Takeaways

Cross-border payments still cost too much, and the people sending the money are usually the first to know. The global average cost to send a $200 remittance was 6.39% from G20 countries in Q3 2025, with digital channels averaging 4.59% and non-digital averaging 7.30%. Stablecoins are the first credible challenger to that pricing in a generation.

Total stablecoin payments more than doubled to about $390 billion in 2025, according to McKinsey and Artemis Analytics.

But "stablecoins for payments" hides the more useful question, which is which corridors. The economics shift dramatically depending on the route, the dominant token, the local payment rail at the off-ramp, and the regulatory shape.

This guide walks through the five corridors where stablecoin payments have genuinely changed the math, and one where policy is keeping things frozen.

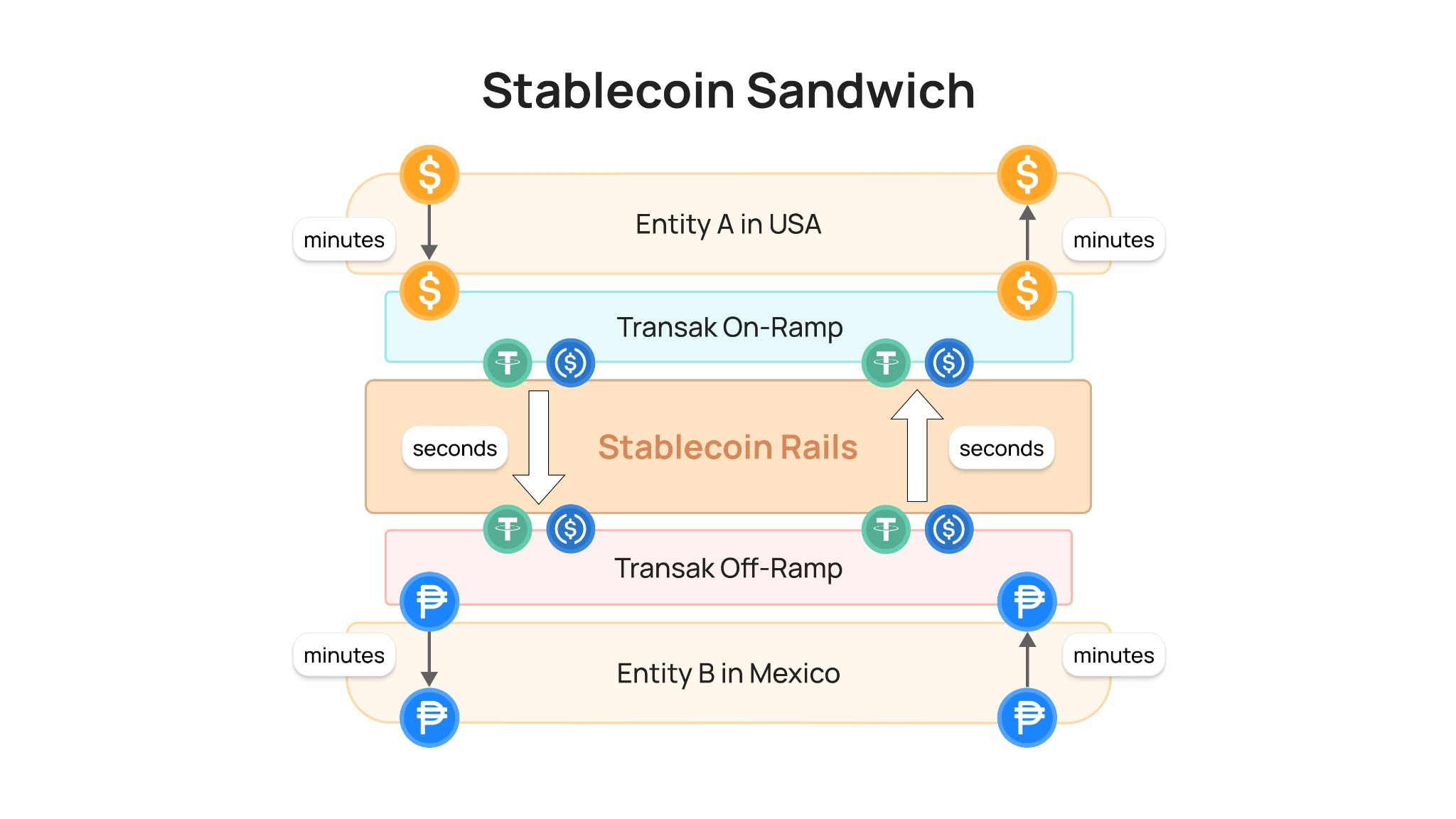

What Is A Stablecoin Corridor?

A stablecoin corridor is a cross-border payment route where a dollar-pegged token sits between two fiat currencies as the settlement layer.

A sender's local currency is converted into a stablecoin like USDC or USDT through an on-ramp, the token moves over a public blockchain in seconds, and an off-ramp converts it back into the recipient's local currency. The corridor's economics depend on costs at both ramps, not the on-chain leg.

The on-chain transfer is close to free. The cost lives in the FX spread, the off-ramp fee, and last-mile fiat payout.

Also Read: What Is A Stablecoin Sandwich

How To Read A Corridor

Four variables determine whether a stablecoin corridor actually works in practice. All-in cost from sender to recipient is the headline number, but it depends on the other three.

The four-variable check:

- All-in cost: Sender fee plus FX spread plus off-ramp fee plus last-mile payout

- Dominant flow: B2B settlement, retail remittance, or store-of-value

- Regulatory shape: What's legal, what's tolerated, what's hostile

- Ramp depth: Number of licensed providers and reliability of fiat payout

Most analyses focus on cost alone. That misses why some corridors with similar prices behave completely differently. Sub-Saharan Africa, for example, sees nine of the world's thirteen corridors with costs above 20 percent in Q3 2025, and the issue is rarely sender-side fees. It's off-ramp depth and FX liquidity.

Also Read: The Origination Layer: Where Remittance Companies Win or Lose

United States → Mexico

The US-Mexico stablecoin corridor is the most mature in the world. It's also the cleanest case study for how the model works at scale, and the only retail-adjacent corridor where the cost compression is now obvious to operators on both sides.

|

Variable |

Value |

|

Mexico inbound remittances, 2025 |

|

|

Traditional cost on a $200 transfer (Q1 2025) |

|

|

Stablecoin B2B cost, best case |

Under 1% end to end |

|

Dominant stablecoin |

USDC |

United States/EU/UK → Philippines

The Philippines corridor is the second most-developed retail stablecoin route globally. It's also the cleanest example of policy and infrastructure moving together, with the country's national QR standard now natively supporting stablecoin payments alongside the peso.

|

Variable |

Value |

|

Philippines inbound OFW remittances, 2024 |

|

|

US-to-Philippines cost on $200 |

|

|

Stablecoin savings vs traditional |

|

|

Dominant stablecoin |

USDC, USDT |

Argentina

Argentina breaks the framework, which is exactly why it's worth studying. It isn't a one-way remittance route. It's a multi-directional store-of-value corridor where stablecoins serve as savings, hedge, and B2B rail simultaneously.

|

Variable |

Value |

|

Argentina crypto transaction volume |

|

|

Stablecoin share of all crypto volume |

|

|

Argentines who own crypto |

|

|

Inflation, September 2025 |

|

|

Dominant stablecoins |

USDT, USDC |

Nigeria

Nigeria is the largest stablecoin economy outside the United States, and the clearest example of a corridor driven by import-export finance rather than household remittance.

|

Variable |

Value |

|

On-chain volume, mid-2024 to mid-2025 |

|

|

Active digital asset users |

|

|

Stablecoin share of sub-$1M flows |

|

|

Naira depreciation, 2019–2024 |

|

|

Dominant stablecoins |

USDT, cNGN |

India

India should be the largest stablecoin corridor in the world. It isn't, almost entirely because of policy. The country is the largest recipient of inbound remittances globally, yet retail stablecoin remittance into India remains structurally unavailable through compliant infrastructure.

|

Variable |

Value |

|

Inbound remittances |

Largest globally (~$120B+) |

|

RBI position |

Hostile to private stablecoins |

|

Compliant retail off-ramp for USDC/USDT |

None at scale |

|

LRS individual remittance cap |

What This Means for Payment Builders

The pattern across all five active corridors is the same. The on-chain leg is solved. The hard parts are the on-ramp in the sending country, the off-ramp in the receiving country, and the compliance scaffolding around both. Anywhere you see a corridor working at scale, it's because someone built that scaffolding first.

This is why infrastructure is the actual business under all of this. Transak raised a $16 million strategic round led by Tether and IDG Capital in 2025, on the thesis that issuers may mint the dollars, but without compliant gateways, distribution stalls. The same logic applies to every operator running an actual corridor today. Transak covers 40+ off-ramp assets across 20+ networks in 60+ countries, which is closer to the shape of a payments network than a crypto product.

The corridor takeaway for builders is simple. Don't optimize for the cheapest on-ramp. Optimize for the off-ramp you can rely on in your destination market, and the compliance license that lets you operate there without legal risk. Solve those two, and the cost compression follows.

Corridors To Watch In Late 2026

A few corridors are at inflection points worth tracking.

The UAE-Pakistan corridor is the Middle East's largest at $24 billion in annual remittances, with the UAE's DFSA and ADGM frameworks attracting stablecoin infrastructure and Pakistan's Q4 2025 sandbox approving three stablecoin remittance providers for pilots. If those pilots scale, this becomes the next major route after US-Mexico.

Brazil has the volume already. The country saw $318.8 billion in crypto inflows through mid-2025, with over 90% moving through stablecoins. PIX integration makes the off-ramp leg trivial. Retail adoption is the missing piece.

Sub-Saharan Africa more broadly is the largest single arbitrage opportunity in remittances globally. Of the 13 corridors with costs above 20% in Q3 2025, nine originate from SSA. Whoever solves off-ramp depth in Nigeria, Kenya, Ghana, and South Africa simultaneously will own the corridor that matters most.

Unlock New Corridors with Transak

If the bottleneck to a new corridor is regulatory scaffolding and ramp depth, Transak is built to solve both.

We hold licenses across several jurisdictions that allow businesses integrating our solutions tap into major markets, and the full on/off-ramp stack can ship as a single API that handles fiat conversion, KYC, sanctions checks, and local payment methods.

Sandbox access takes a few days to set up. A full production integration is usually live in under four weeks. Against the 12 to 18 months it takes to build the same coverage in-house, that's the shortest path from idea to a live route.

FAQ

What's the cheapest stablecoin corridor right now?

The US-Mexico corridor is the most cost-compressed. B2B stablecoin flows often clear under 1 percent end to end against a traditional cost of around 5 percent on a $200 transfer.

Which stablecoin dominates cross-border payments?

USDT and USDC together hold most of the stablecoin market share. USDC tends to dominate compliant flows in regulated corridors like US-Mexico and US-Philippines. USDT dominates emerging-market and peer-to-peer flows in Nigeria, Argentina, and across Asia, where regulatory licensing for USDC is less established.

Why doesn't India have a working stablecoin corridor?

The Reserve Bank of India considers dollar-backed stablecoins a macroeconomic risk and prioritizes the digital rupee CBDC instead. As of December 2025, the RBI's Deputy Governor publicly dismissed the case for stablecoins in India. A domestic alternative called ARC is targeting an early 2026 launch but is restricted to business accounts.

What's the role of on-ramp and off-ramp providers in a stablecoin corridor?

Ramp providers handle fiat-to-stablecoin conversion, KYC/AML compliance, local payment method integration, and last-mile fiat payout. A corridor only works as well as its weakest ramp, so choose wisely.