Takeaways

In 2002, eBay acquired PayPal for $1.5 billion. At the time, PayPal processed payments for over 70% of eBay auctions. It was the invisible layer that made eBay work.

But in 2015 the companies split and PayPal had spun off into an independent company. By 2020, eBay had replaced PayPal with Adyen. And by 2025, PayPal's consumer products (Venmo, PayPal.me, Honey, Xoom) were directly competing with the same merchants who once depended on it.

And now, history is repeating itself by playing out in crypto payments infrastructure.

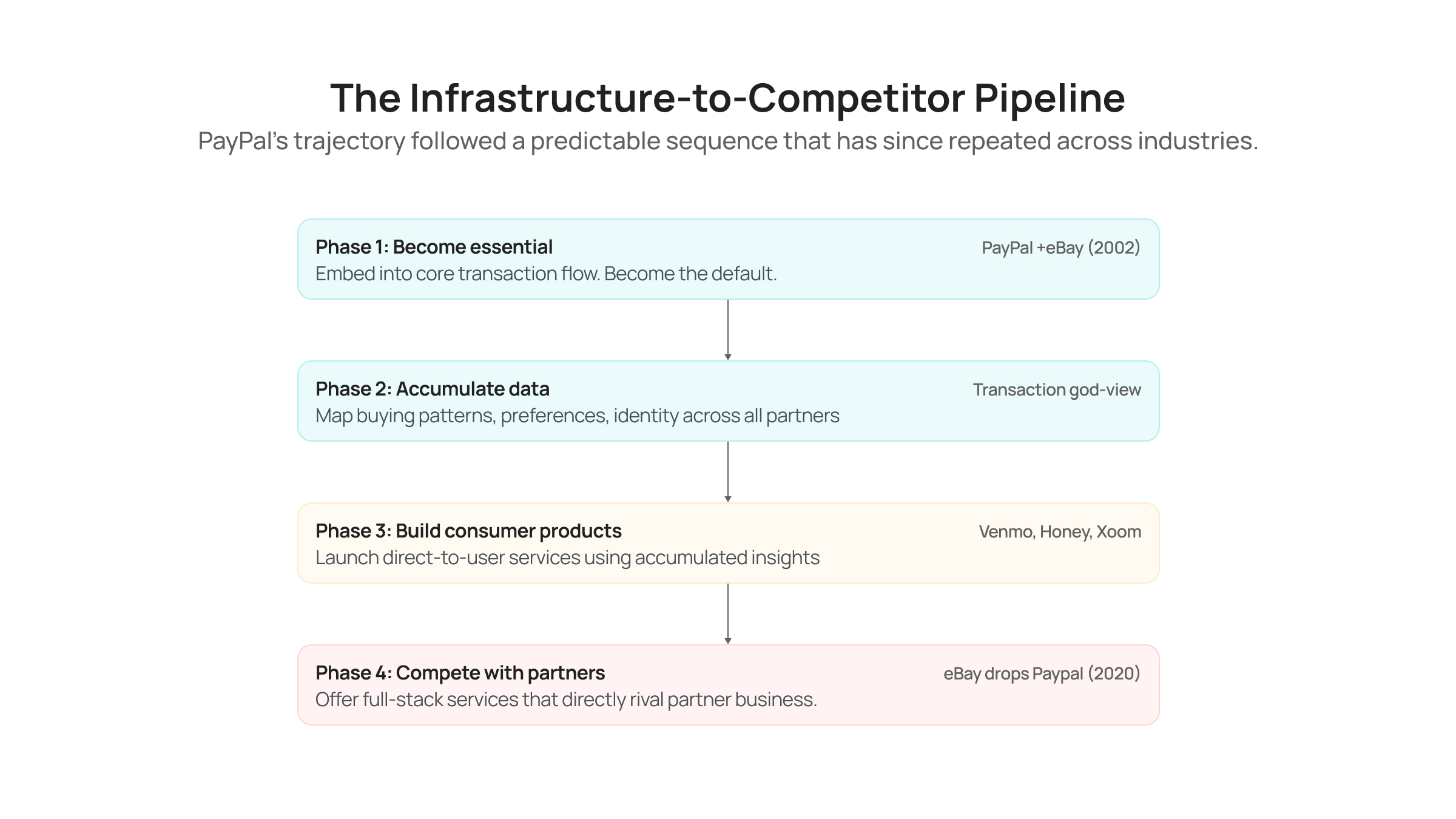

The Infrastructure-to-Competitor Pipeline

PayPal's trajectory followed a predictable sequence that has since repeated across industries.

Phase 1: Become Essential

PayPal embedded itself into eBay's core transaction flow. It became the default. Merchants could not sell effectively without it. By 2012, PayPal accounted for 40% of eBay's total revenue and processed $145 billion in payment volume.

Phase 2: Accumulate Data

Every transaction that flowed through PayPal generated insight. Who was buying, what they paid, how often they returned, where they lived, what payment methods they preferred. PayPal had a god-view of commerce patterns across millions of sellers.

Phase 3: Build Consumer Products

PayPal launched its own consumer-facing services. Venmo for peer-to-peer payments. PayPal.me for direct payment requests. Honey for shopping rewards. Xoom for international remittances. Each product turned PayPal from a background utility into a destination.

Phase 4: Compete with Your Partners

PayPal Complete Payments now offers merchants a full-stack checkout, marketing tools, and buyer engagement features. The company that started as infrastructure now competes for the same consumer attention and spending that its merchant partners are trying to capture.

eBay saw this coming very early. So, it moved to Adyen in 2020 and rebuilt its payment stack from scratch. Most merchants were not in a position to do the same.

Braintree: B2B Infrastructure Turned Consumer Checkout

In 2013, PayPal acquired Braintree for $800M. Braintree was the definition of infrastructure fidelity. It was used by Uber, Airbnb, and thousands of marketplaces that needed reliable payment processing without a competing agenda.

Braintree came with Venmo.

PayPal turned Venmo from a peer-to-peer app into a checkout button and pushed it into the same merchant payment pages that Braintree powered. Merchants who chose Braintree for clean, invisible infrastructure now had PayPal inserting a branded consumer experience into their checkout flow.

Xoom: Competing in Your Partners' Corridors

In 2015, PayPal acquired Xoom for $890M and entered cross-border remittance directly.

Remittance companies had been using PayPal's payment rails to process transfers for years. PayPal had visibility into which corridors moved the most volume, which fee structures converted best, and which user segments sent money most frequently.

Xoom launched into those exact corridors. Armed with data from the very partners it was about to undercut.

PYUSD: When Your Rails Start Issuing the Asset

In 2023, PayPal launched PYUSD, its own stablecoin.

Crypto wallets and exchanges had integrated PayPal as a fiat payment method. It was a clean split. Apps handled the crypto side. PayPal handled the fiat side.

Then PayPal started issuing the asset itself. The fiat payment provider became a stablecoin issuer competing for the same user wallet share as the apps it serviced.

Why This Pattern Repeats

The mechanism is always the same. An infrastructure provider sits between a business and its customers. Over time, the provider accumulates enough data and enough user relationships to realize that it can capture more value by going direct.

If a company has already acquired user relationships through its B2B partners, launching a consumer product becomes a calculated move backed by data that no competitor can replicate.

Three conditions accelerate the betrayal.

1. The provider holds user identity

If the infrastructure layer requires account creation, KYC verification, or payment credentials, the provider owns a direct relationship with the end user, not the partner. The partner thinks the user belongs to them. The data says otherwise.

2. The provider sees across all partners

A single partner sees its own users. The infrastructure provider sees patterns across hundreds or thousands of integrations. It knows which products are trending, which markets are growing, and which user segments are most valuable, months before any individual partner does.

3. The provider has switching costs working in its favor

Users who have completed KYC, saved payment methods, or built transaction history with the infrastructure provider face friction when switching. Even if the partner changes providers, the users' relationship with the old provider persists.

This Is Now Happening in Crypto Payments

Several crypto payments infrastructure providers have recently launched consumer-facing applications. Some have built standalone wallets. Others offer direct purchase interfaces that compete with the same exchanges and wallet apps that integrate their services. Not every provider has taken this route. Some, like us, have made a deliberate decision to stay on the infrastructure side of the line, treating partner growth as their own growth metric. But the ones that have crossed over are already deep into the playbook.

The dynamics are more pronounced in crypto than in any previous industry for one reason. Crypto on-ramp and off-ramp providers collect government-issued identification documents, bank account details, and transaction histories. This is KYC-grade identity data tied to financial accounts.

When an infrastructure provider with thousands of integrations and millions of KYC-verified users launches a consumer app, it starts with advantages that no organic startup can match. It already knows the users. It already has their payment credentials. It already understands their transaction patterns across every partner application.

A provider that operates both a B2B infrastructure service and a consumer product faces an inherent conflict. Where should engineering resources go? Which product gets better approval rates? Which users see marketing messages for the consumer app after completing a transaction through a partner?

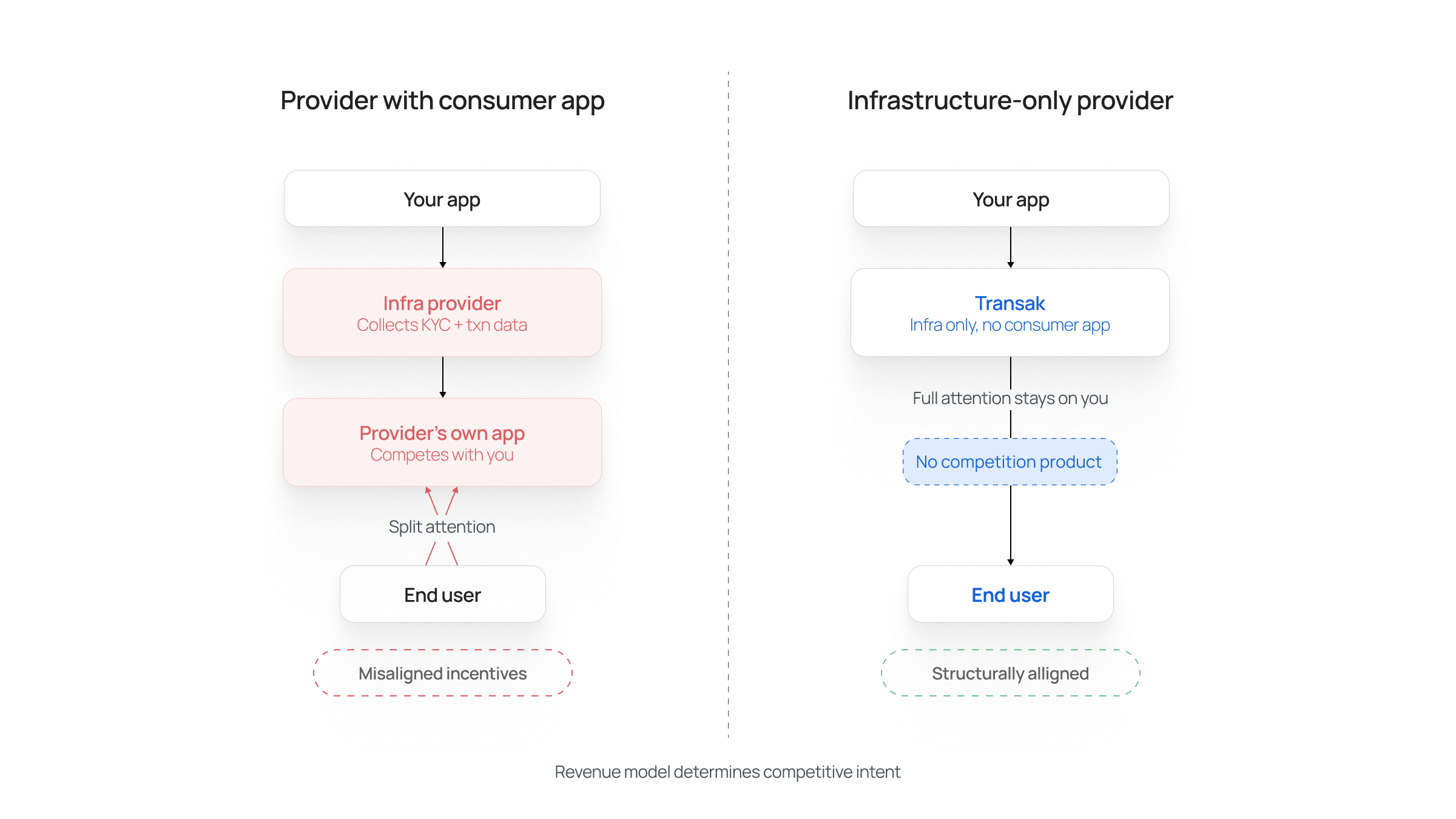

What Structural Alignment Looks Like

The alternative to the PayPal playbook is infrastructure that is designed, from the ground up, to never compete with its partners.

This is a business model decision. A company that generates revenue primarily from B2B infrastructure, like Transak, has no economic incentive to redirect users away from partners. Its growth is directly tied to partner growth.

When evaluating payments infrastructure, the questions that matter most have nothing to do with fees or geographic coverage.

- Does the provider operate a consumer-facing product?

- Does the provider retain the right to market to users acquired through partner integrations?

- Does the provider require users to create an account with the provider (rather than the partner) to complete transactions?

- Does the provider's compliance infrastructure hold KYC data in a way that could be leveraged for a future consumer product?

The eBay Lesson

eBay's decision to drop PayPal in favor of Adyen was painful, expensive, and took years to execute. But eBay's leadership recognized something that most companies learn too late. When your infrastructure provider has consumer ambitions, every day you remain integrated is a day they get stronger at your expense.

The crypto industry is still early enough that companies can make this choice proactively. The question is whether they will.

Every wallet, exchange, and dApp that relies on third-party payment rails should be asking a simple question about their infrastructure provider.

Are they building for you, or are they building toward replacing you?

Transak provides payments infrastructure for financial applications across 64+ countries. Transak does not operate a consumer wallet, remittance app, or other similar applications. Learn more about our approach to infrastructure alignment.