Takeaways

The stablecoin market crossed $320 billion in total market capitalization in March 2026, nearly 50% higher than a year ago. A growing share of that volume is moving through cross-border payment corridors that were once the exclusive domain of correspondent banks and licensed money transmitters.

Regulators have noticed, and they're not standing still.

If you're a remittance company, payroll platform, or fintech exploring stablecoin rails for cross-border transfers, the compliance picture has shifted dramatically over the past 12 months. New laws are live and enforcement is tightening.

Looking for regulated infrastructure for your remittance app? Start here.

This article breaks down the actual regulatory requirements for stablecoin remittances in 2026 so you can build (or evaluate) your compliance stack with precision.

The U.S. GENIUS Act

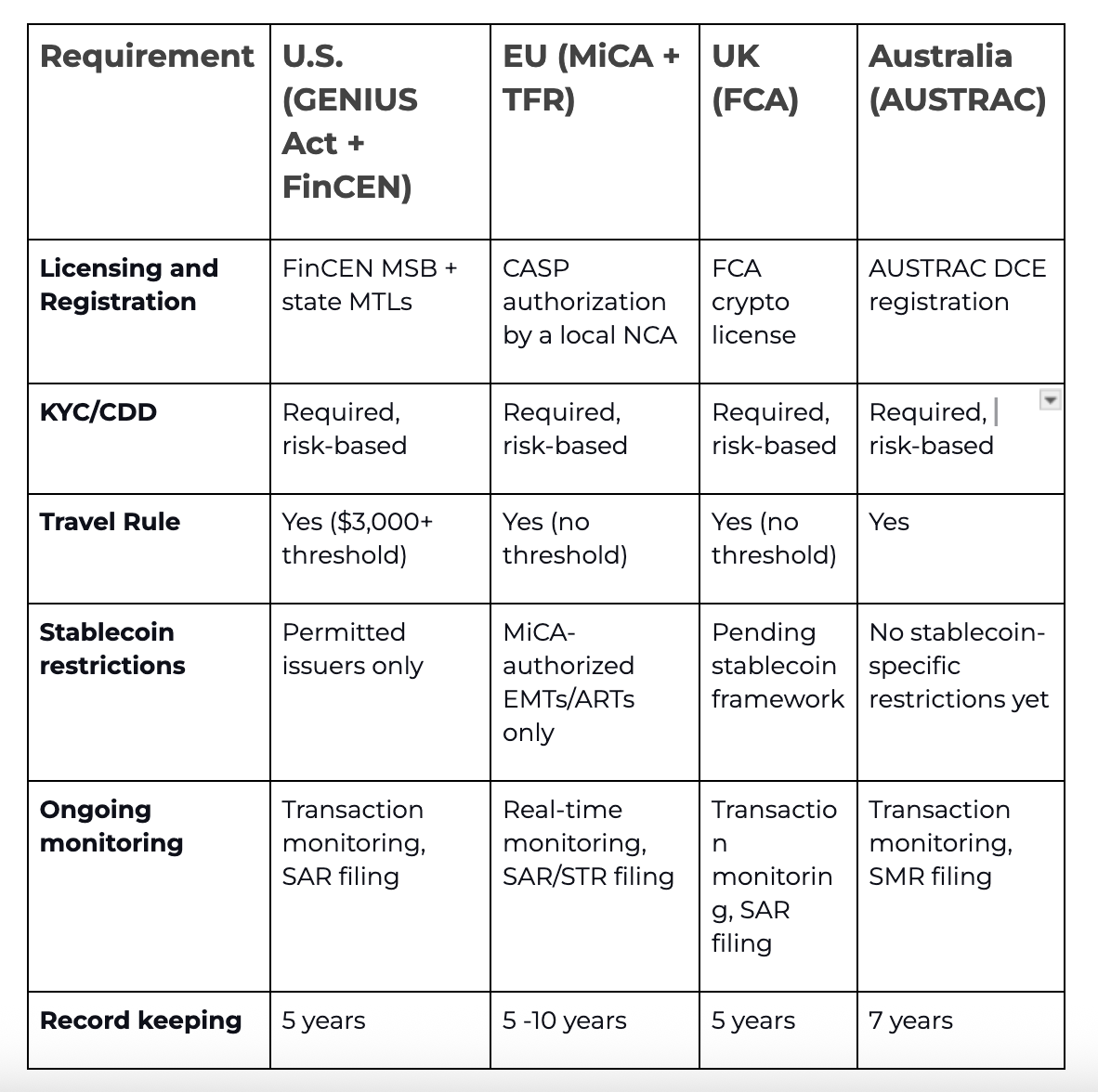

The GENIUS Act, signed July 2025, is the first federal law regulating digital assets. It mandates that stablecoins only be issued by "permitted issuers" meeting strict reserve and audit standards. Federal banking regulators oversee large issuers (over $10B), while states handle smaller ones. Implementation concludes by early 2027.

MiCA Enforcement in the EU

The EU's Markets in Crypto-Assets Regulation (MiCA) entered into force on December 30, 2024, creating a comprehensive framework for crypto assets services and implicitly stablecoin remittances.

- Mandatory Authorization: All Crypto-Asset Service Providers (CASPs) must be authorized by a national competent authority in any of the member states to operate legally.

- Token Classification: MiCA distinguishes between e-money tokens (EMTs) and asset-referenced tokens (ARTs), requiring issuers to obtain the necessary license to operate in the EU.

- Compliance Shifts: USDC, EURC, or Paxos's USDG, because of their regulated status are preferred by regulated exchanges.

For platforms building stablecoin payment rails in Europe, MiCA compliance isn't optional. It's the cost of doing business.

The Travel Rule Is Now Live in 64+ Jurisdictions

The FATF's Travel Rule (Recommendation 16) is enforced in over 64 jurisdictions, including the U.S., UK, Singapore, Japan, South Korea, Canada, India, UAE, and many others.

Here's what the Travel Rule requires for stablecoin remittances:

- Originator and beneficiary data must travel with the transactions: VASPs must collect and transmit the originator and beneficiary’s name, unique identifier (or national identity number, date and place of birth, or customer identification number), and address .

- No threshold exemption in many jurisdictions: While the traditional banking Travel Rule kicks in at $3,000 in the U.S. Several crypto-specific implementations apply at lower thresholds or have no threshold at all. The EU's Transfer of Funds Regulation (TFR), which works alongside MiCA, requires originator and beneficiary information for all crypto transfers regardless of amount.

- Unhosted wallets trigger additional obligations: Transfers to or from self-custodied wallets face enhanced scrutiny. Some jurisdictions require proof of wallet ownership. Others require risk-based due diligence above certain thresholds.

- Australia and Brazil join the list in 2026: Australia's Travel Rule implementation will take effect in early 2026, under AUSTRAC's expanded regulatory remit. Brazil's local regulation came into force on February 2, 2026. Both markets are significant remittance corridors.

Every reputable CASP compliance stack needs a Travel Rule solution that can exchange data with counterparty VASPs in real time. Manual processes don't scale and pose serious data security and protection issues, and regulators are now actively supervising compliance rather than just publishing guidelines.

The UK Runs Its Own Playbook

The UK's Financial Conduct Authority (FCA) regulates crypto assets under the Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017. Crypto businesses must register with the FCA, and the bar for approval is high. The FCA has rejected more crypto registration applications than it has approved. The FCA has announced a new registration regime which applies to CASPs and issuers, which is expected to come into force in Q3 2026.

For stablecoin remittances touching the UK:

- Adequate authorizations are non-negotiable: The FCA will assesses AML controls, governance, prudential, risk and cyber security arrangements and the fitness and propriety of key personnel among other requirements specific to the business model of the applicant

- The UK Travel Rule is live: Since September 2023, crypto service providers operating in the UK must comply with the Travel Rule for all transfers, regardless of value. The UK does not recognize a de minimis threshold for crypto.

- Financial promotions regime: Since October 2023, all crypto marketing targeting UK consumers must comply with the FCA's financial promotions regime. This applies even if your company is based overseas. Failure to comply can result in criminal penalties.

The UK is also developing its own comprehensive regulatory framework separate from MiCA. A full stablecoin regulatory regime is expected to be finalized in 2026, which could introduce issuance and reserve requirements similar to (but distinct from) MiCA.

Australia's AUSTRAC Framework Is Tightening

Australia has been actively expanding its regulatory perimeter around digital currency exchanges. A registration with AUSTRAC as a Digital Currency Exchange (DCE) provider has been mandatory since 2018, but enforcement and expectations have since ramped up considerably.

Key requirements:

- AUSTRAC registration: All businesses exchanging fiat for crypto (or crypto for fiat) must obtain an adequate authorization. Remittance services that use stablecoins as an intermediary rail are among those who need to register.

- AML/CTF programs: Registered entities must maintain comprehensive AML/CTF programs, including customer identification procedures, ongoing customer due diligence, transaction monitoring, and suspicious transaction reporting.

- Travel Rule (from March 2026): Australia's implementation aligns with the FATF standard but adds local reporting requirements. The stablecoin remittance corridor between Australia and South/Southeast Asia covers some of the highest-volumes in the world at $25 billion annually, making compliance here a strategic priority.

Singapore and Hong Kong: Asia's Important Licensing Regimes

Singapore operates under the Payment Services Act (PSA), administered by the Monetary Authority of Singapore (MAS). Digital payment token (DPT) service providers must hold either a Standard Payment Institution license or a Major Payment Institution license, depending on volumes of transactions processed and customers serviced. MAS has been among the most proactive regulators globally, having set clear guidelines for stablecoin issuance, custody, and cross-border transfers early.

Hong Kong introduced its crypto licensing regime under the Anti-Money Laundering and Counter-Terrorist Financing Ordinance. Virtual asset trading platforms must obtain a license from the Securities and Futures Commission (SFC). The regime includes specific requirements for stablecoin transactions and cross-border compliance.

Both jurisdictions enforce the FATF Travel Rule and maintain stringent AML/CFT standards.

India's VDA Framework Adds Reporting Obligations

India classifies crypto as Virtual Digital Assets (VDAs) and requires all VDA service providers to register with the Financial Intelligence Unit (FIU-India). The registration mandates:

- KYC procedures aligned with existing banking standards

- Suspicious transaction reporting to FIU-India

- Record maintenance for a minimum of five years

- Compliance with the Prevention of Money Laundering Act (PMLA)

India's Travel Rule implementation is live, and the FIU has blocked non-compliant foreign platforms from operating locally. In early 2024, India ordered the blocking of nine foreign crypto exchanges that failed to register with FIU-India, including Binance and KuCoin (both having later registered and resumed operations).

For stablecoins remittances to Indian resident recipients, the tax regime adds another layer of scrutiny. India applies a 1% TDS (Tax Deducted at Source) on all crypto transfers and a flat 30% tax on gains from digital assets operations. These aren't compliance requirements for a virtual assets trading platform directly, but they affect user adoption and corridor economics.

What A Compliant Stablecoin Remittance Stack Actually Looks Like

Knowing the rules is one thing. Building a system that satisfies all of them simultaneously is another.

Here's what regulators across jurisdictions are converging on as the baseline:

This shows why multi-jurisdictional compliance is a real challenge. Each corridor served potentially adds a new regulatory layer and local specific requirements. A transfer from the U.S. to the Philippines requires U.S. licensing, Philippine BSP registration, Travel Rule compliance on both ends, and AML screening.

This is exactly why many remittance companies prefer to plug into existing compliance infrastructure rather than building them. Licensing alone can take 12-18 months per jurisdiction. The ongoing compliance burden, including regulatory reporting, audit preparation, and sanctions screening, requires dedicated teams.

Infrastructure providers that hold licenses across multiple jurisdictions and offer compliance-as-a-service are becoming the preferred approach for platforms that want stablecoin capabilities without rebuilding their compliance function from scratch.

The Sanctions Screening Layer Most Platforms Underestimate

Every customer and crypto transfer including every stablecoins remittance must be screened against sanctions lists. While not a new practice the on-chain dimension adds complexity to the screening process.

Among others, OFAC (U.S.), the EU's consolidated sanctions list, and the UK's HMT sanctions list all apply. OFAC has sanctioned specific crypto wallet addresses since 2022, and enforcement actions have followed.

For remittance platforms, this means:

- Pre-transaction wallet screening against OFAC, EU, UN, UK and other sanctions lists.

- Ongoing monitoring of wallets later added to sanctions lists.

- Blockchain analysis to detect interactions with sanctioned addresses, mixers, or high-risk protocols.

- Geographic screening to restrict transactions to/from comprehensively sanctioned jurisdictions

Sanctions compliance is non-negotiable and the penalties are severe. OFAC violations can result in fines of up to billions of dollars, remediation plans (including financial investments to correct/reinstate compliance processes) and criminal penalties of up to 30 years' imprisonment.

Future Outlook

Looking ahead to 2026, global stablecoin regulation is expected to significantly tighten as several key frameworks reach maturity.

In the United States, the industry expects final implementation details of the GENIUS Act to clarify reserve standards and issuer obligations by mid-year. Simultaneously, the UK is finalizing its own bespoke regulatory regime focused on custodial standards, while Singapore and Hong Kong have stated they are refining their licensing frameworks with the first stablecoin-specific licenses expected from the MAS.

These regional shifts are occurring alongside continued pressure from the FATF, which remains focused on ensuring strict Travel Rule enforcement across all jurisdictions.

The Compliance Advantage

There's a reason the fastest-moving remittance companies are treating compliance as a competitive advantage rather than a cost center.

Licensed infrastructure is harder to build than fast settlement. Anyone can move stablecoins on-chain in seconds. But doing it legally, in 64+ countries, with proper KYC, Travel Rule data exchange, sanctions screening, and regulatory reporting in place is the actual goal.

FAQs

What licenses do I need to send stablecoin remittances in the U.S.?

You need FinCEN registration as a Money Services Business plus individual money transmitter licenses in each state where you operate. The GENIUS Act (signed July 2025) adds requirements around permitted stablecoin issuers, which take full effect by early 2027.

Does MiCA apply to stablecoin remittance companies outside the EU?

Yes, if you offer services to EU customers. MiCA's scope includes third-country firms offering services to EU residents. Such entities need CASP authorization in at least one EU member state, which can afterwards be passported across all 27 countries.

What is the FATF Travel Rule and how does it affect stablecoin transfers?

The Travel Rule (FATF Recommendation 16) requires VASPs to collect and transmit originator and beneficiary information with every virtual asset transfer. The EU applies it with no minimum threshold. The U.S. applies it above $3,000.

Which stablecoins are compliant for cross-border payments?

It depends on the jurisdiction. In the EU, only MiCA-authorized stablecoins qualify. USDC (Circle) and EURC compliant with MiCA standards. In the U.S., the GENIUS Act will require stablecoins from permitted issuers only.

How long does it take to get licensed for stablecoin remittances?

Licensing timelines vary across jurisdictions. The FCA registration can take 12+ months. EU CASP authorization varies by member state but typically takes 6-12 months. U.S. state money transmitter licenses can take 12-24 months to acquire across all required states. Many platforms chose partnership models with licensed infrastructure providers to address additional burdensome licensing requirements.