Takeaways

Dedollarization (countries reducing their reliance on the U.S. dollar) was becoming a looming threat to the U.S. economy.

By establishing clear federal guidelines and shifting oversight to the CFTC, the GENIUS Act does more than just legitimize stablecoins. It unlocks a new chapter for the U.S. economy where digital dollars can move at internet speed, reduce reliance on legacy banking rails, and reinforce the dollar’s dominance.

The GENIUS Act brings regulatory clarity and outlines the expectations for stablecoin issuers in terms of safeguards, compliance, and eligibility.

Post-implementation, a regulated stablecoin would be:

- 100% backed by reserves

- Audited monthly

- Strictly labeled

- Follow clear disclosure guidelines

- Have consumer protection and anti-fraud safeguards

Let’s dig in.

Regulated Stablecoins Would Offset USD’s Friction

Despite fueling 50% of international transactions, the USD isn’t seamless or universally accessible. A simple cross-border transaction in USD can invite charges north of 10% and take up to 2 or 3 days’ settlement time.

Source: MSN

On the other hand, stablecoins are already enabling billions worth of value exchange daily via faster, frictionless payments across borders, 24/7, without the need for a third party or correspondent bank, at a fraction of the cost.

The Russia-Ukraine war was a wakeup call for the billionaires sitting on their dollars but being able to do nothing. Stablecoins, on the other hand, are unimpacted by war. They are neutral, borderless currencies.

Currently, stablecoins make up about 3% of the total cross-border payments. For mainstream adoption, stablecoins need to be embedded in systems that people trust, protect users, resolve disputes, and work seamlessly across borders and platforms.

The GENIUS Act lays clear guidelines for innovators and institutions to kickstart the ‘digital switchover’ to crypto rails.

Preserving Dollar’s Dominance As The World Reserve Currency

USDT (Tether) remains one of the biggest holders of short-term US Treasuries. Circle and other stablecoin players aren’t far behind. Donald Trump sees a huge opportunity to establish dollar dominance via the GENIUS Act.

98% of the stablecoins are pegged to the US Dollar. 100% backed stablecoins means the demand for US treasuries would be manifold. If McKinsey’s $2 trillion market cap prediction by 2028 comes true, there’s a direct demand for nearly $2 trillion worth of USD, treasuries, and bonds. The GENIUS Act would further accelerate adoption, triggering even greater demand for treasuries.

Also, the US Dollar corridor has been shrinking globally. Stablecoins can restore financial pathways and grant access to economies where USD markets do not exist.

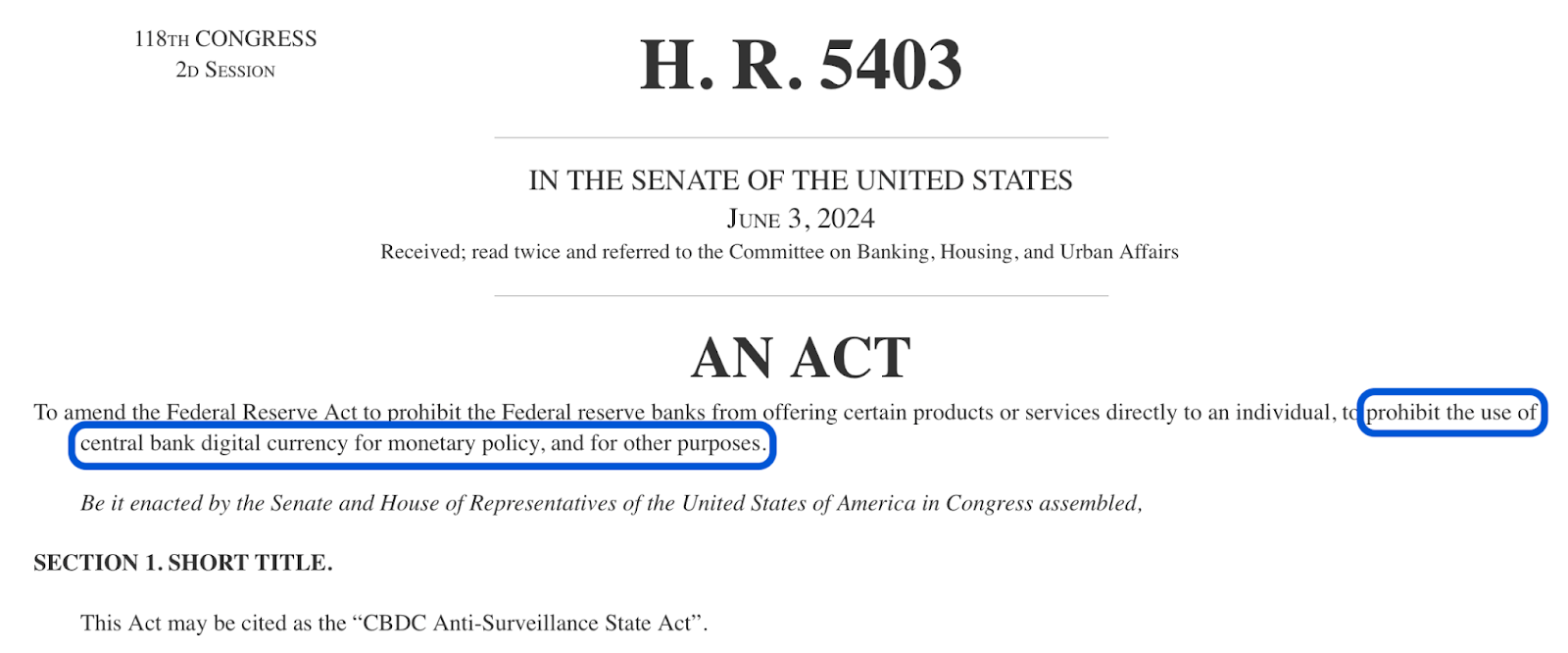

Stablecoins In, CBDCs Out!

President Trump is also planning an anti-CBDC bill, as per which the Federal Reserve won’t be allowed to issue a CBDC, and would be obligated to support stablecoins use cases. Further, stablecoin adoption is highest in the US and is expected to increase further when the Act takes effect.

Source: Congress

The Act embraces the existing stablecoin infrastructure and regulates it. It adds ‘functional surveillance capabilities’ without the scary name (read CBDCs) and faster private sector deployment. Stablecoins will act as proxy payment networks sanctioned by the government without the heavy lifting involved in CBDCs.

Also Read: What Are Dark Stablecoins?

The GENIUS Act is a perfect act of neutering the stablecoin threat and turning it into an opportunity.

Stablecoins As Payment Rails For Banks

Banks and businesses, which were resisting crypto earlier, can now launch branded stablecoins. JP Morgan, Stripe, Standard Chartered, Revolut, Circle, PayPal, and Shopify are already in the stablecoin business.

The rest of the lot is readying to launch or embrace the ‘exorcised’ stables. As Brian Moynihan, chief executive of Bank of America, says, ‘If they make that legal, we will go into that business.’

Once stablecoin integrations kick in, banks can bypass traditional card and payment systems, and opt for a regulated issuance to manage B2B and B2C money flows. They can put their US treasury reserves to good use that way.

US Bank consolidations and failures have pushed the banking systems to the brink. The pro-consumer and transparent mechanisms will help mitigate systemic risks. Banks can also access DeFi, and save costs on payments once stablecoin rails are integrated.

Crypto Firms Aren’t Shying Away

Crypto firms like Circle and Bitgo are pursuing banking charters which would make them fall in line with fintechs who have an account with the Fed.

A stablecoin is a payment rail in itself. Banks are going to lose business to crypto issuers if they don’t adapt. 10% of bank deposits are expected to flow into stablecoins with time.

Also Read: The New Dollar Standard: How Stablecoins Are Becoming Global Money

Conclusion

While the EU’s MiCA framework set the global momentum for stablecoin adoption, the GENIUS Act will be the opening Act in the story of stablecoin adoption.

You won’t be able to buy your coffee with stablecoins immediately (unless you use a crypto card), but we are nearing a time when payments are going to get a big makeover, courtesy the GENIUS act.