Takeaways

1.3 billion adults can't open a bank account. The annual cost of their exclusion runs into the trillions of dollars, paid in remittance fees, inflation losses, and the everyday surcharges that come with handling cash in a digital economy.

Most of that cost never appears on a balance sheet. For example, a construction laborer in Houston pays $10 to send $100 home to his mother in Honduras, and waits three days for it to arrive.

Many of us thing those are edge cases. But that’s the everyday economics of roughly a quarter of the world's adult population, and the largest unbuilt market in financial services.

For the first time in modern financial history fintech founders can effectively solve issues for the unbanked and the underbanked with stablecoins and blockchain rails.

Who Counts As “Unbanked” and “Underbanked”?

The unbanked are adults with no account at any bank, credit union, or mobile money provider. The underbanked have an account but rely on nonbank services like check cashers and payday lenders for things accounts are supposed to do. Together, they make up roughly a quarter of the world's adult population, with most concentrated in just eight countries.

The World Bank's Global Findex 2025, published in July 2025, found that about 1.4 billion adults still lack any kind of financial account. Another 300 million hold accounts that sit dormant. More than half the world's unbanked live in eight countries, i.e., Bangladesh, China, Egypt, India, Indonesia, Mexico, Nigeria, and Pakistan. Women make up 55% of the unbanked. The poorest 40% of households account for 52%.

In the United States, the FDIC's 2023 National Survey found 4.2% of households (about 5.6 million) were fully unbanked, and 14.2% (around 19 million) were underbanked. The unbanked rate is a record low, but the gaps are not evenly distributed.

Group |

U.S. unbanked rate (households)* |

|

Black households |

10.6% |

|

American Indian/Alaska Native |

12.2% |

|

Hispanic households |

9.5% |

|

White households |

1.9% |

*Source: FDIC 2023 National Survey of Unbanked and Underbanked Households.

What Is The "Being-Poor Tax"?

The being-poor tax, also known as the poverty premium, is the extra cost low-income and unbanked households pay for the same essential services. It surfaces in higher remittance fees, predatory credit, costly nonbank financial services, and inflation that erodes cash savings. Estimates run into hundreds of dollars per household annually in developed markets, and far more in emerging ones.

University of Bristol researchers, working with Fair By Design, peg the average UK poverty premium at £490 per household per year. Total drag on low-income British households runs to roughly £2.8 billion annually. People in poverty pay more for energy, more for credit, more for insurance, and more to access their own cash.

In the U.S., the Financial Health Network estimates households spent over $25 billion a year on fees and interest for nonbank financial services between 2020 and 2022. The spending concentrates in unbanked and underbanked populations.

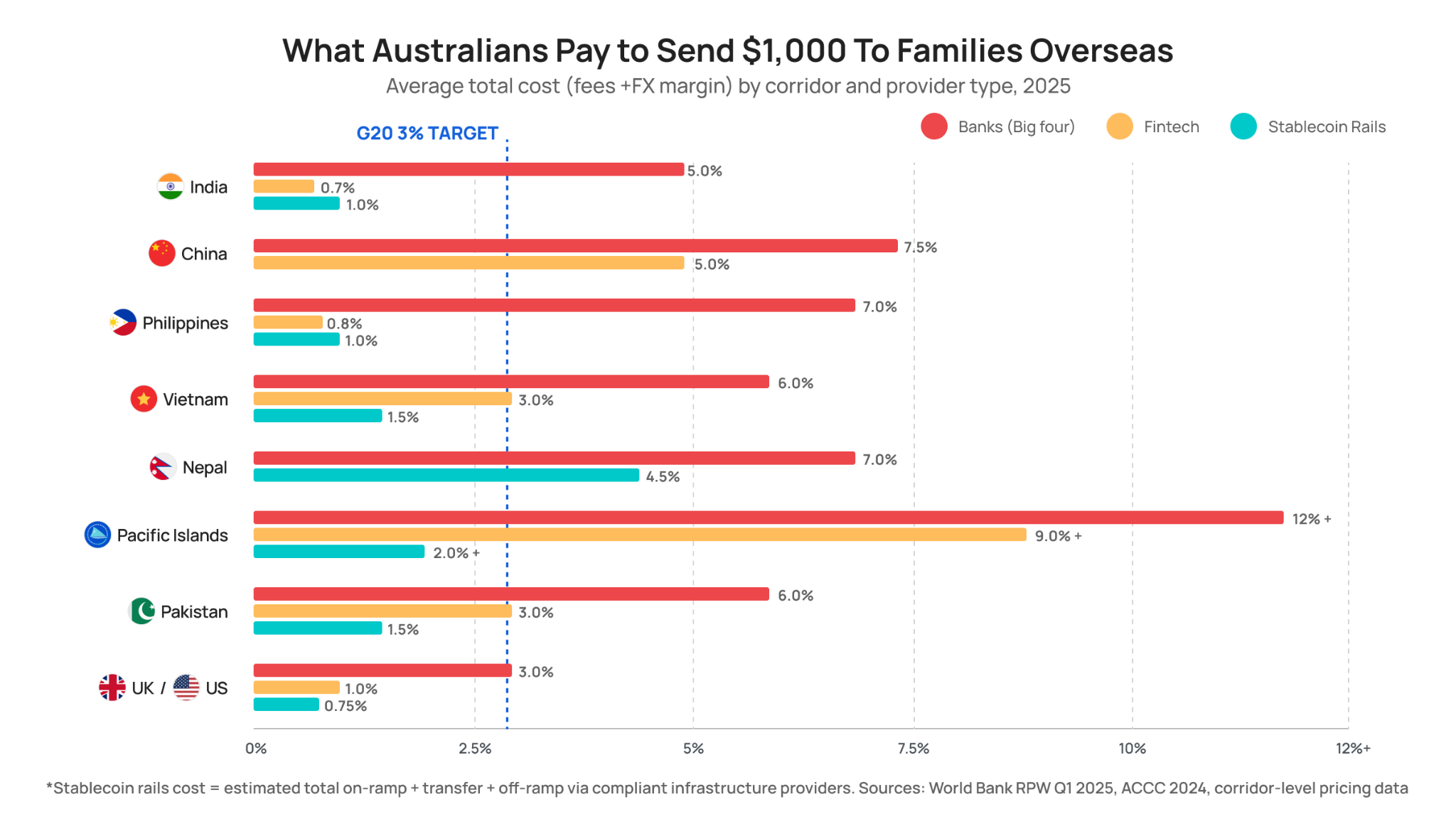

The most visible international version is remittance fees. The World Bank's Remittance Prices Worldwide database recorded a global average cost of about 6.5% to send $200 in early 2025. That's more than double the UN Sustainable Development Goal target of 3%. Sub-Saharan Africa is the most expensive region, at roughly 8.5%. Corridor-level costs above 10% are still common.

The flows are massive. Officially recorded remittances to low- and middle-income countries hit an estimated $685 billion in 2024, with global flows around $905 billion. Remittances now exceed foreign direct investment plus official development assistance combined for the developing world. Every percentage point of friction in that pipe strips roughly $9 billion a year from households that, by definition, can least afford it.

Then there's currency itself. Argentina averaged about 220% inflation in 2024. Turkey ran at 58.5%, Venezuela at 49%, Nigeria at 31.4%. Holding savings in local currency in those economies works as a recurring tax, paid quietly every day by anyone who lacks access to a stable store of value. That access has historically meant a U.S. dollar bank account, which most of these people cannot legally or practically open.

Why Hasn't Traditional Fintech Closed The Gap?

Domestic fintech has worked brilliantly inside borders.

The last fifteen years of fintech have produced extraordinary wins. Payment methods like M-Pesa, PIX, and UPI have brought hundreds of millions into the formal financial system. But these systems hit a wall, and that wall is the border.

The trouble starts when money has to cross a border, currency, or regulator. Settlement reverts to correspondent banking, which still relies on pre-funded nostro accounts, business-day cutoffs, and a chain of intermediaries that each take a slice.

A wire that takes "3 to 5 business days" is, in 2026, a polite description of a 1970s clearing model running on top of fiber optics.

Neobanks have extended access to underserved consumers, but most cannot bank a customer who doesn't exist on a credit bureau, has no permanent address, or earns wages across multiple jurisdictions. None of these stacks were built for the 21st-century reality of distributed labor, distributed family, and distributed currency risk.

How Do Stablecoins Reduce The Cost Of Being Unbanked?

Stablecoins are tokenized claims on a stable asset, usually a U.S. dollar, that move on public blockchain networks. They settle in seconds, around the clock, for a fraction of a cent in many cases. For unbanked users, they offer three things traditional rails don't:

- Dollar access without a U.S. bank account

- Near-zero-cost cross-border transfer

- Smartphone-friendly onboarding

Volume tells the story. Stablecoin transfer volume reached roughly $27.6 trillion in 2024, exceeding the combined annual transaction volume of Visa and Mastercard. That headline figure deserves a caveat because as much as 70% is bot- and protocol-driven activity rather than human payments. Even adjusted, the human-and-business share is in the trillions, growing fast, and concentrated in exactly the markets that are underserved by everything else.

Chainalysis's 2024 and 2025 Geography of Crypto reports show stablecoins making up the majority of crypto exchange purchases in Argentina, Brazil, Colombia, Nigeria, and Turkey. In Argentina, stablecoins represent roughly 62% of crypto transaction volume, well above the global average of 45%. Turkey alone processed more than $63 billion in cross-border stablecoin payments in 2024.

Three outcomes drive that adoption.

1. Dollar access without a dollar bank account

A worker in Buenos Aires who cannot legally open a U.S. dollar bank account can hold a dollar-denominated balance in a wallet on her phone. For hundreds of millions of people, this is the first time they've had a reliable savings instrument.

2. Cross-border transfer at near-zero marginal cost

Felix Pago, a Miami-based remittance company, lets U.S. workers send money to family in Mexico, Guatemala, and Honduras directly through WhatsApp, using USDC behind the scenes. The customer never knows a stablecoin was involved.

|

Channel |

Avg. cost to send $200 |

Settlement time |

|

Bank wire transfer |

$25–$50 |

1–5 business days |

|

Money transfer operator (e.g., Western Union) |

~$13 (6.5%) |

Minutes to hours |

|

Stablecoin-powered remittance (e.g., Felix Pago) |

~$3 (1.5%) |

Seconds to minutes |

Sources: World Bank Remittance Prices Worldwide 2025; Felix Pago published rates.

3. Smartphone-friendly onboarding and 24/7 settlement

A merchant in Nairobi can settle with a supplier in Dubai on a Saturday night without waiting for Monday morning correspondent windows. Payroll for a remote workforce spread across twelve countries can run on the same rail without twelve banking relationships.

Conclusion

For fintech founders, stablecoins are infrastructure, not a product category. They're a settlement layer that changes the unit economics of cross-border products.

Using stablecoins is utility, not novelty. The financial rails could and, for many, should stay invisible. Customers should not have to take a masterclass on blockchain to make a $1000 transaction. They should notice that the money arrives faster, costs less, and holds its value.

If you're building a cross-border fintech product and want to talk about the rails underneath it, get in touch.

FAQs

How many people are unbanked globally in 2025?

About 1.4 billion adults worldwide have no account at any financial institution, according to the World Bank's Global Findex 2025. Another 300 million hold dormant accounts. More than half live in eight countries: Bangladesh, China, Egypt, India, Indonesia, Mexico, Nigeria, and Pakistan.

What is the average cost of sending an international remittance?

The World Bank's Remittance Prices Worldwide database recorded a global average of 6.5% to send $200 in early 2025. The UN Sustainable Development Goal target is 3% by 2030. Sub-Saharan Africa remains the most expensive region at roughly 8.5%.

Why are stablecoins useful for unbanked populations?

Stablecoins give users in inflation-prone or underbanked economies three things traditional banking does not: dollar-denominated savings without a U.S. bank account, near-instant cross-border transfers at a fraction of traditional costs, and onboarding that requires nothing more than a smartphone.

Are stablecoins a replacement for traditional banking?

No. Stablecoins complement existing financial infrastructure rather than replacing it. They're most useful as a settlement layer for cross-border use cases that traditional rails handle slowly or expensively, particularly in emerging markets with limited banking access or unstable local currencies.