Takeaways

The ACH network was built in the 1970s to replace paper checks between American banks. The wire predates the telephone. Both still move trillions of dollars a year, and for most of what you'll ever pay for, one of them is the right call.

Here's how to tell which.

An ACH payment is cheap, runs in batches, and can be reversed if something goes wrong, so it carries the routine work like payroll, rent, the subscriptions you forgot you have. A wire moves on its own, lands the same day, and stays put once it clears, which is why it handles the payments that have to be fast and certain, like the deposit on a house.

The key differences between ACH and wire transfers come down to cost, speed, safety, limits, and reach, and this guide walks through each. It also answers the questions people ask most, including whether Zelle counts as either one, and where both rails quietly fail.

ACH vs Wire Transfer: A quick comparison

ACH transfers move money between US bank accounts in batches through the ACH network for a few cents, settling in one to three business days, and they can be reversed. Wire transfers send money individually and in real time for $25 to $50, settle the same business day, and are final.

ACH suits routine domestic payments while wire transfers suit large, urgent, or international ones.

|

ACH transfer |

Wire transfer |

|

|

Typical cost |

Free–$3 (often free) |

$25–$50 |

|

Speed |

Hours to 1–3 business days |

Minutes to same business day |

|

Processing |

Batched, several times daily |

Individual, real time |

|

Reversibility |

Yes, via returns/disputes |

No, final once cleared |

|

Direction |

Sender or receiver can initiate |

Only the sender initiates |

|

Reach |

US domestic (mostly) |

Domestic and international |

|

Limits |

$1M (same-day cap) |

Very high or unlimited |

|

Best for |

Payroll, recurring bills, direct deposit |

Real estate, urgent or international payments |

ACH transfers bundle many payments into batches and a wire transfer moves one payment on its own, instantly and irreversibly.

What is an ACH transfer?

An ACH transfer is an electronic payment that moves money between bank accounts through the Automated Clearing House network, governed by NACHA. Banks and credit unions batch these electronic payments and process them several times a day.

In 2025 the ACH network handled 35.2 billion payments worth $93 trillion, making it the backbone of US payroll and bill payments.

ACH stands for Automated Clearing House, the network that connects nearly every bank or credit union account in the United States. Most banks and credit unions in the country support ACH transfers, so reach is rarely an issue domestically. Almost any routine domestic payment you make without cash or a card runs across these ACH rails, from your salary to your utility bill.

How do ACH transfers work?

Because ACH transfers are typically processed in batches rather than one at a time, financial institutions clear them in set windows during the day. That batch model keeps the cost near zero and leaves a clear digital paper trail, which strengthens fraud protection.

What is ACH used for?

ACH transfers are best for low-cost, routine domestic payments. Routine or recurring bills/payments like payroll, subscriptions, and direct deposit all sit squarely in ACH territory.

What is a wire transfer?

A wire transfer moves money directly between two financial institutions, settled individually and in real time rather than in a batch. Domestic wire transfers run over the Federal Reserve's Fedwire network, while international wires use SWIFT.

Funds sent/received via wire transfers are usually available within minutes to hours and are final once the receiving bank credits them. Wire transfers are built for large, urgent, or international payments.

Because each wire transfer is processed on its own, there is no waiting for a batch window. Send a domestic wire before your bank's cutoff, usually between 3 and 6pm ET, and it often settles within hours. That immediacy is the whole point of paying for a wire.

How do wire transfers work?

Only the sender can start a wire, which makes wire transfers unidirectional. You cannot pull money toward yourself by wire the way an ACH debit can. The sender's financial institution sends a secure payment instruction to the recipient's bank, the funds move, and the receiving bank credits the recipient's account.

Domestic vs international wire transfers

Domestic wire transfers stay inside the US banking system and settle fastest. International wire transfers operate on SWIFT and can move money between countries and convert currencies across a large international banking network. That global reach is why wire transfers remain the default for international payments.

International wires typically take one to five business days, route through correspondent banks that may each deduct $15 to $50, and hide a currency-conversion markup of 3 to 5 percent over the mid-market rate. When you send money abroad through a traditional bank, the headline wire fees are rarely the full story.

ACH vs wire transfer cost comparison

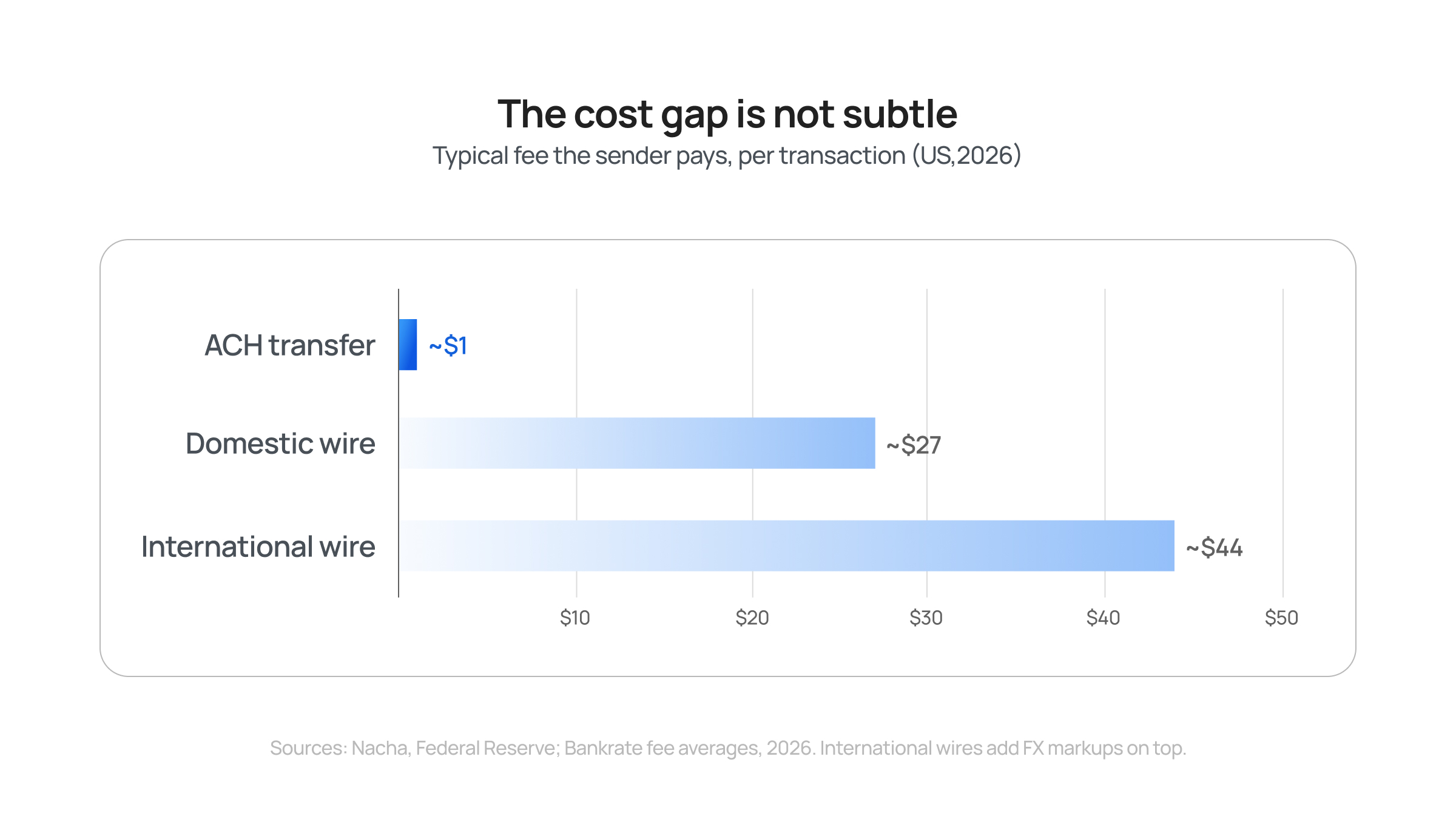

ACH transfers are far cheaper than wire transfers.

An ACH payment is usually free for consumers and roughly $0.25 to $3 for businesses, while wire transfers typically cost $25 to $50. A domestic wire transfer runs up to $35 for the sender and up to $20 for the receiver..

|

Transfer type |

Sender pays |

Receiver pays |

|

ACH transfer |

Free–$3 |

Usually free |

|

Domestic wire |

$15–$35 |

~$13–$20 |

|

International wire |

$35–$50+ |

~$14–$25 |

Financial institutions charge high premiums for wire transfers because each one settles individually instead of riding in a batch. ACH transfer fees stay low for the opposite reason. On international wires the gap widens further. A 3% currency markup on a $100,000 payment adds $3,000, far more than any visible wire fee.

The caveat is that low cost assumes you can wait. If a payment has to clear today to release a shipment or close a deal, the higher fees on a wire buy a certainty that ACH cannot.

ACH vs wire transfer speed: Which is faster?

An ACH transfer usually takes longer than a wire. Domestic wire transfers clear within minutes and settle the same business day, while ACH transfers take from a few hours to one to three business days.

Same Day ACH narrows the gap by clearing and settling on the same day, but standard ACH is slower than a wire by design.

Speed and finality are linked. A wire feels fast partly because it cannot be reversed once it clears. ACH feels slower partly because the network builds in time to catch errors and process returns. The delay is a feature, not a flaw, for routine transactions.

If the sender pays for same day processing, ACH transfers can clear, settle, and disburse on the same business day. Same-day settlement moved 1.4 billion payments worth $3.9 trillion in 2025. For an urgent domestic payment under the cap, the same-day option often beats reaching for a wire.

Is an ACH transfer safer than a wire?

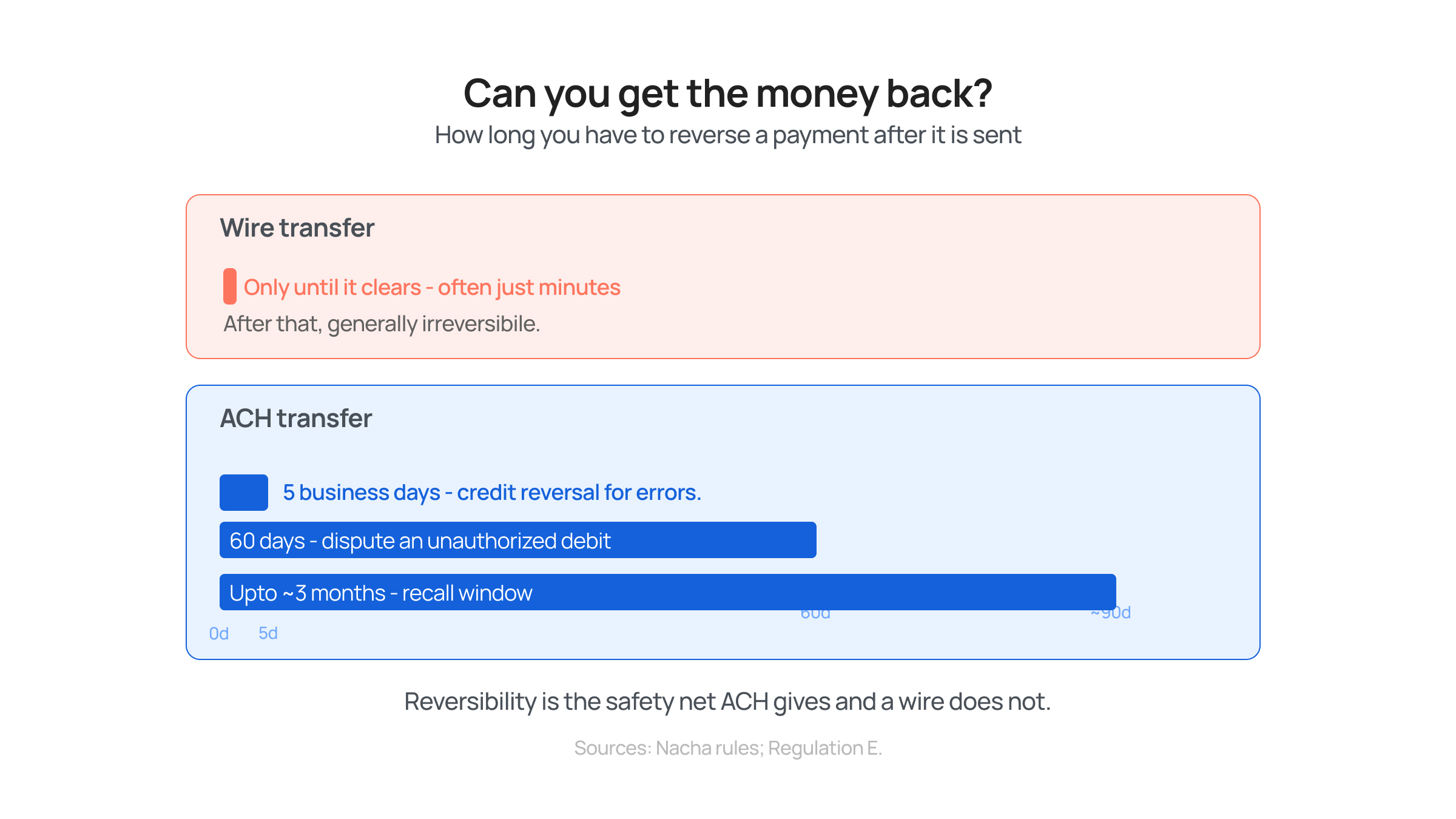

For everyday payments, yes. ACH transfers are reversible and carry strong consumer protections, so an unauthorized or mistaken payment can be disputed. Wire transfers are immediate, final, and generally impossible to reverse once funds leave, which makes them a favorite target for fraud. For routine transactions, ACH is the safer transfer method.

Importantly. ACH transfers can be recalled for up to three months, and credit reversals can be requested within five business days for errors such as a wrong account number or amount. Banks and credit unions follow NACHA rules for these returns. A consumer can dispute an unauthorized ACH debit for up to 60 days after the statement date under federal rules.

Importantly. ACH transfers can be recalled for up to three months, and credit reversals can be requested within five business days for errors such as a wrong account number or amount. Banks and credit unions follow NACHA rules for these returns. A consumer can dispute an unauthorized ACH debit for up to 60 days after the statement date under federal rules.

Wire transfers offer almost none of that. A wire can be canceled only up until it clears, which can happen within minutes, and after that it is generally irrevocable. The FBI's Internet Crime Complaint Center reported that business email compromise scams cost US businesses more than $2.7 billion in 2024, and most of those schemes end in a fraudulent wire that cannot be clawed back.

The practical rule is to use ACH when you want a safety net. Only send a wire to a recipient you trust, and confirm the bank account information through a second channel first.

Transaction limits and international reach

Wire transfers carry far higher limits, often exceptionally high or effectively unlimited, while ACH transfers face per-payment caps.

Same Day ACH currently tops out at $1 million per payment, rising to $10 million in September 2027. ACH is also largely US-only, whereas wire transfers move money across the globe through SWIFT, the standard rail for international money transfers.

ACH transfers are primarily used within the United States and a few countries with bilateral agreements. International ACH transfers exist, but they are not as widely accepted, so finance teams sending money abroad still reach for international wires. Wire transfers can reliably move money between countries and convert currencies, which is why they remain necessary for high-value and international transactions.

This is the clearest line between the two.

For domestic transfers, the choice is about cost and speed. The moment a payment crosses a border, only one of these rails can even reach the recipient.

Is it better to use ACH or wire?

It depends on the payment.

Use ACH transfers for recurring, domestic, lower-urgency payments such as payroll, rent, and bill payments, where low cost and reversibility matter most.

Use a wire transfer for large, urgent, or international one-off payments where same-day finality is required and the recipient is verified, such as a real estate down payment.

|

Scenario |

Better rail |

Why |

|

Monthly payroll |

ACH |

Recurring, predictable, low cost adds up |

|

Real estate down payment |

Wire |

Large, same-day, recipient requires it |

|

Subscription billing |

ACH |

High volume, reversibility helps |

|

Urgent vendor payout (US) |

Same Day ACH |

Same business day without the wire fee |

|

Sending money overseas |

Stablecoins |

Faster, lower fees, supports any volume, compliant with Transak as infrastructure |

Is Zelle a wire transfer or ACH?

Zelle is not a wire transfer. It is a real-time, peer-to-peer service that moves money between US bank accounts almost instantly, and it traditionally settles between financial institutions over the ACH network. So, Zelle behaves like a faster ACH transfer rather than a wire, though like a wire it is hard to reverse once sent.

Zelle links a bank account to an email address or a US mobile number, and funds usually arrive within minutes when the recipient is enrolled. Behind that instant experience, settlement between banks has historically run on ACH rails, with some banks now using newer real-time networks. The front end feels instant while the back-end clearing often still rides ACH rails.

Because a Zelle transfer feels final, treat it with the same caution as a wire. Only send money to people you know, since there is little recourse if you pay the wrong person. Zelle also works only with US bank accounts, so it is no help for international payments.

Where ACH and wire transfers both fall short

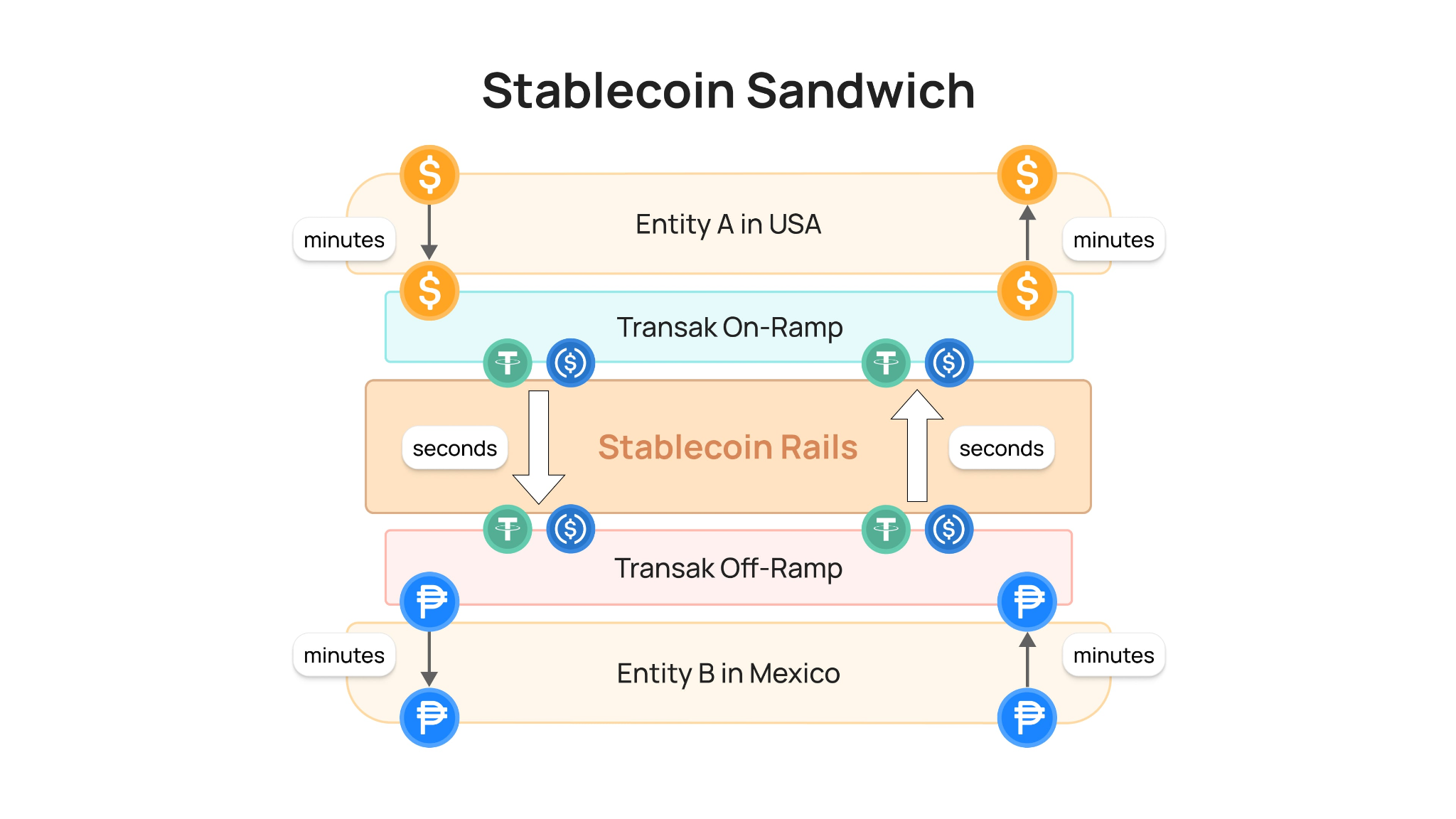

Neither ACH nor wire transfers handle cross-border payments well. ACH is US-focused, and international wire transfers are slow and costly, taking one to five business days at 2% to 7% of value once SWIFT, correspondent banks, and currency markups are counted. This gap is what pushed payment teams toward the stablecoin sandwich model, where value moves abroad on blockchain rails in minutes.

The moment money crosses a border, the two legacy rails both struggle. ACH simply cannot reach the recipient. A wire can, but slowly and expensively, and only about 55-60% of wholesale cross-border payments settle within an hour, lower than the G20 75% target.

Stablecoins reroute that flow. Money starts as local fiat, converts to a stablecoin such as USDC or USDT, moves across a blockchain in seconds, and converts back to local currency at the other end. Both the sender and the receiver touch only their own currency.

Also Read: How Stablecoins Help Financial Apps and Fintechs Improve Settlement Speed and Reliability

This is already in production. Remittance companies use it to cut settlement from days to minutes, payroll platforms run global payouts on stablecoin payroll rails, and fintechs add the capability by embedding a regulated on-ramp instead of building money-transmission licensing from scratch. Routing across chains and partners is handled by a stablecoin orchestration layer, so the business issues one payment instruction and the complexity stays hidden.

FAQs

Is it better to use ACH or wire?

It depends on the payment. Use ACH transfers for recurring, domestic, lower-urgency payments such as payroll, rent, and paying bills, where low cost and reversibility matter most. Use a wire transfer for large, urgent, or international one-off payments where same-day finality is required and the recipient is verified.

Does an ACH take longer than a wire?

Yes. Domestic wire transfers clear within minutes and settle the same business day, while standard ACH transfers take from a few hours to one to three business days. A same-day ACH option narrows the gap, but a wire is still faster for genuinely same-day, large-value payments.

Is Zelle a wire transfer or ACH?

Zelle is not a wire transfer. It is a real-time, peer-to-peer service that moves money between US bank accounts almost instantly and traditionally settles between financial institutions over the ACH network. Zelle behaves like a faster ACH transfer, but like a wire it is hard to reverse once sent.

Is an ACH transfer safer than a wire?

For everyday payments, yes. ACH transfers are reversible and carry consumer protections, so an unauthorized or mistaken payment can be disputed. Wire transfers are final and generally impossible to reverse once funds leave, which makes them a more common target for fraud.

Can ACH transfers be used for international payments?

Mostly no. ACH transfers are used within the United States and a handful of countries with bilateral agreements. International ACH transfers exist but are not widely accepted, so wire transfers over SWIFT remain the standard rail for international money transfers, and stablecoin rails are a faster modern alternative.

What is the difference between ACH and EFT?

EFT, or electronic funds transfer, is the umbrella term for any movement of money between bank accounts over a computer network. ACH transfers and wire transfers are both types of EFT. ACH is one specific system that runs on the ACH network and is governed by Nacha.

Move money across borders without the wire

If your next payment is headed to another country, we provide compliance-ready on- and off-ramp rails so apps can settle cross-border value on stablecoins in minutes, in users' own currencies. See how Transak's regulated rails work.