Takeaways

You would not hire a law firm that also represents the other side. You would not share your product roadmap with a vendor who sells to your competitors.

Yet in crypto payments, companies routinely hand their most sensitive business data to infrastructure providers that are actively building consumer-facing products designed to replace them.

Multiple crypto payments infrastructure providers now operate consumer-facing applications alongside their B2B services. They process transactions for wallets, exchanges, and dApps while simultaneously running their own apps that target the same end users.

The problem is not that these providers are bad at infrastructure. Many of them are excellent at it. The problem is that a company that serves partners and competes with them at the same time cannot fully optimize for both.

The Conflict Is Built Into the Business Model

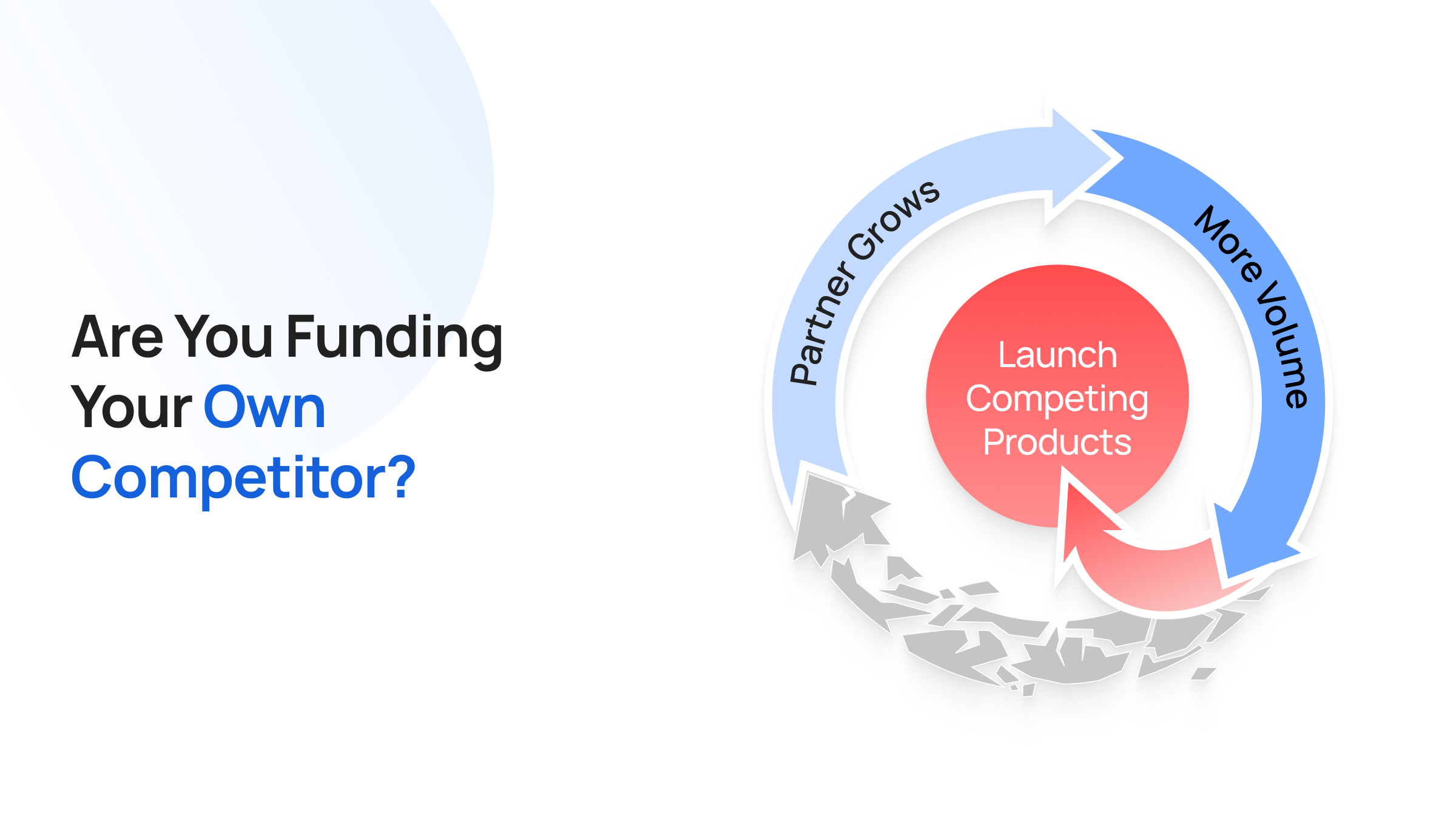

When a payments infrastructure provider launches a consumer product, two things happen immediately.

First, engineering and product resources get split. Every hour spent improving the consumer app is an hour not spent improving the partner-facing API. Every UX optimization in the consumer flow is a feature that partners do not get. Over time, the consumer product becomes the priority because it carries higher margins and drives the company's valuation narrative.

Second, the provider gains an unfair information advantage. A provider embedded in 1000+ partner applications sees aggregate transaction data that no single partner can access. All of this intelligence flows into the consumer product, giving it a head start that no organic competitor can match.

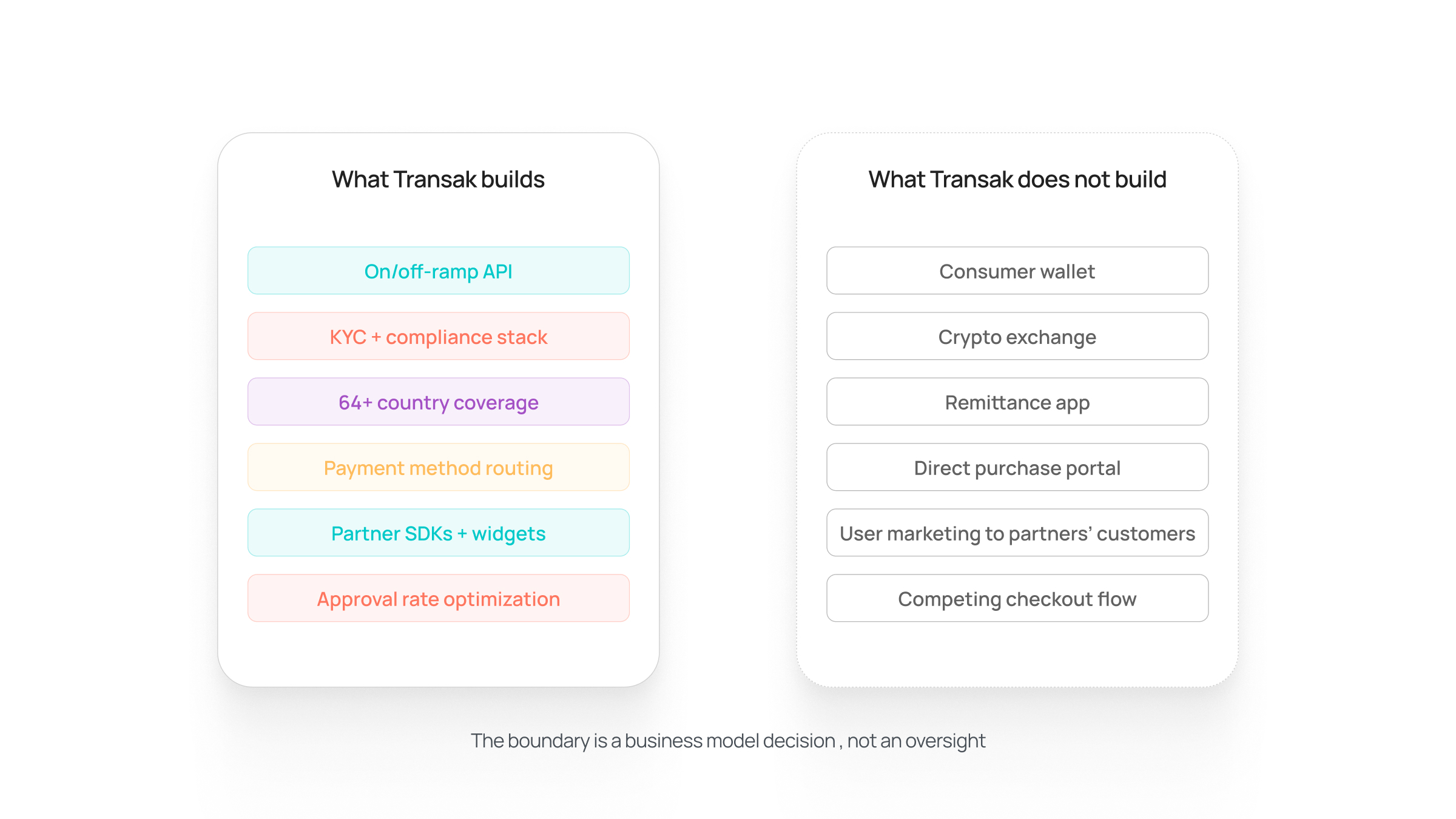

At Transak, our business model is infrastructure, not a consumer product.

What Your Provider Knows About Your Users

Consider what a typical crypto on-ramp integration shares with the infrastructure provider.

- Identity Data: Providers collect full KYC records, including government IDs and biometric verification, to know exactly who is transacting.

- Financial Data: Providers access bank details and card numbers to build a complete profile of user spending behavior across the ecosystem.

- Behavioral Data: Aggregated data on app preferences and token purchases allows providers to identify market trends before they become public.

- Contact Information: Email and phone data collected during onboarding is often retained by providers for their own marketing and lead generation.

Now imagine that same provider launches a consumer wallet or a direct purchase app. Every piece of data listed above becomes a competitive weapon. The provider can target the highest-value users from partner integrations. It can undercut partner pricing because it knows exactly what users are willing to pay. It can time product launches to coincide with trends it spotted across partner transaction data weeks earlier.

The Questions Your BD Team Is Not Asking

Most partnership evaluations focus on fees, geographic coverage, supported currencies, and integration complexity. These are table-stakes factors. They tell you nothing about whether the provider's long-term incentives are aligned with yours.

Here are the questions that actually matter.

Does the provider operate a consumer-facing product?

If yes, you are funding your own competition. Every transaction you send through their infrastructure generates revenue and data that strengthens their consumer business.

Does the provider require users to create an account with the provider?

If users must register with the provider (rather than your application) to complete a transaction, the provider owns that user relationship. Even if you switch providers later, the user's account, KYC data, and payment methods remain with the old provider.

Does the provider retain the right to market to users acquired through partner integrations?

Check the terms of service and the privacy policy. Some providers explicitly reserve the right to send promotional emails to users who completed transactions through partner apps. Your users become their leads.

Has the provider raised capital at a valuation that requires consumer-scale returns?

A company valued at $5 billion+ and raising hundreds of millions cannot justify to the investors based on B2B infrastructure margins alone. The math only works if the company plans to monetize users directly, i.e., go mass market.

Does the provider's off-ramp require account creation on their platform?

If a user can onramp through your app but must visit the provider's app to off-ramp, the provider has designed a funnel that pulls users away from partners and into its own ecosystem.

The Cost of Switching Late

The longer you stay with a conflicted provider, the harder it becomes to leave.

Users accumulate KYC records, saved payment methods, and transaction history with the provider. Switching to a new infrastructure partner means asking users to re-verify their identity, re-enter payment details, and rebuild their transaction history from scratch. Many will not bother. Some will follow the path of least resistance and continue using the old provider's consumer app instead of yours.

eBay learned this lesson in the payments world. After years of dependence on PayPal, eBay spent three years migrating to Adyen, a process that required re-architecting its entire payment stack. The transition was successful, but it was expensive and slow. Most crypto companies do not have eBay's resources.

The best time to evaluate infrastructure alignment is before integration. The second-best time is now.

What Infrastructure Alignment Actually Means

Infrastructure alignment is not a marketing term. It is a structural property of a business model.

An aligned infrastructure provider has the following characteristics.

- No consumer product: The provider avoids competing with partners by generating revenue primarily from B2B services.

- No user ownership: The partner maintains the primary brand relationship while the provider handles compliance requirements.

- No data exploitation: Transaction data is never used to inform competing products or benefit other partners.

- Transparent incentives: The business model and roadmap remain strictly focused on long-term infrastructure support.

How Transak Approaches This

Transak is built as pure-play payments infrastructure. There is no Transak consumer app on iOS or Android. There is no Transak wallet.

Every product in Transak's stack is designed to be embedded into partner applications. On-ramp, off-ramp, and programmatic payment rails all operate within the partner's UX, under the partner's brand. Users interact with your product, not ours.

Transak is integrated into 600+ applications serving over 10 million users across 64+ countries. Partners like MetaMask and others rely on Transak precisely because the infrastructure is designed to make their products better, not to compete with them.

Case Study: How MetaMask Launched ‘Deposit’ using Transak’s White-Label APIs to Redefine Stablecoin Onramping

Transak's revenue grows when partner revenue grows. There is no structural incentive to redirect users, no consumer product roadmap to fund, and no cap table pressure that requires direct user monetization.

When your infrastructure provider has no reason to compete with you, partnership becomes what it is supposed to be. A relationship where both sides win.

Want to evaluate whether your current payments infrastructure is aligned with your business? Talk to our team or explore our integration docs.