Takeaways

A fintech app integrates stablecoin payments by embedding a regulated on-ramp provider that handles fiat-to-stablecoin conversion, KYC, and compliance. The fintech app is a software product while the provider carries the licenses, the banking partnerships, and the money transmission risk.

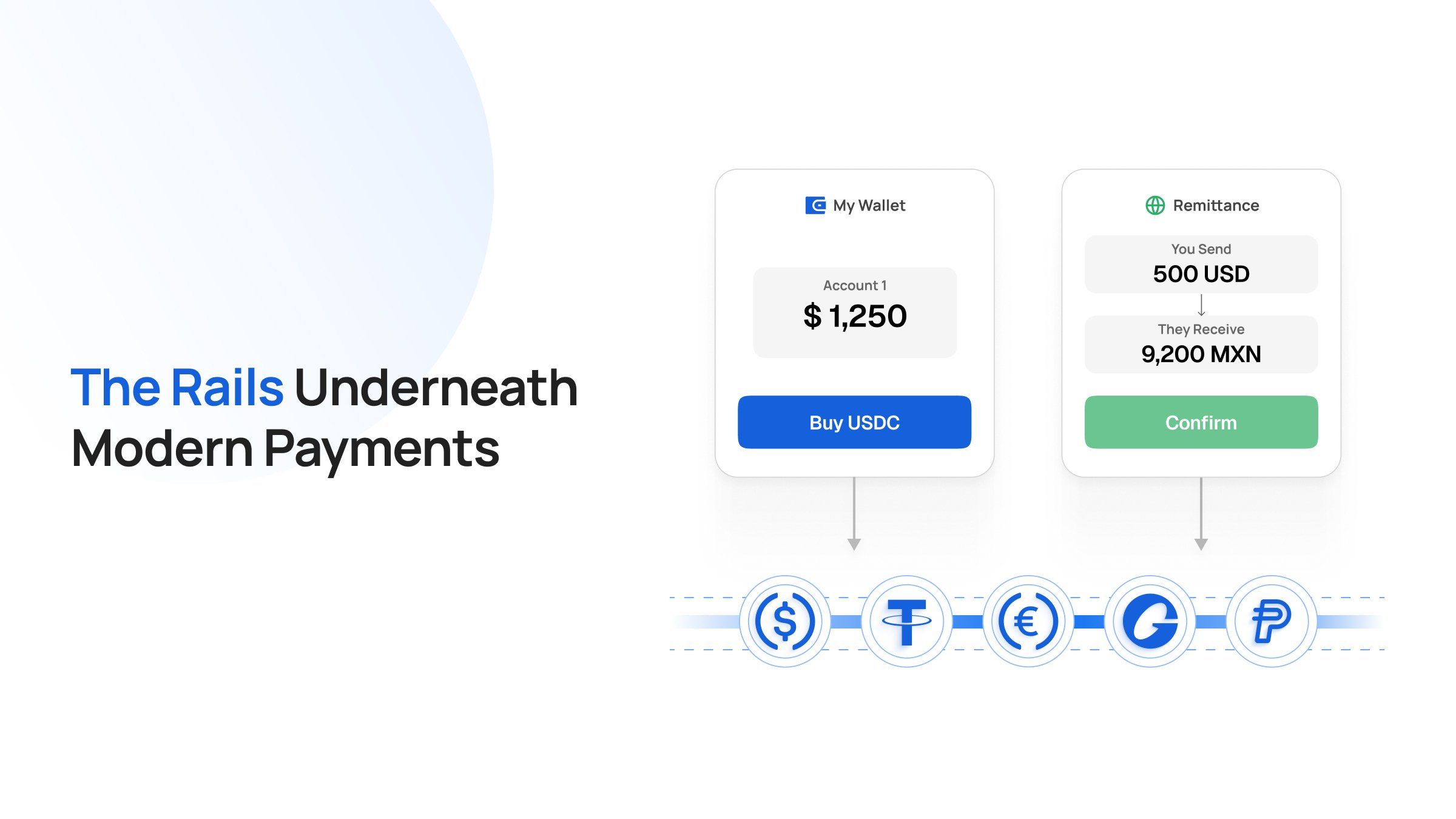

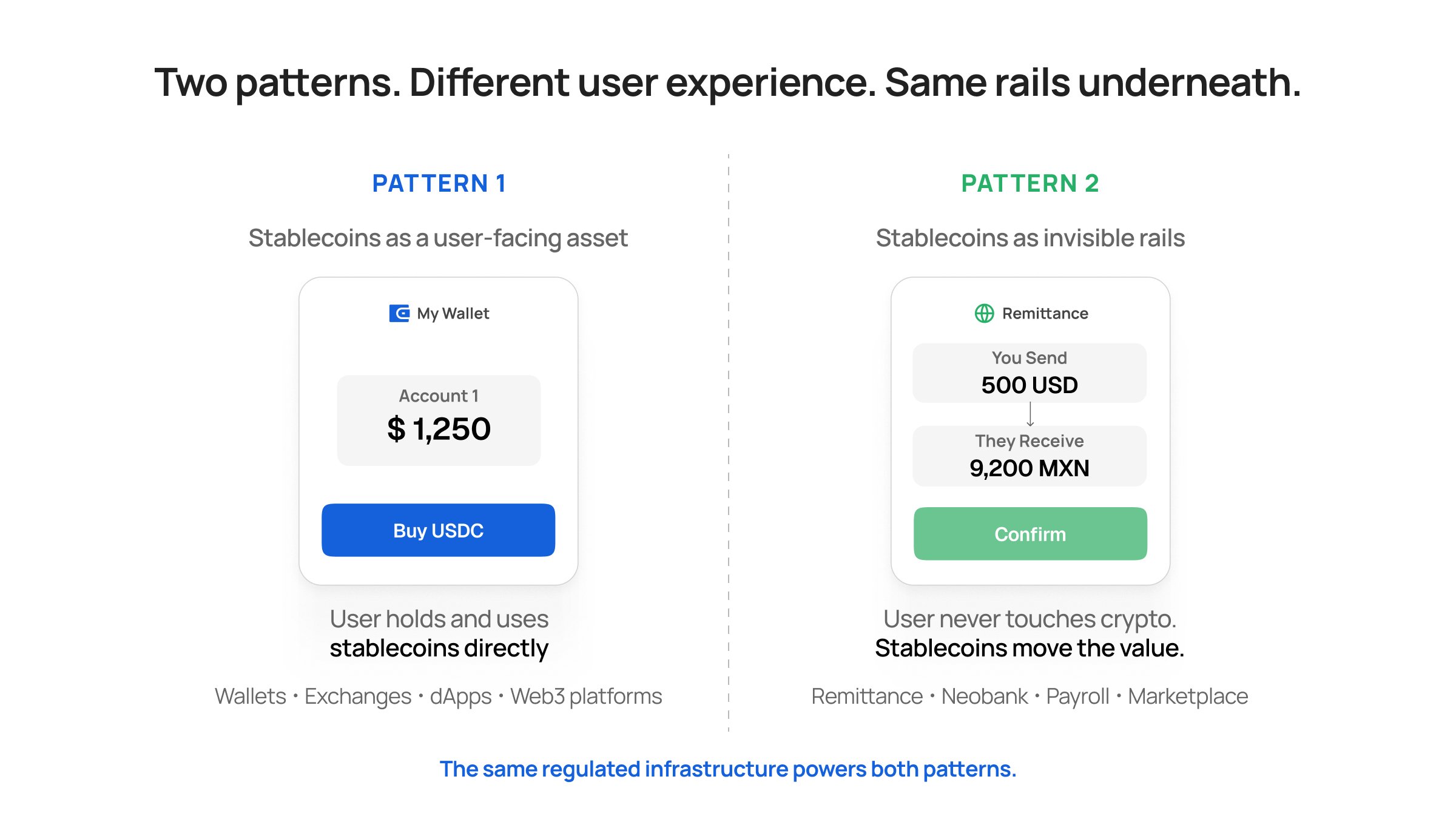

Depending on what you are building, stablecoins either sit in front of the user as the asset they hold, or sit underneath the product as the rails that move value.

That answers the question at a high level. Most founders evaluating this space run into category confusion before they get to integration, so the rest of this guide unpacks the choices that shape your timeline, your compliance footing, and whether the finished flow feels like one app or two.

What Is A Stablecoin On-Ramp?

A stablecoin on-ramp is a regulated service that accepts fiat from a user (card, bank transfer, local payment methods) and delivers stablecoins to a wallet address you specify. The on-ramp runs KYC, screens for fraud, holds the money transmission licenses required in each market, and manages the banking partnerships behind the fiat side.

What Does "Stablecoin Payments" Actually Mean For A Fintech App?

The phrase covers two integration patterns. The right one depends on what your product does and who uses it.

Pattern 1: stablecoins as the user-facing asset.

The user actively buys, holds, sends, or interacts with stablecoins. This is the natural model for self-custodial wallets, exchanges, dApps, on-chain savings products, and Web3 platforms where the user already has a wallet address and understands they are using crypto. Integration here centers on a clean fiat-to-stablecoin onboarding experience inside your app.

Pattern 2: stablecoins as invisible payment rails.

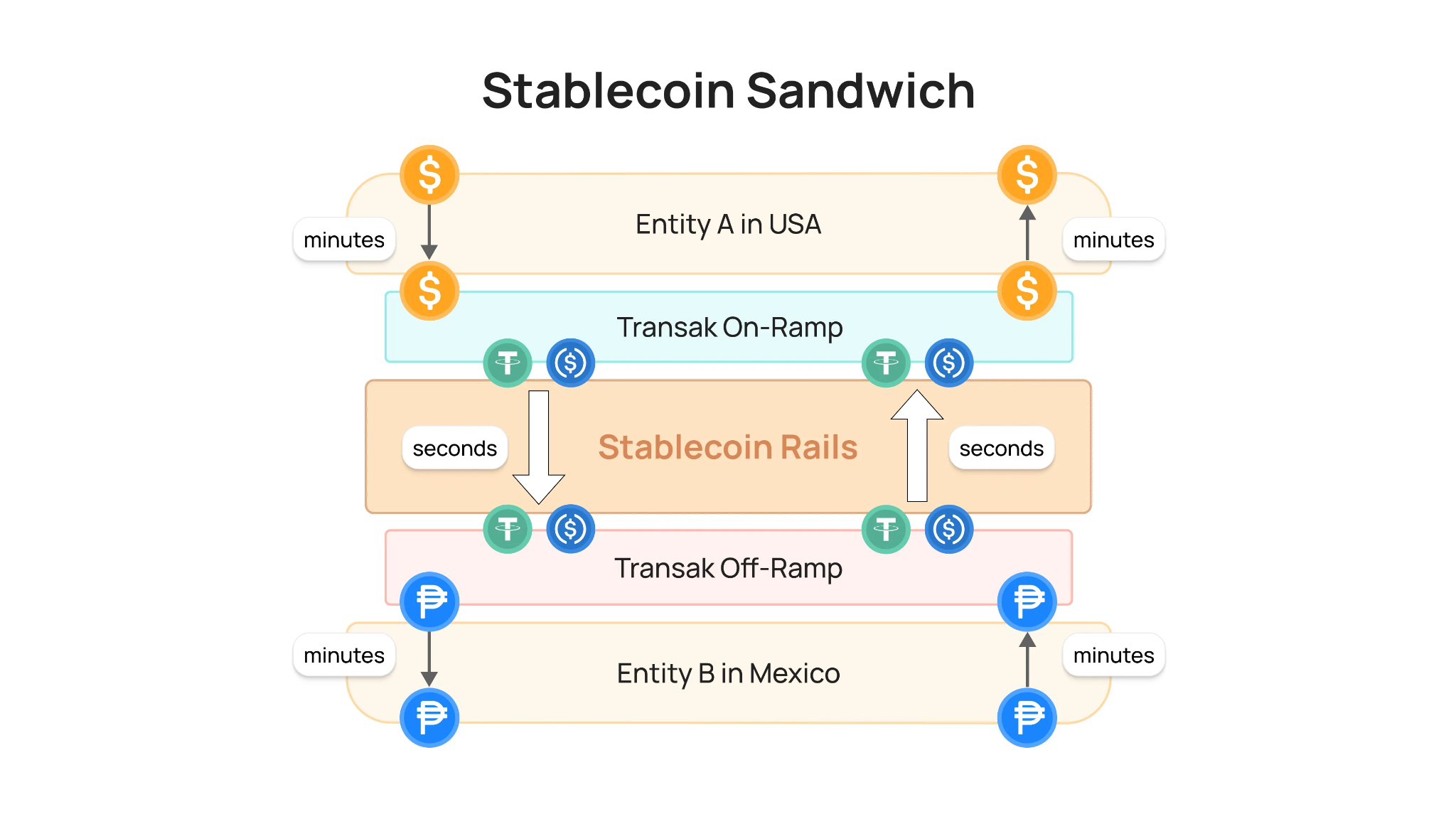

The user pays in local currency. The recipient receives in local currency. Stablecoins move the value across in between, without the user ever touching crypto. This is the model for remittance apps, neobanks, payroll platforms, marketplaces, and B2B cross-border products. The user experience stays familiar fiat. The infrastructure underneath shifts to faster, cheaper, programmable rails. This pattern is sometimes called the "stablecoin sandwich": fiat in, stablecoin in the middle, fiat out.

On-Ramp vs Crypto Aggregator: Which One Do You Need?

Founders often treat on-ramps and crypto account aggregators as substitutes. They sit in different product categories and solve different problems.

A crypto account aggregator (the "Plaid for crypto" model) connects to wallets and exchange accounts a user already has. It reads balances and can move funds between accounts the user controls. It does no first-time fiat onboarding, runs no KYC for new buyers, and processes no card payments. If your user has never bought crypto, an aggregator cannot help them.

A stablecoin on-ramp turns fiat into stablecoins for new and existing users. It accepts payment, verifies identity, delivers stablecoins to a wallet, and owns the regulatory side of the conversion.

If your product needs to onboard users who have never touched crypto, you need an on-ramp.

Do I Need To Become A Money Transmitter To Offer Stablecoin Payments?

When you integrate a regulated on-ramp, the provider holds the licenses (MSB, money transmitter, VASP, or the local equivalent in each market), runs the AML program, and takes regulatory liability for the conversion. Your app is software that integrates a financial service. The provider is the financial institution.

Note that this is a generalization and may differ depending on jurisdiction.

Building the rails yourself takes years, requires bank partnerships you cannot win at low volume, and exposes a small team to a fraud surface they cannot defend at scale.

When you evaluate providers, ask if you are the regulated entity, or are you reselling another company's license?

A direct provider holds the licenses in their own name. You contract with them, and you call them when something goes wrong. A reseller depends on a chain you cannot see, and that chain breaks the moment the underlying entity hits a problem, like paused payouts, a regulatory action, or a partnership change. Your product feels it, and you have no seat at the table when it gets resolved.

Transak operates as a direct, regulated on-ramp across 64+ countries with multiple active licenses. Use that as the verification bar for any provider you evaluate. Basically, licenses held in their own name, in the markets you serve.

How Long Does The Integration Take?

1. Embedded Widget: <1 Week

The provider hosts the flow, and you open it inline or in a redirect with the user's wallet address and any context you want to pass. Good for validating the end-to-end flow quickly.

2. API Integration: A few weeks for a polished version

You build the UI yourself and call the provider's APIs for KYC state, payment status, and settlement events. This path suits teams that want zero provider UI inside their product.

Most teams ship the widget first, prove the flow with real users, and migrate toward API integration on the surfaces where they want full control.

How To Make Stablecoin Payments Feel Native To The App?

A native experience comes down to four engineering choices. Users read the seam between two products at the points where these break:

- Domain: Does the flow live on your domain or on a third-party URL? Subdomain support (something like pay.yourapp.com) matters for user trust and for browser behaviors such as autofill and saved cards.

- Branding: Does your branding carry through every surface, including KYC, payment, success, and error screens? White-label theming should cover the full flow, end to end.

- Context pass-through: Can you send user data you already collected (email, country, wallet address) so the user skips re-entry? Re-entry is where conversion drops.

- Failure paths: When something fails (KYC rejection, declined card, geo-block), does the error surface in your UI with a copy you control, or does the user hit a generic provider error screen with no route back into your flow?

A provider that handles all four delivers an integrated user experience as one app. Miss two of them, and users feel they left.

Get Started

Stablecoin payments come down to whether you want to build the regulated infrastructure yourself, or integrate a provider that already has it. For nearly every fintech founder, the answer is to integrate. The licensing, banking partnerships, fraud surface, and ongoing compliance work that sit underneath stablecoin payments take years to build and millions to maintain. None of that is what your product competes on.

Transak already handles that layer for 600+ apps across wallets, remittance platforms, neobanks, payroll products, and marketplaces. One integration covers on-ramp, off-ramp, virtual accounts, compliance, and more across 64+ countries with 18+ active licenses, all held directly. You ship the product. We handle the rails.

Talk to our team to scope your integration, or read the developer docs to start building with the widget today.