reason institutional players are migrating to stablecoin rails. Visa's stablecoin settlement program exceeded a $7 billion annualized run rate by May 2026. Western Union announced in April 2026 that its USDPT stablecoin will replace SWIFT as the settlement layer between the company and its global agents, citing real-time, around-the-clock settlement as the primary motivation.

For a fintech, the practical impact shows up in three places:

- User experience: A remittance app that confirms delivery in seconds beats one that promises "1-3 business days" every time.

- Working capital: Funds aren't trapped in correspondent accounts waiting to settle. They're available the moment the block confirms.

- Operational predictability: A 24/7 rail means weekend payouts, holiday remittances, and end-of-quarter treasury moves all run on the same timeline as a Tuesday afternoon transaction.

What Makes Stablecoin Settlement More Reliable Than Legacy Rails?

Speed gets the attention, but reliability is what makes a payment system usable at scale.

A fast rail that fails often is not a solution. Fintechs need confidence that transfers will arrive, balances will update correctly, and exceptions can be handled cleanly. Stablecoins help here because the transfer layer is programmatic and transparent. Teams can see when value moved, when it was confirmed, and where a failure occurred.

This is why stablecoins are now described less as a crypto product and more as financial infrastructure. McKinsey reported that Asian-originated stablecoin payments alone accounted for $245 billion in 2025 (roughly 60% of global volume) with treasury teams at multinationals using USDC and USDT for intraday liquidity moves.

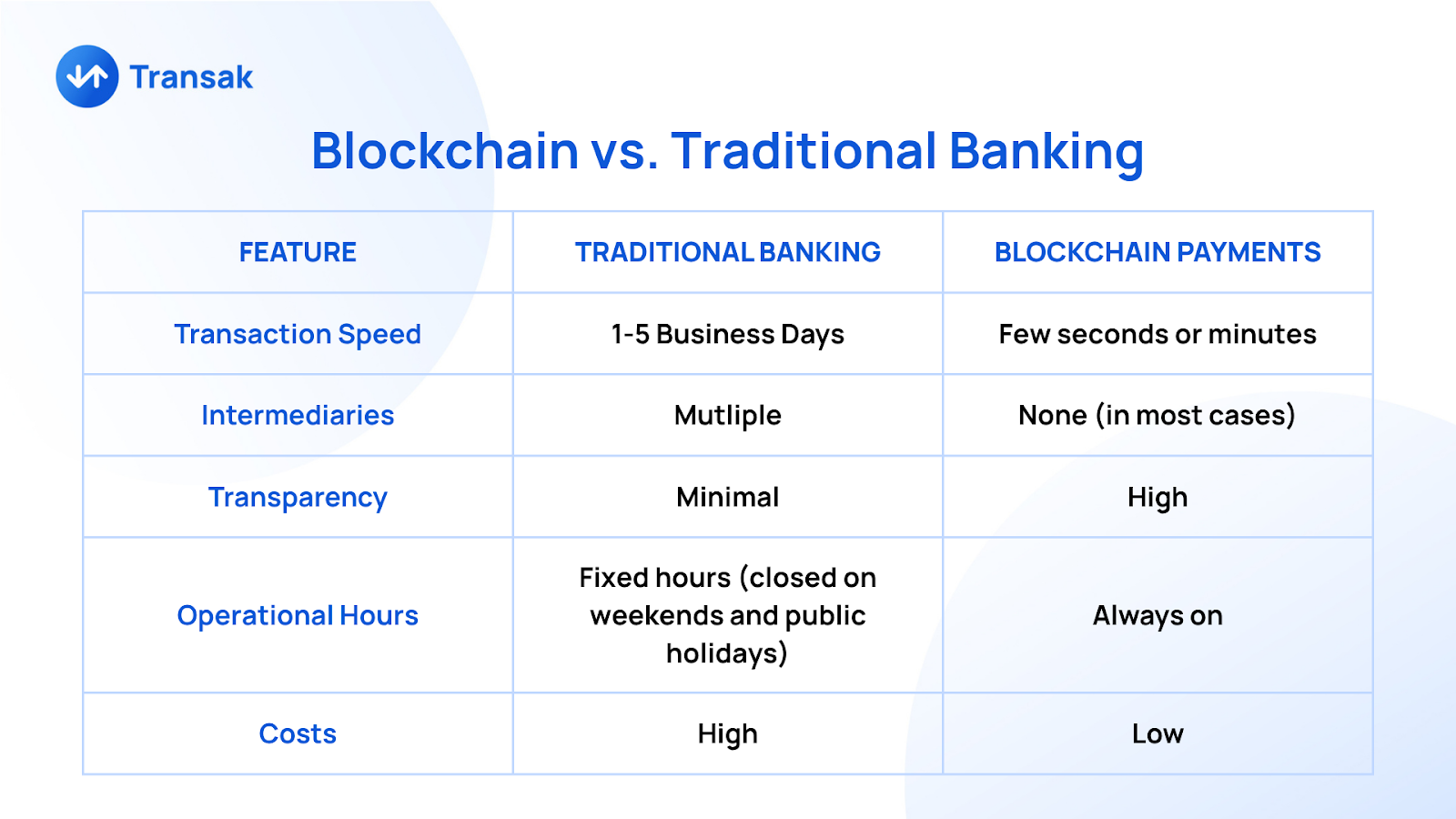

Stablecoin Settlement vs. Traditional Rails

|

SWIFT/Correspondent Banking |

Stablecoin Rails |

|

|

Settlement time |

1-5 business days; 60% of wholesale settles within 1 hour |

Seconds to minutes; finality in 0.4s (Solana) to 15s (Ethereum) |

|

Operating hours |

Banking hours, weekdays |

24/7/365 |

|

Cost (cross-border) |

2-7% of transfer value; 6.49% average for retail remittance |

0.1-0.5% of transfer value |

|

Reversibility |

Reversible during multi-day clearing window |

Irreversible once block confirms |

|

Reconciliation |

Manual, multi-party, often days |

Real-time, on-chain, hash-verified |

|

Pre-funding |

Required (nostro/vostro accounts) |

Not required |

|

Programmability |

None (messaging only) |

Native via smart contracts |

|

Geographic coverage |

~200 countries via correspondent chains |

Anywhere with internet access |

How Fintech Teams Should Think About Stablecoin Implementation

If you are evaluating stablecoins for settlement, do not start with the coin. Start with the workflow.

Ask:

- Where do our current settlement delays happen?

- Which flows need 24/7 availability?

- What level of finality do we need before crediting a user or partner?

- Where does manual reconciliation create cost or risk?

- Which markets suffer most from banking-hour dependencies?

That framing helps you focus on business outcomes rather than asset speculation.

Conclusion

A common mistake is to treat stablecoins as a niche crypto tool. That misses the point.

Stablecoins are increasingly useful as a payment primitive. For many financial apps, they sit underneath the product, powering faster settlement without forcing the company to become a crypto-native brand.

Transak allows fintechs and financial apps to use regulated on- and off-ramp rails with global payment coverage so that stablecoin flows are easier to launch and operate. The user sees a smoother experience. The business keeps its own product identity.

FAQs

How fast do stablecoin payments settle compared to SWIFT?

Stablecoin payments settle in seconds to minutes while SWIFT cross-border payments take 1-5 business days, with only 60% of wholesale payments settling within an hour according to the FSB.

Are stablecoin payments cheaper than wire transfers?

Yes. Stablecoin cross-border payments typically cost 0.1-0.5% of transfer value, compared to 2-7% for traditional wire transfers and a 6.49% global average for retail remittances per the World Bank's 2026 data.

Are stablecoins regulated for fintech use?

Yes, in major markets. The EU's MiCA framework went into force in 2024, the US passed the GENIUS Act in 2025 providing a federal stablecoin framework, Singapore's MAS finalized stablecoin rules in 2023, and the UK's FCA is finalizing rules in 2026. Fintechs operating with regulated issuers (USDC, USDT, EURC, PYUSD) and licensed infrastructure providers can run stablecoin settlement compliantly across most major jurisdictions.

Which stablecoins are best for fintech settlement?

USDC and USDT account for roughly 85% of stablecoin liquidity and are the default choice for most fintech settlement use cases. EURC is the leading euro-denominated option for European corridors. PYUSD and RLUSD offer additional issuer diversity for institutions wanting to spread reserve risk.

Do I need to build stablecoin settlement infrastructure in-house?

Most fintechs don't. Building in-house requires money transmitter licenses in each target market, KYC/AML infrastructure, fraud monitoring, and ongoing compliance taking typically 12-18 months of regulatory work before first settlement. Transak offers that stack as a single API integration that can go live in a few weeks.

Looking to add stablecoin settlement to your fintech product? Explore how Transak powers fiat-to-stablecoin and stablecoin-to-fiat infrastructure for 600+ apps across 64+ countries through a single API.