Takeaways

In 2024, personal remittance outflows exceeded $850 billion globally, according to the World Bank. Cross-border money transfers are now larger than many countries' entire GDP.

Despite the scale of this market, the average cost of sending a remittance remains 6.49% of the amount sent (World Bank, Q1 2025). That means roughly $44 billion is lost to fees, FX markups, and intermediary costs every year. For a $200 transfer, a migrant worker pays nearly $13 in fees before a single dollar reaches their family.

The industry has spent decades trying to fix this from the delivery side with faster payouts, more mobile wallets, better last-mile networks. But the bottleneck was never delivery. It was always “origination”.

What Is Origination in Remittance?

Origination is the process of accepting a user's money in the sending country and converting it into a form that can move across borders. In traditional remittance, this means collecting local currency through local payment rails (bank transfers, cards, mobile money), verifying the sender's identity, running compliance checks, and initiating the transfer.

Every step of that process is jurisdiction-specific.

A bank transfer in the United States operates under different rules, different payment networks, and different regulatory requirements than a bank transfer in Germany. Card acceptance in Australia follows different interchange structures than card acceptance in Kuwait. KYC requirements in France differ from KYC requirements in the United Kingdom.

There is no such thing as a universal origination flow. Each sending country is, effectively, its own product.

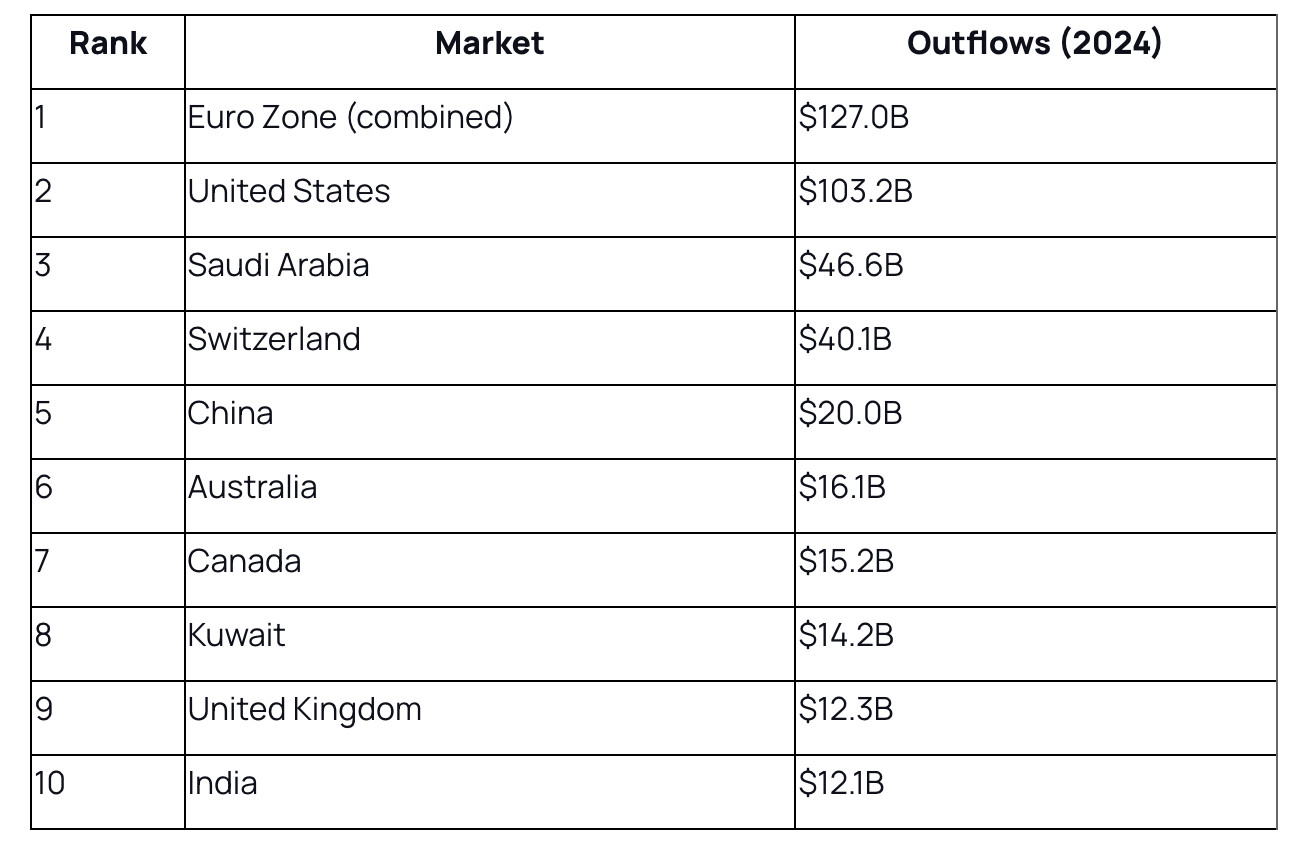

The Top 10 Remittance-Sending Markets

Using World Bank 2024 data (indicator: BM.TRF.PWKR.CD.DT, "Personal remittances, paid"), the top 10 remittance-origination markets are:

The Euro Zone is the single largest remittance-origination market in the world. When you aggregate outflows from Germany ($23.7B), France ($19.7B), Luxembourg ($18.7B), the Netherlands ($18.1B), Italy ($12.4B), Belgium ($10.1B), Austria ($9.7B), and the remaining Eurozone members, the combined total reaches $127 billion. That exceeds even the United States.

This is rarely discussed because most analyses rank countries individually. But for any company building remittance infrastructure, the Euro Zone functions as a single regulatory and payments environment under SEPA and, increasingly, under MiCA. Treating it as a fragmented collection of small markets is a strategic mistake.

Why Origination is the Hardest Layer to Build

Building delivery infrastructure (the "last mile" of remittance) is difficult, but it benefits from a relatively standardized set of outputs, i.e., bank deposits, mobile money credits, etc. The input side, origination, has no such standardization.

Here is what it takes to launch origination in a single new market.

Licensing and Regulatory Compliance

Every jurisdiction requires specific licenses to accept consumer funds.

In the United States, money transmission licenses are issued state by state. In the European Union, an Electronic Money Institution (EMI) license or Payment Institution (PI) license covers the region, but compliance requirements vary significantly between member states. In the UK, firms need FCA authorization. In Australia, AUSTRAC registration is required.

Securing these licenses takes 6 to 18 months. Maintaining them requires ongoing compliance teams, regulatory reporting, and audit infrastructure.

Local Payment Rail Integration

Users in different markets pay differently.

In the US, ACH bank transfers and card payments dominate. In Europe, SEPA transfers and local card schemes are standard. In the Gulf states, bank transfers and specific domestic payment systems prevail. In Australia, PayID and NPP (New Payments Platform) are becoming standard alongside cards.

Each integration requires separate technical work, separate banking relationships, and separate settlement flows.

Identity verification and KYC

KYC requirements vary by jurisdiction, not just in what documents are accepted but in how verification must be performed.

Some jurisdictions require video verification. Others accept document-only flows. Liveness checks, address verification methods, and acceptable ID types all differ.

A KYC flow built for the United States will not pass regulatory review in Germany. A flow built for the UK will not satisfy Australian requirements.

Fraud and Risk Management

Chargeback rules, fraud patterns, and risk thresholds differ by market.

Card-present and card-not-present fraud rates vary significantly across geographies. The risk profile of a transaction originating from Kuwait looks fundamentally different from one originating from Canada.

Risk models must be trained on local data. Generic, global models consistently underperform.

Banking Relationships

To collect local fiat, you need banking partners in each market.

And banks have been aggressively de-risking their exposure to money transfer businesses. A compliance issue in one corridor can cause a banking partner to terminate the entire relationship.

Smaller remittance companies report that maintaining banking access is their single largest operational challenge.

The Compounding Cost of Building Origination In-House

For a remittance company expanding into new corridors, the cost of origination is not linear. It compounds.

Each new market requires its own license, its own banking partner, its own payment integrations, its own KYC flows, its own fraud models, and its own compliance team. A company operating in 5 sending markets doesn't have 5x the origination cost. It has closer to 5x the regulatory surface area, 5x the banking dependency risk, and 5x the ongoing compliance burden.

This is why most remittance companies serve a handful of corridors well and struggle to expand beyond them. The delivery side scales but the origination side does not.

It is also why the largest remittance operators (Western Union, Wise, Remitly) have spent years and hundreds of millions of dollars building their origination networks. For newer entrants, replicating this infrastructure is prohibitively expensive.

How Stablecoin Rails Change the Equation

The emergence of stablecoins as a settlement layer has fundamentally changed what is possible in cross-border payments. Stablecoins now power $46 trillion in annual transactions globally, and their application in remittance is accelerating.

The stablecoin model for remittance works in two steps:

- Step 1 (Origination): A user in the sending country pays in local fiat. That fiat is converted into stablecoins through regulated infrastructure.

- Step 2 (Settlement and delivery): Stablecoins move across borders in minutes (or seconds), then convert back to local currency at the destination for payout.

Step 2 is, for the most part, solved. Blockchain settlement is fast, transparent, and cheap. The infrastructure for converting stablecoins back to fiat in receiving countries is maturing rapidly.

Step 1 remains the bottleneck. Converting local fiat into stablecoins in a compliant, low-friction way, across dozens of sending countries, through locally accepted payment methods, with full KYC and AML compliance, is the hard part.

This is the origination layer.

What Origination Infrastructure Looks Like at Scale

Solving origination at scale requires a platform approach, not a corridor-by-corridor build. The infrastructure must handle:

- Multi-jurisdiction licensing: Regulatory coverage across sending markets, with licenses maintained and updated as regulations evolve.

- Local payment method acceptance: Cards, bank transfers, SEPA, ACH, faster payments, and market-specific methods, all through a single integration point.

- Modular identity verification: KYC flows that adapt to jurisdiction-specific requirements, using local document types, verification methods, and compliance standards.

- Real-time risk assessment: Fraud and AML scoring calibrated to local transaction patterns, with the ability to ingest partner risk signals.

- Fiat-to-stablecoin conversion: Compliant conversion of local currency into stablecoins for cross-border settlement.

This is what we have built.

Transak for Remittance Origination

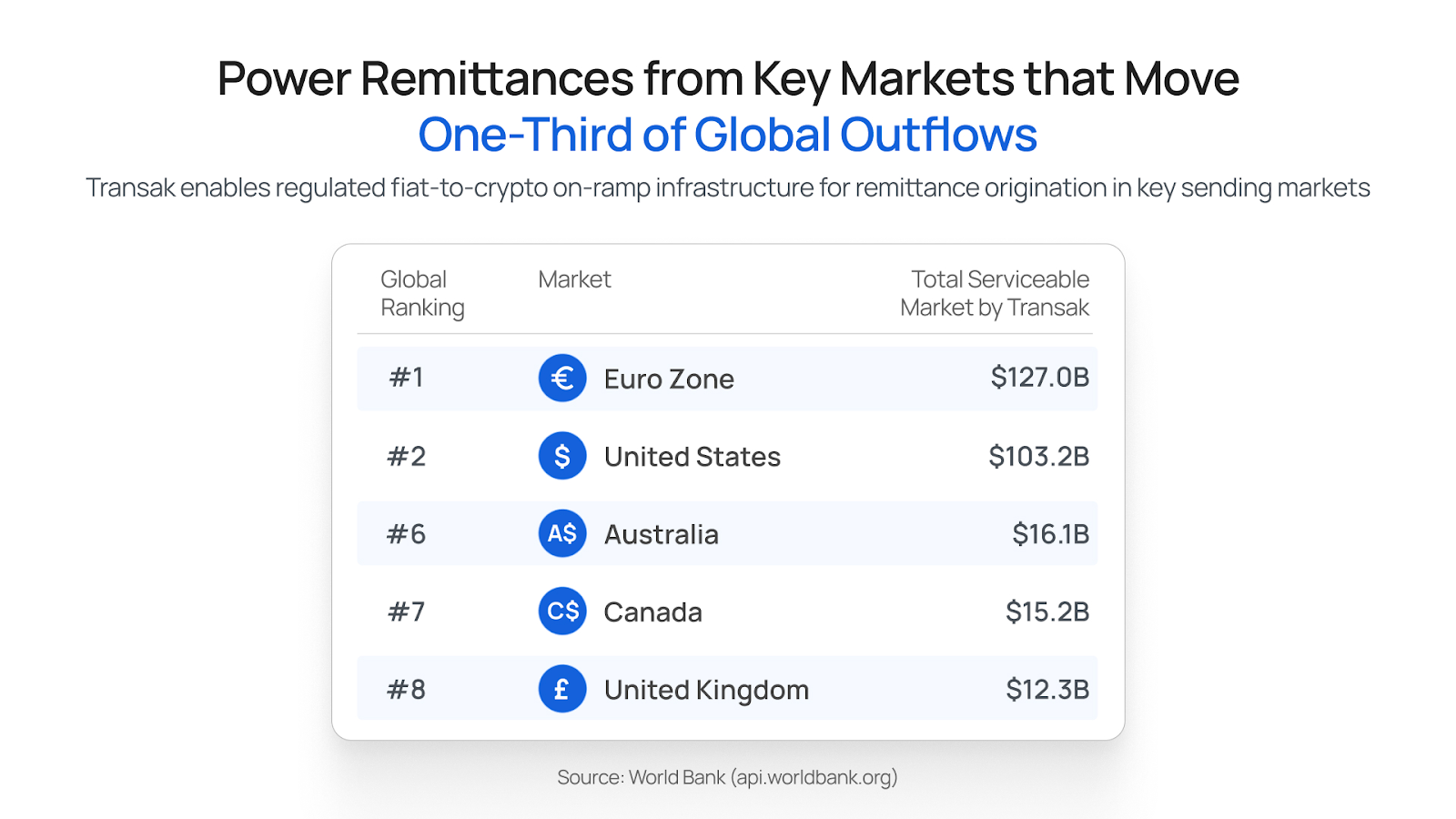

With regulatory coverage across 64+ countries, including 6 of the top 10 remittance-origination markets, Transak provides the origination infrastructure that remittance companies can integrate through a single API.

Rather than building and maintaining licensing, banking relationships, payment integrations, and compliance infrastructure in each sending market, remittance platforms can embed Transak's infrastructure and go live in weeks instead of months.

The architecture is modular. Companies can use the full stack, or plug in only the components they need. For companies that already have KYC or auth infrastructure, Transak can operate in "reliance mode," accepting existing verification.

Finally, we’ll leave you with this takeaway. In a $850 billion market, the hardest problem isn't moving money across borders. It's getting money into the system in the first place.

Transak is the regulated payments infrastructure for stablecoins and crypto. With coverage across 64+ countries and 600+ integrated partners, Transak provides the origination layer that powers the next generation of cross-border payments. Talk to us.