Takeaways

Australia is now one of the fastest-growing remittance-sending nations in the world.

The country’s overseas-born population, which hit 8.6 million in 2024 (31.5% of the country) and that resulted in more than US$25 billion (A$38.2 billion) in personal remittances being abroad in the same year.

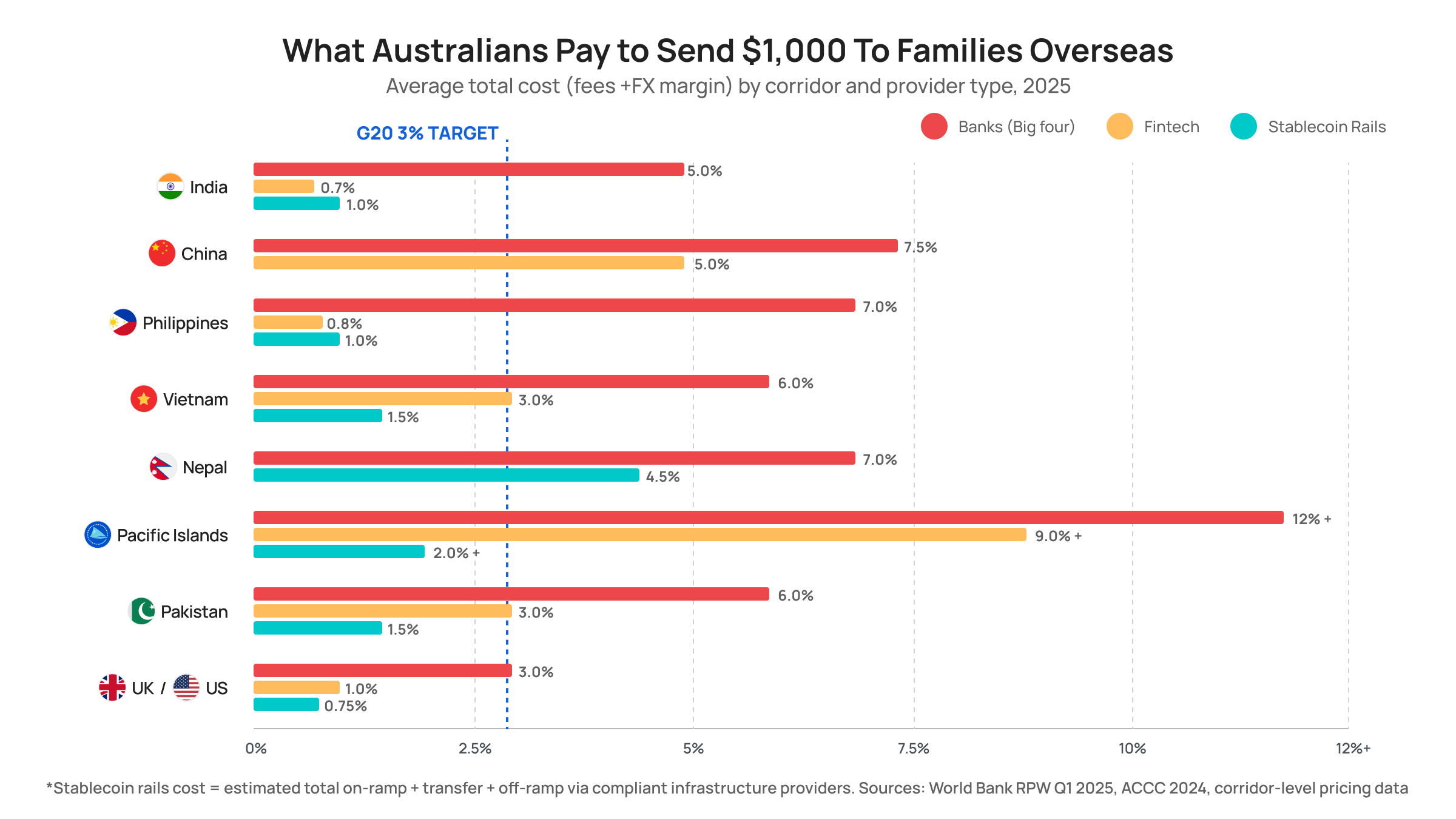

Unfortunately, Australians still face average costs of 5.11% on a $200 transfer, settlement windows stretching to seven business days through banks, and Pacific Island corridors where fees exceed 9-12%!

The gap between what payments could cost and what they actually cost is as inefficiency that is easily addressable via stablecoins.

The Real Cost Isn't the Fee, It's the FX Margin

Most Australians don't realize what they're actually paying to send money overseas. The ACCC's 2024 transparency report on international money transfers made this painfully clear.

The Big Four banks have largely eliminated flat fees for online transfers. That sounds like progress until you look at the exchange rate. Commonwealth Bank applies a 3–5% markup above the mid-market rate. On a $10,000 transfer, that hidden FX margin translates to A$300–500 in invisible costs.

Fintechs have compressed this dramatically. Wise charges an average of 0.58% with zero FX markup, and other fintech competitors have pushed effective costs even lower on some corridors. But even the best fintechs are still routing through traditional banking rails underneath. They've optimized the interface but the plumbing remains the same.

Also Read: Why FinTechs Are Turning To Stablecoins

Where Australia's A$38 Billion Actually Goes

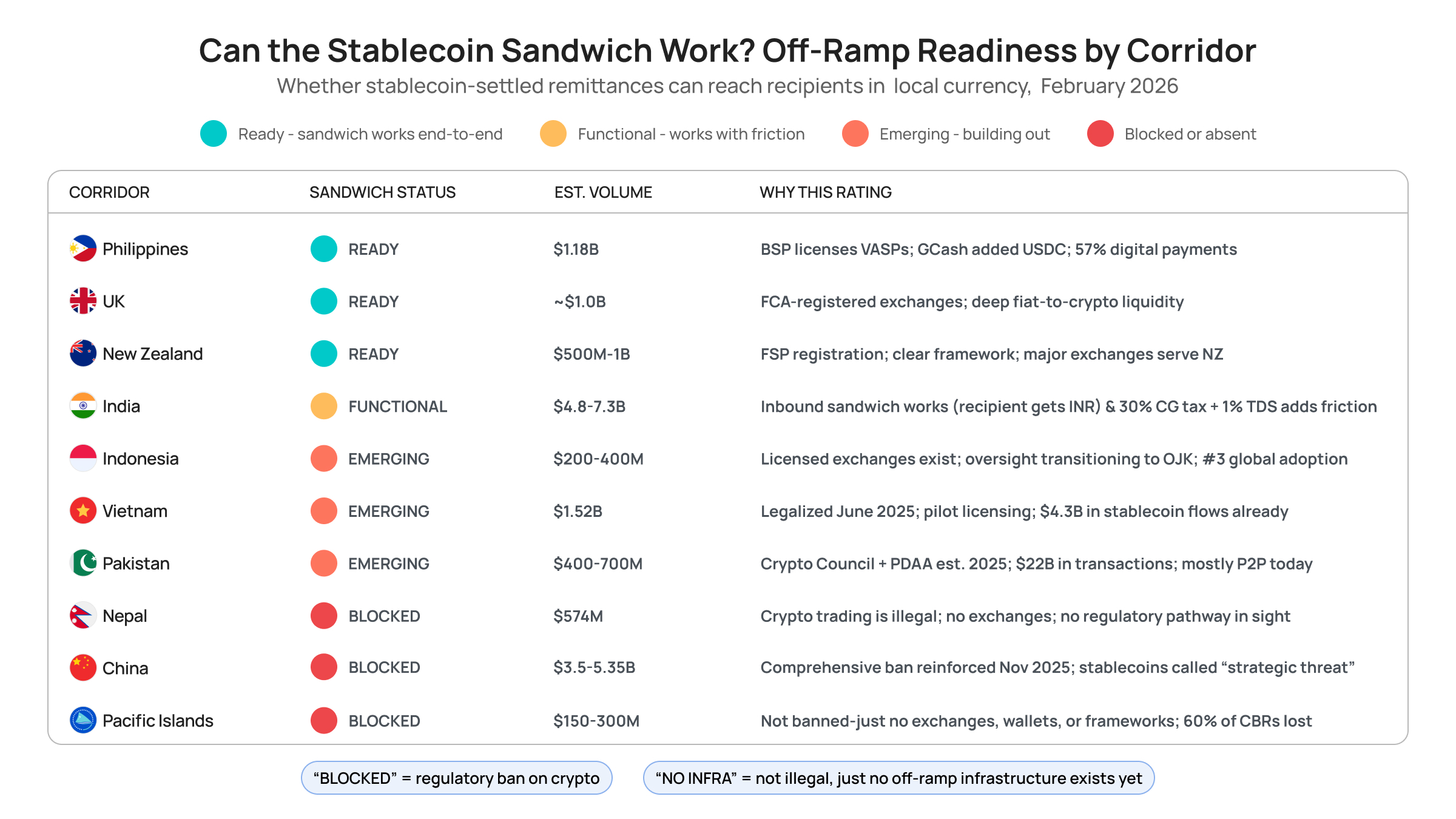

Not all corridors are created equal. Some are high-volume and well-served. Others are high-cost and actively losing banking infrastructure. The stablecoin opportunity depends entirely on which corridor you're looking at.

We observe three patterns in this data.

The corridors with the highest volume aren't necessarily the ones with the biggest stablecoin opportunity. India is the largest corridor but faces complex crypto taxation. China is the second-largest but entirely blocked.

The corridors with the highest costs have the weakest off-ramp infrastructure. Pacific Islands pay 9–12% in fees but have lost 60% of their correspondent banking relationships and have no crypto regulatory framework. Nepal's remittances exceed 20% of GDP but crypto is illegal. The places that need stablecoin rails the most are the places least equipped to receive them.

Regulatory momentum is accelerating across the board. Vietnam legalized crypto in June 2025. Pakistan established a full digital assets authority. Indonesia is transitioning oversight to the OJK. The off-ramp landscape 18 months from now will look fundamentally different from today.

The Correspondent Banking Model Is Breaking

High fees are one problem. But the bigger, less-discussed issue is that the traditional payment infrastructure is actively contracting in the corridors that need it most.

Globally, correspondent banking relationships (CBRs) have declined 20–30% since 2012. Pacific Island nations lost 60% of their CBRs. Nauru's only bank (Bendigo Bank) announced its exit in 2024, triggering a scramble that was only resolved when Commonwealth Bank of Australia stepped in as a replacement in August 2025.

Banks cite AML/CTF compliance costs as the primary driver. Maintaining correspondent relationships in small, low-volume markets requires the same compliance infrastructure as high-volume corridors, but generates a fraction of the revenue. The economics don't work. So banks leave.

This is the context that makes stablecoin payment infrastructure necessary for connectivity. Stablecoins settle on a shared ledger. They don't require nostro/vostro accounts or bilateral banking relationships across jurisdictions. Any entity with internet connectivity and a licensed on/off-ramp partner can send and receive value.

The FSB's 2025 progress report on the G20 cross-border payments roadmap acknowledged that reaching the target of 75% of payments arriving within one hour by 2027 is unlikely through traditional rails alone. The infrastructure gap isn't closing fast enough.

How the "Stablecoin Sandwich" Actually Works

"Stablecoin sandwich" is a payment architecture that utilizes blockchain-based assets but the end user never touches crypto. Fiat in → stablecoin transfer → fiat out. The infrastructure handles conversion, compliance, and settlement.

Here's what changes when you swap out the SWIFT chain for stablecoin rails.

Also Read: The Stablecoin Playbook for 2026

1. Settlement drops from days to seconds.

A traditional SWIFT transfer from Australia to Nepal goes through an Australian bank, a USD correspondent in New York, and a Nepali correspondent before reaching the beneficiary after 3 to 7 business days. On-chain stablecoin settlement completes in under three minutes and operates 24/7/365.

2. Intermediaries go from five to zero.

Each correspondent bank in the SWIFT chain adds latency, compliance processing, and margin. The stablecoin model has exactly two conversion points (the on-ramp and the off-ramp) with the transfer itself costing fractions of a cent.

3. Compliance becomes programmable.

Rather than each intermediary independently screening transactions (causing delays, false positives, and opaque rejections), smart contracts can embed compliance logic into the payment flow. The RBA's participation in Project Mandala with the BIS Innovation Hub demonstrates exactly this: automated regulatory checks at initiation, with cryptographic proofs of compliance traveling with the payment.

4. The cost structure flattens.

Transak can execute the full on-ramp-to-off-ramp cycle at 1–2% total cost compared to 5–12% on high-cost corridors. In the Philippines, stablecoin-routed remittances through on-/off-ramp infrastructure providers demonstrated an 80% fee reduction versus traditional channels.

Capture the AU Market with Transak

If you're building a remittance app, a cross-border payroll platform, a neobank, or any product that moves money across borders from Australia, you don't need to become a crypto company to use stablecoin rails. That's the whole point.

Transak is the infrastructure layer that handles the hard parts like regulated fiat-to-stablecoin conversion, KYC/AML compliance, and local payment method coverage across 64+ countries all through a single API. Your users pay in AUD. Recipients get local currency. The stablecoin settlement happens in between, invisibly.

We're AUSTRAC-registered, licensed across multiple jurisdictions for key corridor connectivity, and already integrated into 450+ platforms globally. Let’s talk.